Navigating Inflation: The FOMC’s Single Mandate

Published May 23, 2024

Macro Strategist, Model Portfolios

Key Takeaways

- The current focus of the FOMC is on achieving the inflation mandate rather than the employment mandate.

- The FOMC is more concerned about the risk of inflation than the state of the labor market.

- Unemployment remains low and is not a major concern for the FOMC unless it rises substantially further.

The Federal Open Market Committee is always data-dependent. But the dependency is not always the same. There are times when inflation matters more than the labor market, and times when the situation is reversed. Every regime is unique. There is never a perfect corollary to a previous experience. This time is not different.

This time, it is a confidence game. One where the FOMC needs to be incrementally more confident about the trajectory of inflation. There is less—arguably, much less—focus on the state of the labor market. And that makes sense. The full employment mandate is not under the same pressure as the stable prices side. When confronted with a tilted risk outlook, the FOMC reacts to it. And, in the current monetary policy regime, ties it to data.

It is that data that matters. When the FOMC tells you what will cause it to move policy rates, it should not be ignored. It should be embraced. That makes the relevant question to every single data point, “Does this alter the FOMC’s inflation confidence?”

The short answer is, “Maybe?” The longer answer is, “Maybe.” It is all about confidence, and there is less confidence in achieving the inflation mandate than accomplishing the employment mandate.

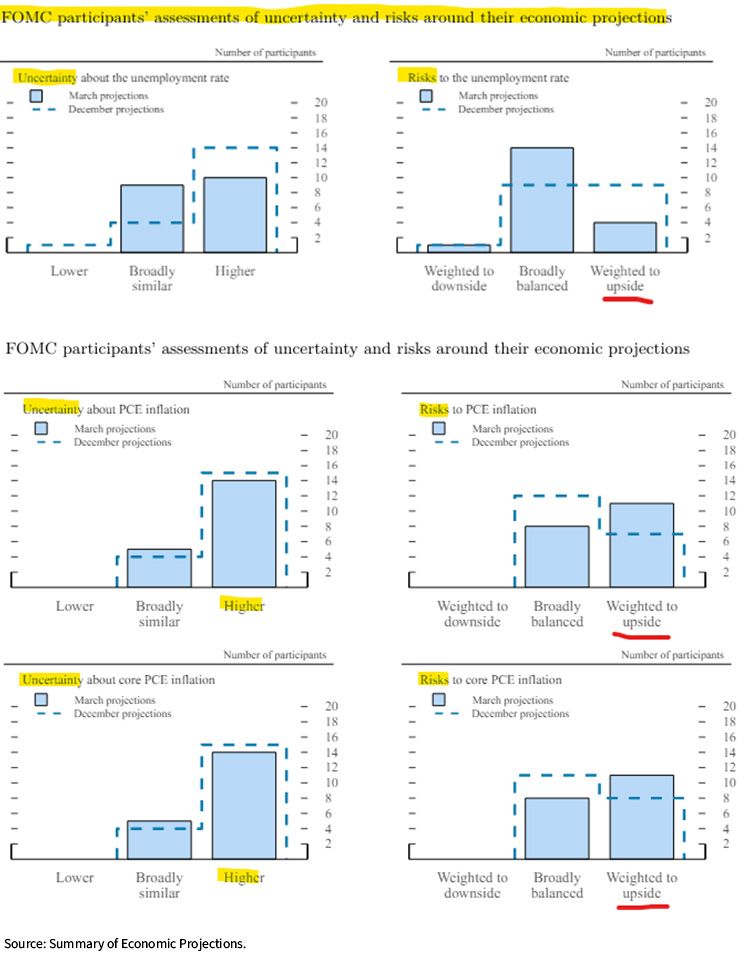

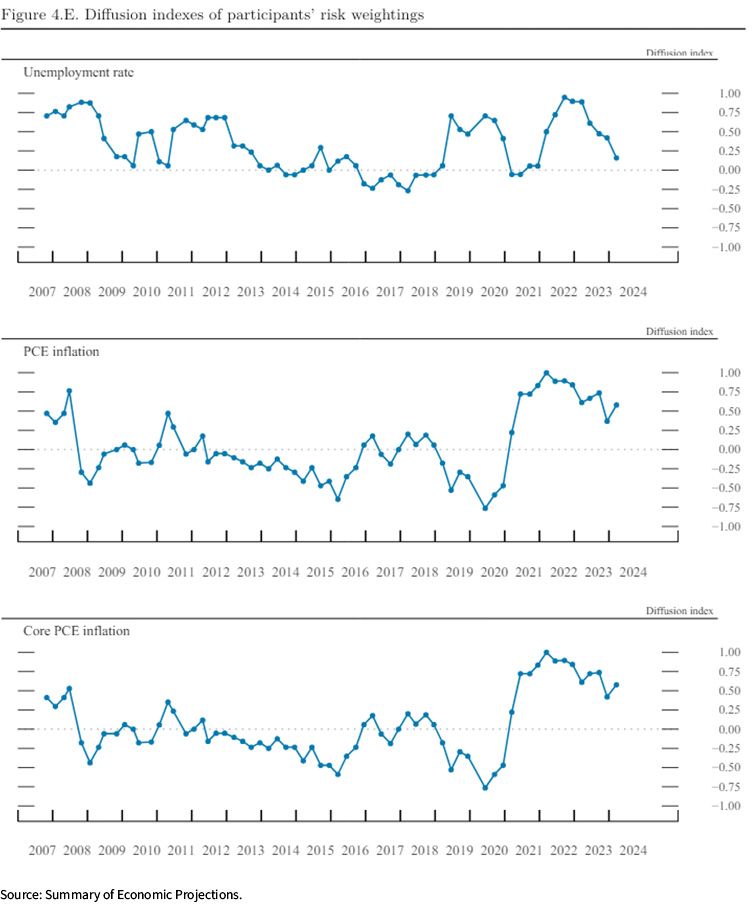

There is a reason for the outsized attention being paid to the inflation side of the mandate. There is more uncertainty and risk to the upside, according to the FOMC. The members of the policy setting committee are simply not concerned about the employment side. That creates a “tilt” in the policy framework toward inflation data and away from employment data.

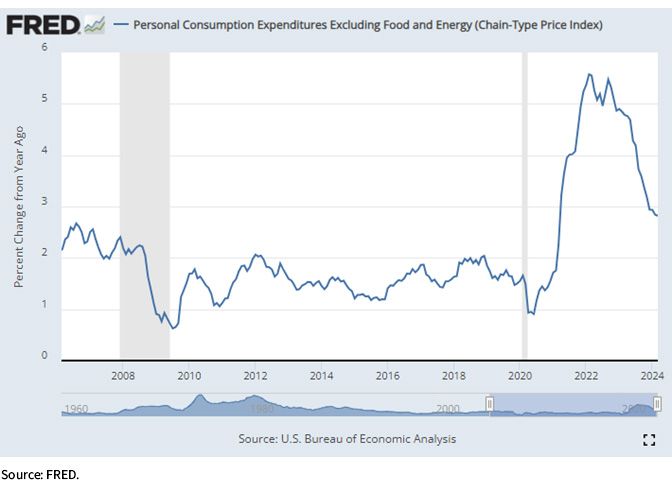

This dynamic is confusing. Prior to the current inflationary episode, the employment mandate was the “risk.” That is no longer the case. It is difficult to stress the importance of this development. In the wake of the global financial crisis, core PCE (the FOMC’s preferred gauge of inflation) consistently ran below the 2% target. At the time, the debate was about getting inflation higher, not lower.

That paradigm is no longer relevant. It is now all about accomplishing the mission of an inflation return to 2%. This is consistent with the long-term message from the FOMC, too. At the annual gathering of central bank officials in Jackson Hole, Powell gave a speech about the commitment to tackling the inflation problem, warning there could be pain ahead.

The pain has not materialized. Unemployment remains sub-4%, and the FOMC is unlikely to be concerned about unemployment unless it rises substantially further. How can we know this? The FOMC releases its “longer-run” view of the unemployment rate. Currently, unemployment sits at 3.9%. That is the bottom of the range for the Committee’s outlook this year (3.9%–4.1%). The longer-run range the FOMC would be happy with is 3.8% to 4.3%.

The inflation concentration is not something that needs to be implied. The FOMC is being rather open and blunt about it. Unemployment is not an issue, but inflation is. The “dual mandate” is now a single mandate.

Eventually, this will shift back to a more balanced mandate. But that will take persistently better news on inflation and negative news on the labor market. Much as one piece of positive news on inflation is not going to provide the FOMC with enough confidence to cut rates, one piece of negative employment news is not going to cause the FOMC to panic either. The single mandate is here. There is no reason to fight it.

Categories

About the contributor

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.