Ooh-Ooh Child…

Ooh-Ooh child

Things are gonna get easier

Ooh-Ooh child

Things’ll get brighter

Someday, yeah

We'll put it together and we’ll get it undone

Someday

When your head is much lighter

Someday, yeah

We’ll walk in the rays of a beautiful sun

Someday

When the world is much brighter

(From “Ooh-Ooh Child” by the Five Stairsteps, 1970)

As many of us enter what seems like Day ∞ of self-quarantining or government-mandated shelter-in-place restrictions, we may well be wondering if our heads will ever be “much lighter” or we’ll once again “walk in the rays of a beautiful sun.”

Well, yes.

For some perspective, Ooh-Ooh Child was written in 1970, in the middle of a period of global upheaval—the Vietnam war, race riots, the destruction of inner cities, assassinations, terrorism and natural disasters (a cyclone in Bangladesh killed 500,000 people). And, gasp, it was the year the Beatles broke up! In other words, it was another time when many people wondered if things would, ever again, “get brighter.”

We are not minimizing the severity of, nor the pain and suffering caused by, the current coronavirus pandemic. We are simply making the point that we often find ourselves in the middle of hard times, but life goes on. We make no predictions on the length or magnitude of the virus’ influence on our economy and our lives, except one—it will end.

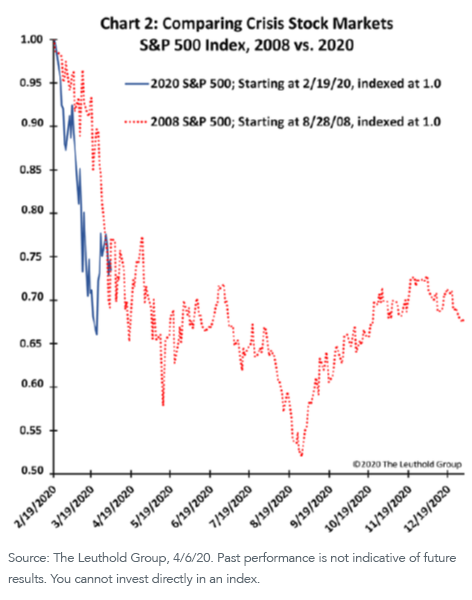

There is no question that the current market disruption is unprecedented. It has two unique characteristics: (1) the market decline has been dizzying in its rapidity and magnitude, and (2) it is the first “self-induced” economic and market recession in history. In the interest of our collective health and safety we voluntarily put the brakes on the global economy, and the market responded accordingly.

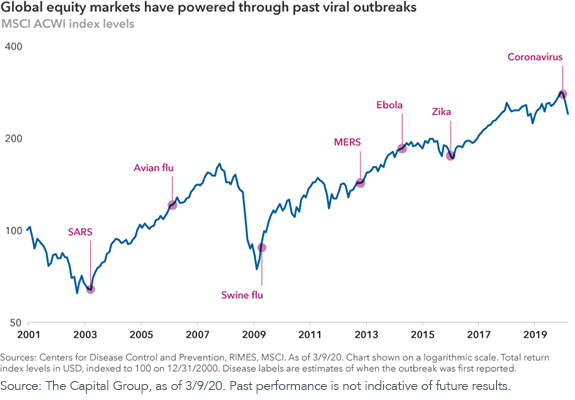

But, as we noted recently, we’ve been here before. As a reminder, consider the following chart. It is a snapshot of market performance since 2000, marked with historical global virus scares.

It must be noted that none of the prior “virus scares” had the global impact of the current Coronavirus, and the corresponding effects on the economy and the markets is unprecedented. Our broader point, simply, is that investing is a long-term endeavor, and the “journey” can sometimes be quite volatile.

If we accept that, as bad as things seem, they will eventually improve, then what should we do about it? Here is a short checklist of things to consider:

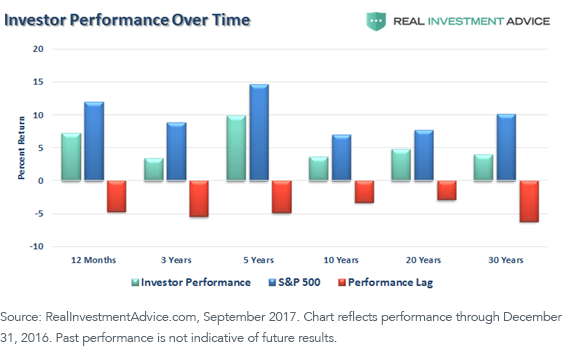

1. Remember to stay disciplined in your long-term investment plan. Investors, historically, have proven to be bad market-timers, and it has cost them significant long-term performance.

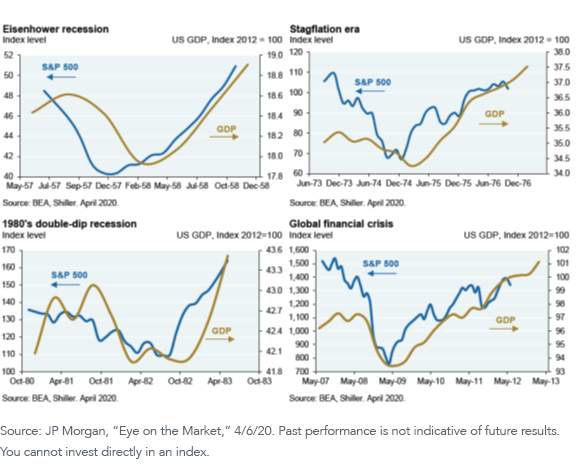

2. Remember that the stock market tends to be a leading indicator of economic recovery. Put differently, you need to be invested before the economy shows signs of turning around if you want to capture the full upside movement of the market.

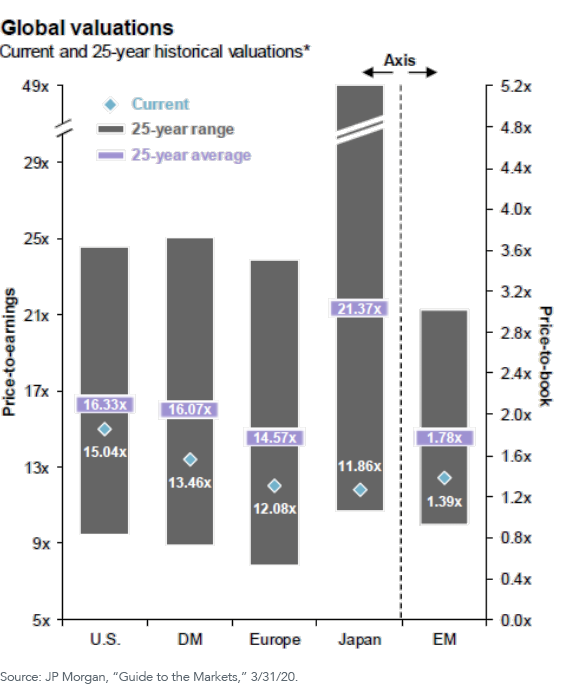

3. Remember that the long-term return potential of an investment is a function of how much you pay for it today. From a “glass half full” perspective, the market decline has brought valuations down to more attractive levels than we have seen in years.

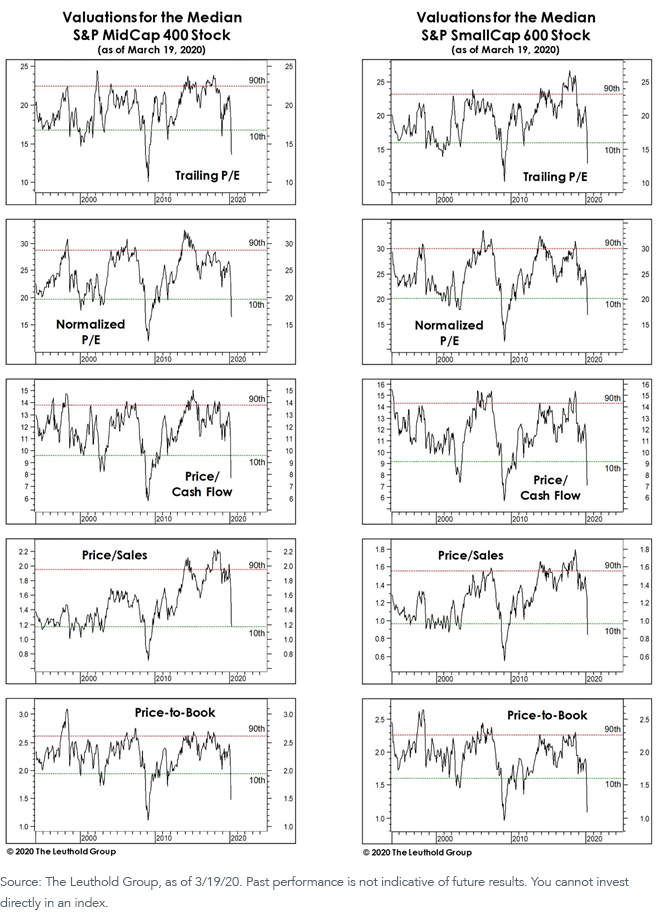

The dramatic decline in valuations makes U.S. mid caps and small caps look especially attractive.

4. When the markets do begin to recover, look to history for clues as to where there may be potential areas of relative outperformance. As we wrote in a recent blog, smaller-cap and dividend-paying stocks historically have outperformed as the market moves into recovery mode.

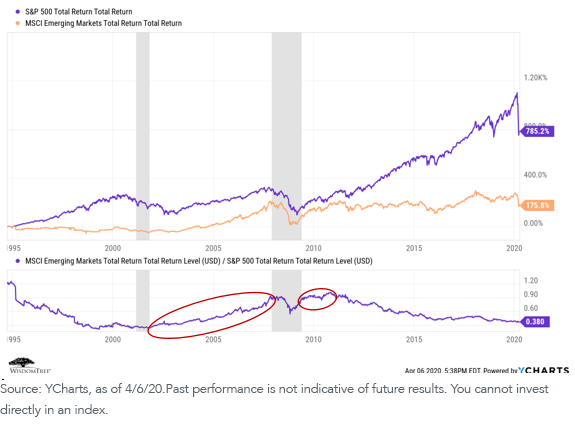

Another potential area to consider is emerging markets. While the U.S. market has outperformed the emerging markets on a cumulative basis over the past 25 years, the emerging markets outperformed as we rolled out of the past two recessionary market regimes (marked by the gray bars).

To summarize, even though we are in the middle of an economic and market storm, we still should keep our eyes on the longer-term horizon and plan accordingly. When this turmoil passes—and it will—there will be investment opportunities available.

In closing, it probably is not often that a Grateful Dead song is used in an investment context, but we think 1987’s Touch of Grey nicely captures where we likely will go from here:

The shoe is on the hand it fits, there’s really nothing much to it

Whistle through your teeth and spit ’cause it’s alright

Oh well, a touch of grey kinda suits you anyway

And that was all I had to say and it’s alright…

We will get by

We will get by

We will get by

We will survive…

Share & Comment

Popular Posts

Categories

Related Links