The WisdomTree Q2 Portfolio Review, Part One: Strategic Models

This article is relevant to financial professionals who are considering offering model portfolios to their clients. If you are an individual investor interested in WisdomTree ETF Model Portfolios, please inquire with your financial professional. Not all financial professionals have access to these Model Portfolios.

Well, FOOOF.… What a first quarter we just witnessed. Markets all over the place, the Fed all over the place, bank failures all over the place, DC politics all over the place, geopolitics all over the place—you name it. Yet, despite all that, markets were up fairly strongly, especially the NASDAQ. You certainly cannot blame investors for wondering what the heck they are supposed to do.

So how did the WisdomTree Model Portfolios hold up? Well, truth be told, it was a mixed bag—our factor “tilts” toward size, value and dividends did not help us amidst a resurgence toward growth and tech stocks as interest rates fell. But we held our own, which is saying something, and our quality tilt certainly helped us.

This is the first of a three-part quarterly blog series examining our portfolio performances and breaking each blog post into our categorizations of models: (1) Strategic; (2) Outcome-Focused; and (3) Collaboration.

Let’s dive in.

Equity

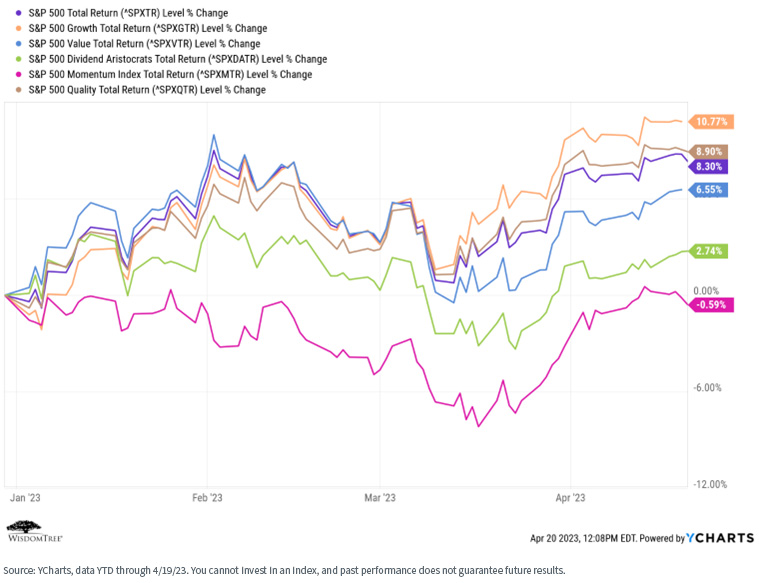

The first thing to note is that, as interest rates fell, growth and “mega-tech” stocks roared back in Q1 versus other asset classes and factors. We believe in risk factor diversification, so we weren’t completely left behind, but our tilts toward value, size and dividends certainly didn’t help us. What DID help us, however, is our persistent belief in both quality and overall risk factor diversification.

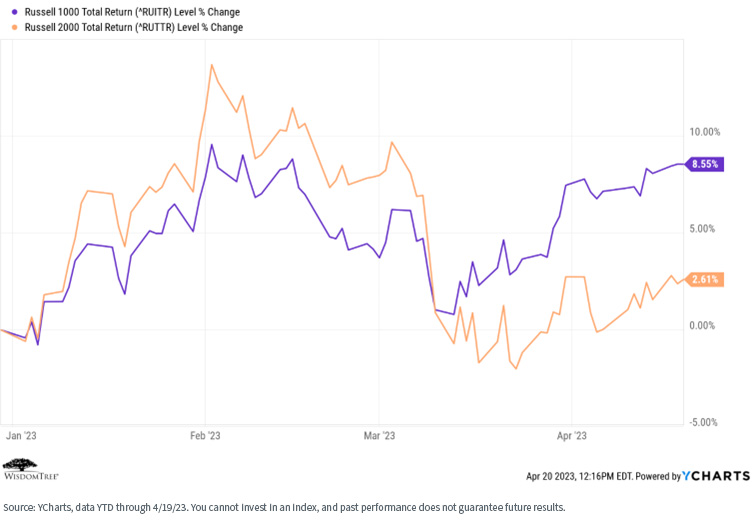

Our long-term belief in the size (small-cap) factor also did not help us, as investors grew increasingly afraid of a recession and migrated toward larger-cap stocks.

One thing that did help us, however, was our consistent tilt toward quality (firms with better balance sheets, earnings, cash flow and dividend sustainability)—a trend we believe will continue.

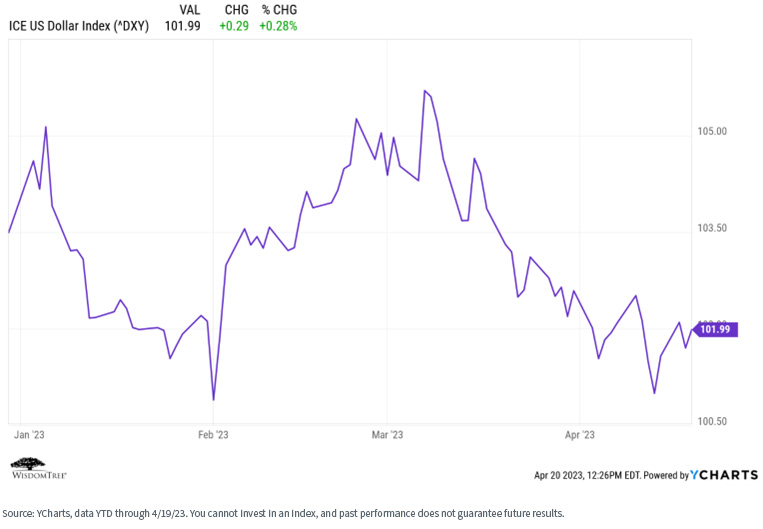

Another inherent thesis in our equity models is a belief in global diversification. This, too, worked for us in Q1, as both developed international and emerging markets outperformed the U.S., helped in part by a more or less declining dollar.

So, bottom line, our asset allocation and security selection positives could not overcome the tidal wave of growth and mega-tech resurgence, and we underperformed our benchmarks.

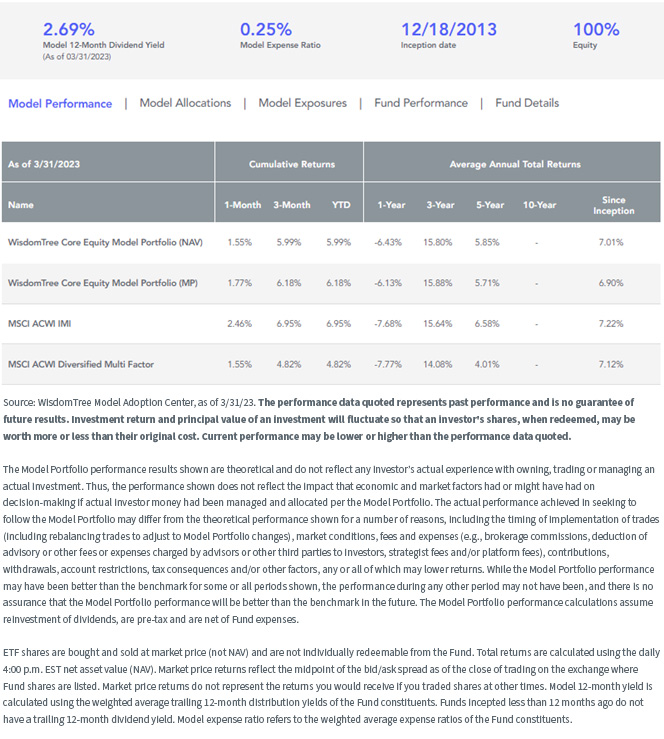

WisdomTree Core Equity Model Portfolio

For the most recent month-end performance, please click here.

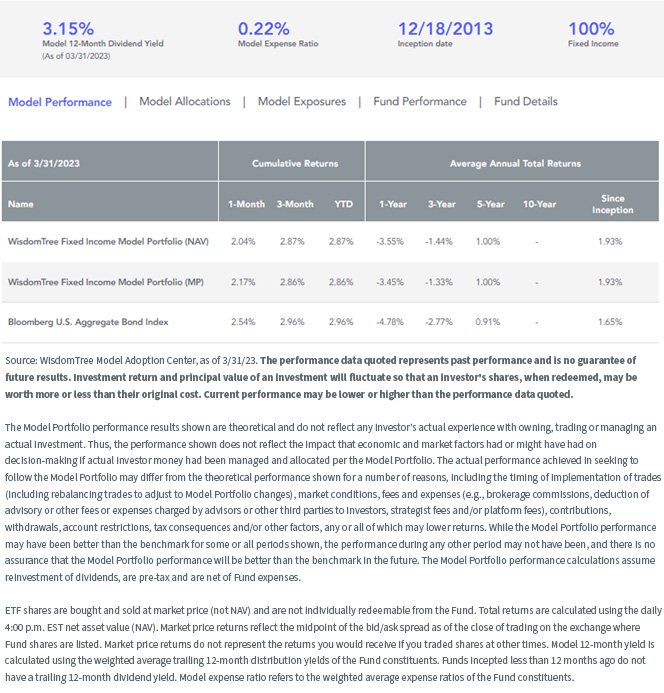

Fixed Income

For several years, our positioning within our fixed income model was to be under-weight in duration and over-weight in quality credit relative to the Bloomberg Aggregate Index.

This hurt us slightly in Q1 as rates fell and the duration trade paid off. But we are comfortable with where we are and believe our over-weight in quality credit will work for us in the medium to longer term.

WisdomTree Fixed Income Model Portfolio

For the most recent month-end performance, please click here.

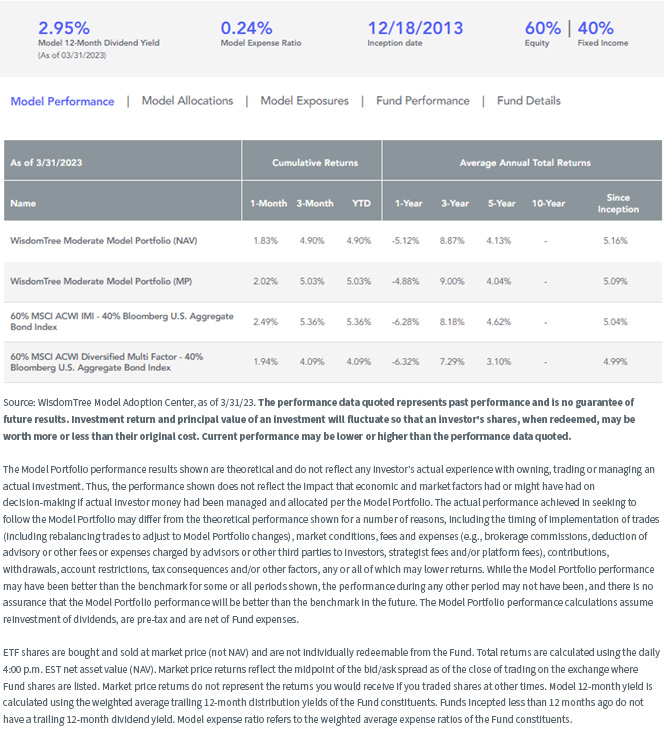

Well, if your core equity and fixed income models both underperformed, then your strategic allocation models, mixing varying combinations of the equity and fixed income portfolios, will also have underperformed. This is exactly what happened (using the “60/40” risk band as a proxy).

WisdomTree Moderate Model Portfolio

For the most recent month-end performance, please click here.

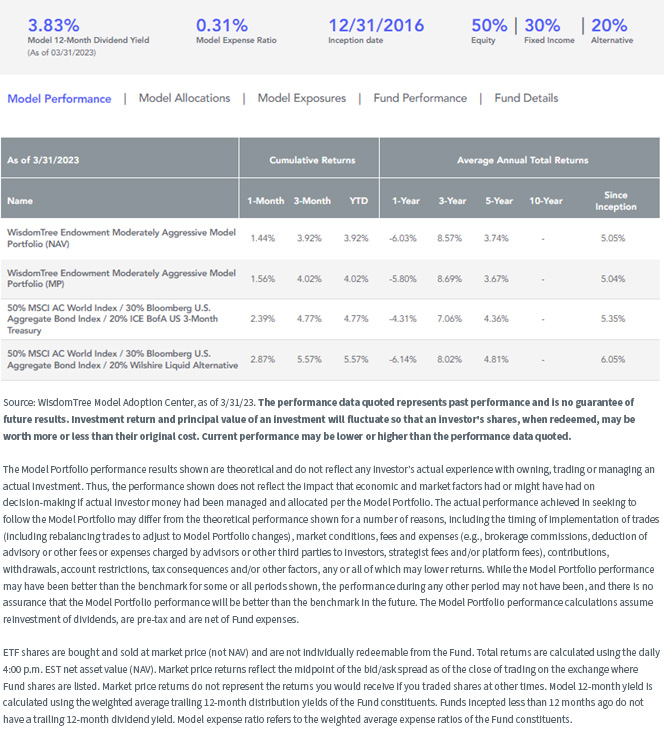

Endowment Model

Finally, a word about our endowment models, which combine stocks and bonds with an allocation to lower-correlated strategies such as real assets and alternatives. The thesis behind these models is that by incorporating lower-correlated strategies, advisors can deliver a more diversified portfolio experience, with the potential of delivering more consistent portfolio performance regardless of the market regime.

The idea is to take advantage of the power of compounding—if you don’t lose as much in down markets, you don’t have to gain as much in up markets to still come out ahead in the long run.

In Q1, our allocations to managed futures, MLPs, hedged equity and inflation-hedging strategies were positive but did not keep up with the large-cap growth rally in the S&P 500. Meanwhile, given that rally in the S&P, our allocation to a short-biased strategy did not help us.

Using our “moderately aggressive” endowment model as an example, as it is the closest allocation to the traditional 60/40 portfolio, we held our own but did not keep up with our benchmarks.

WisdomTree Endowment Moderately Aggressive Model Portfolio

For the most recent month-end performance, please click here.

Conclusion

We believe in transparency within our Model Portfolios, so we share our results, sometimes warts and all. Our strategic models did not keep up with their benchmarks in Q1, but we know why—our philosophical tilts are toward value, size, dividends and quality—and this is exactly what did not work best in Q1 (except quality).

But we believe in the long-term effectiveness of these tilts and further believe the rally in growth and mega-tech will be short-lived. There is some opinion that interest rates may fall over the short term as the Fed pivots back toward a more accommodative policy stance. But longer term, we believe rates will be range-bound or grind higher. We are strategic in nature but will move defensively if we see the need on a more tactical basis. Bottom line, we remain comfortable with our overall allocations.

In part two of this quarterly series, we will examine the performances of our outcome-focused models.

Financial advisors can learn more about these models and how to position them successfully with end clients at our Model Adoption Center.

Important Risks Related to this Article

For Financial Advisors: WisdomTree Model Portfolio information is designed to be used by financial advisors solely as an educational resource, along with other potential resources advisors may consider, in providing services to their end clients. WisdomTree’s Model Portfolios and related content are for information only and are not intended to provide, and should not be relied on for, tax, legal, accounting, investment or financial planning advice by WisdomTree, nor should any WisdomTree Model Portfolio information be considered or relied upon as investment advice or as a recommendation from WisdomTree, including regarding the use or suitability of any WisdomTree Model Portfolio, any particular security or any particular strategy.

For Retail Investors: WisdomTree’s Model Portfolios are not intended to constitute investment advice or investment recommendations from WisdomTree. Your investment advisor may or may not implement WisdomTree’s Model Portfolios in your account. WisdomTree is not responsible for determining the suitability or appropriateness of a strategy based on WisdomTree’s Model Portfolios. WisdomTree does not have investment discretion and does not place trade orders for your account. This material has been created by WisdomTree, and the information included herein has not been verified by your investment advisor and may differ from information provided by your investment advisor. WisdomTree does not undertake to provide impartial investment advice or give advice in a fiduciary capacity. Further, WisdomTree receives revenue in the form of advisory fees for our exchange-traded Funds and management fees for our collective investment trusts.

Share & Comment

Popular Posts

Categories

Related Links