Clarifying Confusion: American Depository Receipts (ADRs) Have Currency Risk Despite Trading in the U.S.

Published September 26, 2012

Global Chief Investment Officer

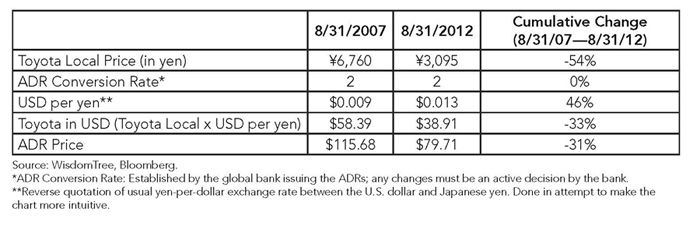

Lately, we have been talking with clients about one of our latest Funds, the Europe Hedged Equity Fund, which invests in a basket of European equities and then neutralizes, or hedges, the exposure to the euro. One common question we heard: “Can’t I just achieve the same thing by investing in a basket of European ADRs, which trade in the United States and thus do not have euro risk?” It is a common misconception that since the ADR is traded in U.S. dollars in the United States, there is no exchange rate risk. We believe it is very important to clarify that ADRs, despite trading in the U.S., do in fact contain the currency risk of the local markets. Here’s why. ADRs are created by a global bank that possesses a large number of an international firm’s local shares. The bank then sets a particular ADR conversion rate—meaning that an ADR share is worth a certain number of local shares. This conversion rate establishes the linkage between the ADR security and the locally traded security. To preserve this conversion relationship over time, movements in the exchange rate of home country vs. the U.S. dollar must automatically be reflected in the price of the U.S.-traded ADR in U.S. dollars. If this did not occur, it would be impossible to preserve the conversion rate established by the bank. • If the local price of the foreign security does not change, but the exchange rate measured versus the U.S. dollar declines by half, the U.S. traded ADR price would also decline by one-half. Conversely, this holds for gains in the exchange rate as well. Let’s analyze how this relationship worked for one Japanese company over the past five years. We selected the largest Japanese company by market capitalization1, Toyota, to illustrate this example, given that Japan is one of largest economies in the world and its currency, the yen, has appreciated by almost 50% relative to the dollar over the last five years. This makes a comparison of the cumulative movement in the ADR price for Toyota with the local stock price for Toyota a clear illustration of how currency moves are factored into the ADR price. While Toyota’s stock price has declined 54% cumulatively over the last five years on the local Japanese exchange, the ADR price has declined only 31%. Why? The yen’s exchange rate versus the U.S. dollar appreciated 46% over this period; the ADR’s decline was thus significantly mitigated by the yen’s appreciation. The ADR price approximates the ADR conversion rate (2.0 to 1) times the price of Toyota converted into U.S. dollars.2 You would not expect the ADR conversion relationship to be exact, because the ADRs are traded during U.S. hours, when the Japanese markets are closed. It should be clear from this example that Toyota’s ADRs trading in the United States were still impacted by the yen’s exchange rate, despite the ADR being traded in the United States.

Many assume that because ADRs trade in U.S. dollars in the United States, they eliminate currency risk. Because of the way ADRs are structured, they still contain currency risk, as we illustrated. In the example we used, currency helped investors in the ADRs. But currency can also take away from returns to investors in ADRs or other international equities. For those looking to hedge the currency risk within their foreign stocks, ADRs are no substitute for strategies that actually employ a specific currency-hedging program. 1Source: MSCI. 2Sources: MSCI, Bloomberg. The Toyota price in U.S. dollars equals the local price multiplied by the number of U.S. dollars per yen. This converts local price into U.S. dollar terms.

Important Risks Related to this Article

Holdings of WisdomTree Funds are displayed daily at wisdomtree.com.

Categories

About the contributor

Global Chief Investment Officer

Jeremy Schwartz has served as Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Behind the Markets podcast. Jeremy is a member of the CFA Society of Philadelphia.