WTPI

Equity Premium Income Fund

Published May 29, 2024

Head of Indexes, U.S.

The option-writing ETF category has seen renewed interest in the past 12 months, growing assets at a rate of 45%.1

The worst time to consider an option-writing ETF may be after very sharp drawdowns in the market that are susceptible to quick rallies—because, by design, option strategies are often capping the upside gains for the market over a shorter-term period.

But we believe some of the best times to consider them are when expectations for the returns off the underlying assets are expected to be subdued or face more near-term uncertainty with a constrained outlook.

With the S&P 500 selling at 21x forward earnings and having a robust period of outsized returns, now may be a particularly good time to consider them. Our own view is that the S&P 500 is set to have lower returns over the next 5–7 years than what it has delivered historically due to the higher valuations.

Options strategies can have meaningful differences in the types of options they sell (puts or calls) and the underlying basket of securities they track. The objective of most of these strategies is to either provide investors with income or reduce the “beta/volatility” in their portfolios.

The WisdomTree PutWrite Strategy Fund (PUTW) aims to achieve both objectives, seeking to provide investors with a monthly income distribution at a relatively stable level and offering a historical beta of 0.652 versus the S&P 500 Index.

PUTW tracks the Volos US Large Cap Target 2.5% PutWrite Index (VULPW25), an Index created in partnership with WisdomTree with the objective of providing investors with enhanced income potential and reduced volatility. VULPW25 follows a systematic, fully collateralized put-write strategy. In simple terms, for each dollar notional in puts sold (written), a dollar is saved (invested) in U.S. Treasuries.

VULPW25 Mechanics:

The questions below are ones we get frequently when talking about PUTW. To answer them, we will contrast the mechanics of VULPW25 with a strategy that rolls monthly or sells “at the money” strike.

Why roll twice per month?

By rolling options bi-weekly, VULPW25 achieves a smoother VIX exposure, averaging entry points 24–26 times per year. A strategy that rolls monthly only has 12 entry points per year.

Why target a 2.5% premium instead of selling “at the money” strike?

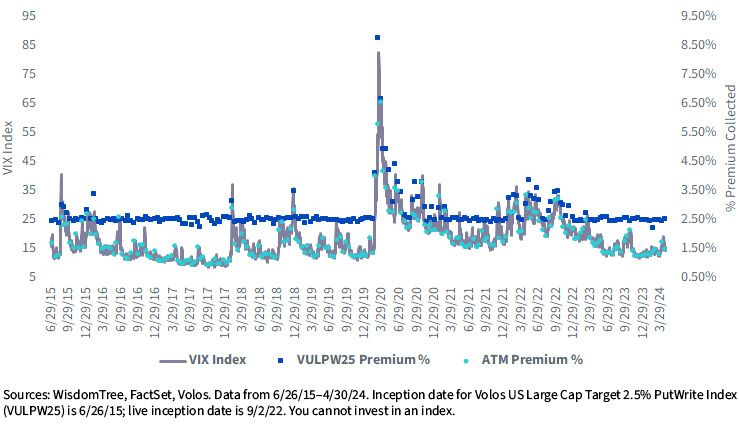

Targeting a consistent premium level allows PUTW to create a monthly income distribution target. As seen in the chart below, the dark blue dot shows the consistency in % premium collected by VULPW25 versus a strategy that sells “at the money” strike, which is more variable and dependent on the level of the VIX Index.

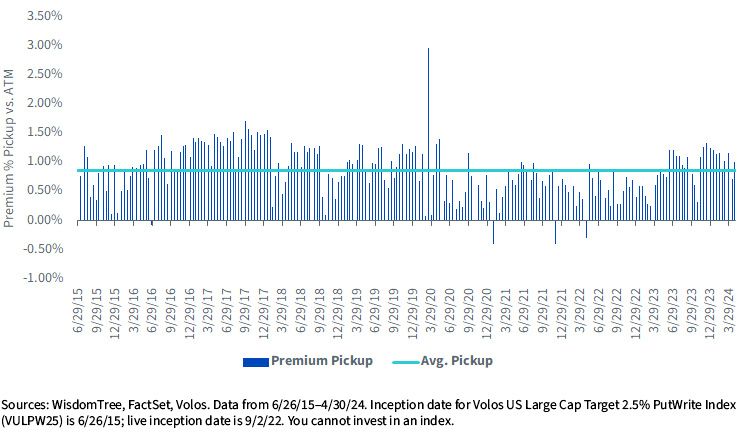

The second advantage is the improved upside potential. The upside in a put-write strategy is limited to the amount of premium collected when selling the options. By targeting a 2.5% premium at every roll, VULPW25 has an average premium pick-up of 0.85% monthly or 10.5% annually compared to selling “at the money” strike.

Does a stable monthly income distribution target mean I can assume annual returns around the annualized yield? Are returns capped at that yield?

The monthly income distribution target is only one component of the strategy’s total return. SPY put options have a price that moves in relation to the broad market and its volatility. Daily, the current price of these options is fully reflected in the strategy’s price.

On the roll date, SPY put options can be closed for gains or losses depending on the direction the market took during the period. These gains (or losses) will impact the strategy’s assets and translate into realized gains (or losses).

SPY put options are sold with a 2.5% premium target, which means the maximum gain from each put option can be 2.5%. By annualizing this number, the maximum upside for this strategy is around 30% (2.5% x 12 months). This upside will be achieved if every option is deep “out of the money” on the roll date (SPY is significantly up in the period), which is unlikely to happen every time.

Given the construction of its underlying Index, PUTW can be used in several ways within an investor’s portfolio. We’ll discuss a few of these below:

1. De-risking S&P 500 Exposure: Selling put options on an underlying asset provides a shock absorption to downward movements at the cost of a limited upside. This trade-off can be attractive to certain investors and in certain periods of expected market stress.

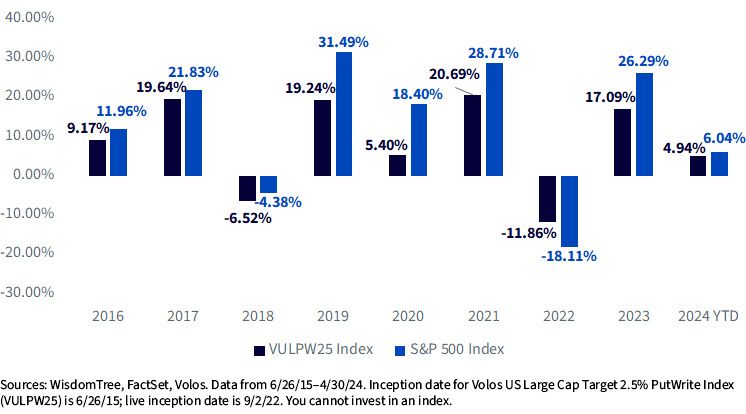

The calendar year performance of VULPW25 against the S&P 500 allows us to illustrate this trade-off. In years when the market shot up, VULPW25 managed to deliver consistent returns by giving up some upside, and in years of market volatility like 2022, it managed to reduce the drawdown.

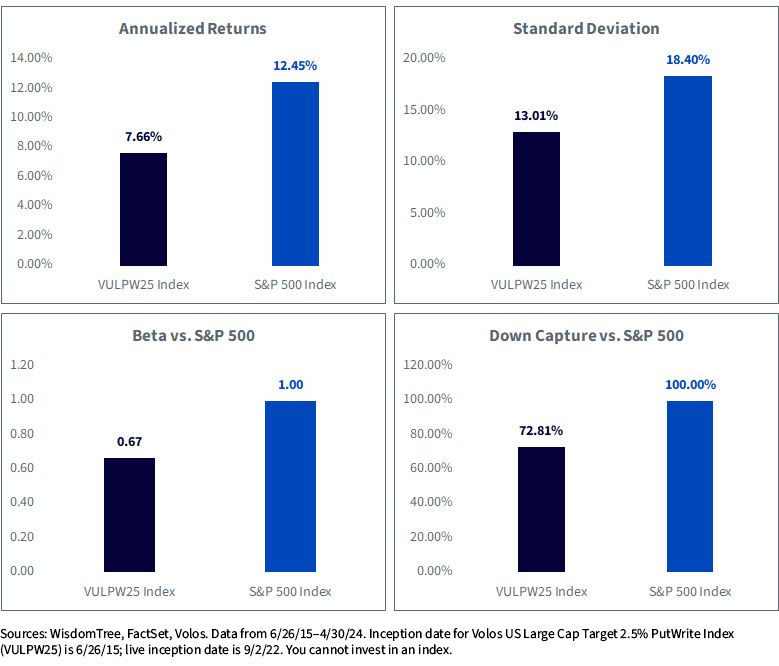

The below full-period statistics further illustrate this concept, showing how standard deviation is reduced by more than 5% while the strategy’s beta to the S&P 500 is 0.67 and downside capture is close to 73%.

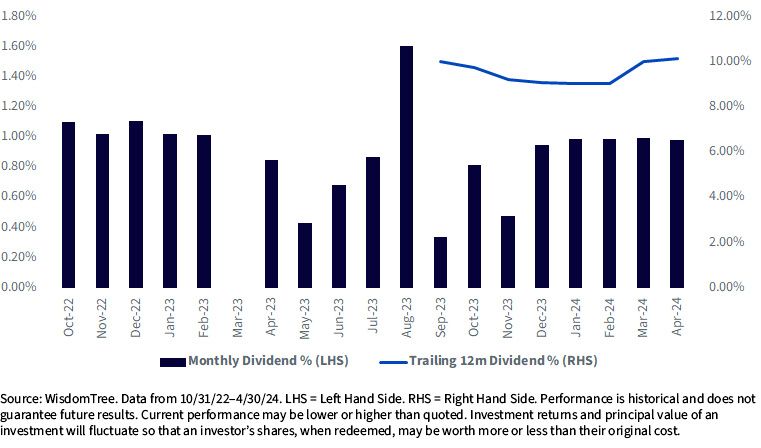

2. Income Generation: Since PUTW's restructuring in late 2022, the Fund has been focused on providing monthly distributions at a relatively stable level. These distributions have been classified as a combination of ordinary income and return of capital.

The Fund’s full standardized performance and SEC 30-day yield data, as of the most recent month-end, are available here.

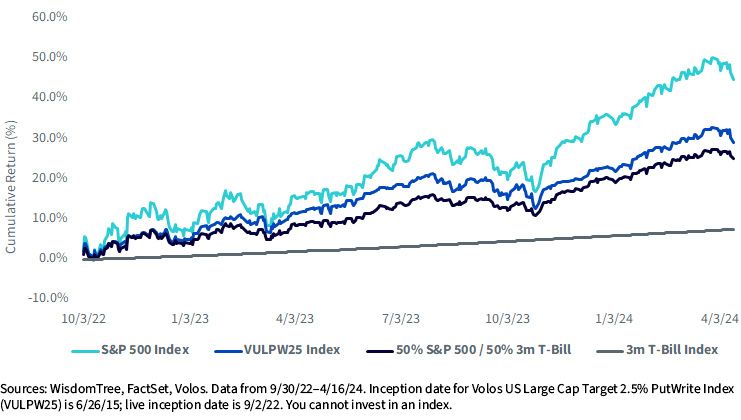

An investor seeking income could have other options for pursuing it, given current interest rates. One of those ways would be to fully invest in short-term Treasuries, the highest-paying node of the curve today (3m t-bill index). Another way to seek income while maintaining broad market exposure would be to split their position between the same short-term Treasuries and the broad market (50% S&P 500 Index/50% 3m t-bill). The investor who only holds short-term Treasuries would be earning roughly 5% in income, while the investor combining Treasuries with the S&P would be earning roughly 3.2%. As we can see in the chart below, VULPW25 has provided investors with a better total return experience than these two options since restructuring in October 2022.

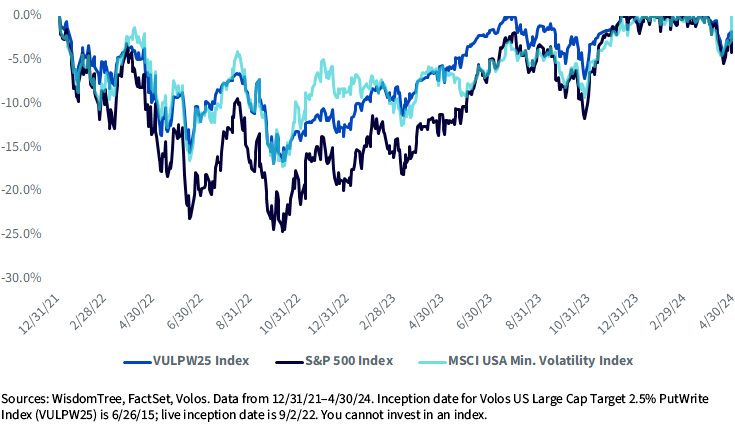

3. Less Active Stock Selection Risk When Targeting “Low Volatility” Exposure: When investors seek to diversify risk, a low- or minimum-volatility portfolio could be an option. Low-vol portfolios rebalance periodically, investing in securities and sectors that experienced the lowest volatility in a pre-defined lookback period. This does not mean these securities and sectors will behave the same way going forward. As can be seen in the maximum drawdown chart below, the construction of VULPW25 allows it to have defensive characteristics in periods of broad market drawdown like 2022, and it does so with less volatility than a low-volatility strategy like the MSCI USA Min. Volatility Index. But whereas low-vol portfolios take meaningful “active risk” versus the market, the option strategy can remain the same underlying portfolio by achieving lower risk through the option strategy.

If investors are expecting a more challenging environment than what we’ve seen over the last four years—one with very few market drawdowns—it is a worthwhile time to explore the characteristics of our option-writing ETF, PUTW.

1 Source: Morningstar. Growth of US Fund Derivative Income category from 3/31/23–3/31/24.

2 Source: WisdomTree. Data from 2/24/16–4/30/24.

There are risks associated with investing, including the possible loss of principal. The Fund will invest in derivatives, including S&P 500 Index put options (“SPX Puts”). Derivative investments can be volatile, and these investments may be less liquid than securities and more sensitive to the effects of varied economic conditions. The value of the SPX Puts in which the Fund invests is partly based on the volatility used by market participants to price such options (i.e., implied volatility). The options values are partly based on the volatility used by dealers to price such options, so increases in the implied volatility of such options will cause the value of such options to increase, which will result in a corresponding increase in the liabilities of the Fund and a decrease in the Fund’s NAV. Options may be subject to volatile swings in price influenced by changes in the value of the underlying instrument. The potential return to the Fund is limited to the amount of option premiums it receives; however, the Fund can potentially lose up to the entire strike price of each option it sells. Due to the investment strategy of the Fund, it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Equity Premium Income Fund

Head of Indexes, U.S.

Alejandro Saltiel joined WisdomTree in May 2017 as part of the Quantitative Research team. Alejandro oversees the firm’s Equity indexes and actively managed ETFs. He is also involved in the design and analysis of new and existing strategies. Alejandro leads the quantitative analysis efforts across equities and alternatives and contributes to the firm’s website tools and model portfolio infrastructure. Prior to joining WisdomTree, Alejandro worked at HSBC Asset Management’s Mexico City office as Portfolio Manager for multi-asset mutual funds. Alejandro received his Master’s in Financial Engineering degree from Columbia University in 2017 and a Bachelor’s in Engineering degree from the Instituto Tecnológico Autónomo de México (ITAM) in 2010. He is a holder of the Chartered Financial Analyst designation.