DXJ

Japan Hedged Equity Fund

Published August 7, 2024

Global Chief Investment Officer

Head of Equity Strategy

Recent central bank actions and currency interventions have created shock volatility in the markets, leading to large-scale position selling across the world, but particularly in East Asia. On Monday, Japan’s Nikkei 225 dropped over 10%, one of its biggest moves since the 1987 crash. The market has largely stabilized as we write.

Japan has been one of our top long-term favorite markets. This short-term turmoil has brought an influx of questions as to whether we are still bullish, along with inquiries about how to handle the currency hedging question.

Our house view is that this sell-off is an attractive buying opportunity.

To summarize:

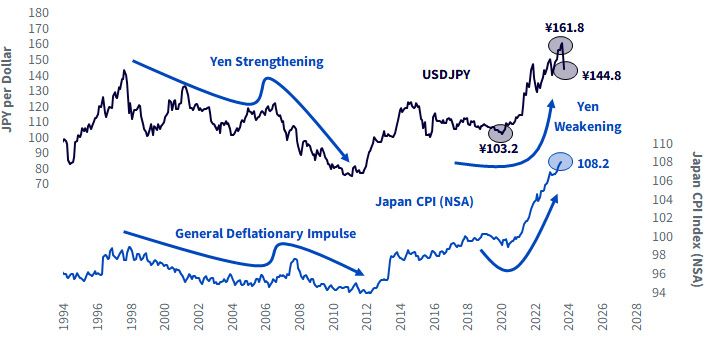

It is important to note that currencies trade on the future, not the present—and the future differential between U.S. and Japanese yields narrowed quickly. The yen snapped stronger in response.

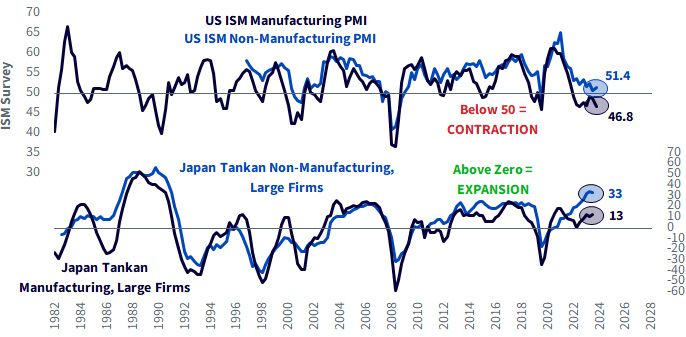

Sources: Refinitiv, ISM, Bank of Japan, as of July 2024 for the U.S., and Q2/2024 for Japan.

Sources: Refinitiv, Statistics Bureau, Ministry of Internal Affairs & Communication, Japan, as of June 2024 for CPI. JPY exchange rate as

of 8/6/24.

We believe Japanese equities crashed because leveraged market participants received margin calls, not because the fundamental outlook for Corporate Japan has changed.

Over the long run, currency risk brings added volatility and an extra bet that is not core to a long Japan thesis, which we think rests primarily on relative valuations.

The country has positive catalysts, namely the follow-through on corporate promises that we have been highlighting for years. The big one is the Name and Shame List, which identifies companies who have not fixed their profitability metrics. The Tokyo Stock Exchange threatened it, and many shook their heads and said it would never happen. Then voila, the TSE called those bluffs and published the list, right there on the home page of their website.

Additionally, we would be remiss if we didn’t give a hat tip to the country’s position as a friendly player in Washington. It offers something of a geopolitical tailwind in the event China’s hawkishness deepens or simply remains consistent. On the matter of Trump tariffs, this has been a known quantity for how many months, if not years? Markets move on surprises; a 10% tariff on Japanese exports is so well-telegraphed that it would surprise zero Japan watchers.

We believe a hedged-currency Japan position should outperform the S&P500 over the next five years.

Consider our arithmetic:

The S&P 500 is priced at 21 times earnings. The reciprocal is the earnings yield, which is less than 5%. Add expected inflation of 2%–3% to arrive at a medium-term return estimate for the S&P 500 of maybe 7%–8%.

Now Japan.

If we own equities with a currency hedge, which is the way most WisdomTree investors do it, the carry from the currency forward contracts is above 5%—at the moment. It is now “everyone’s” base case that the Fed and BoJ will change that, so let’s price in a slide in this gap between U.S. and Japanese short rates to something like 3% in 2025.

The WisdomTree Japan Hedged Equity Fund (DXJ), our flagship currency-hedged equity ETF, is priced at 10–11 times earnings. The reciprocal of that is the earnings yield, about 9%. Add the aforementioned carry of approximately 3% and the combination presents nominal returns from this exercise of more than 12%.

When comparing a country with a sub-11 forward P/E (Japan) and one whose P/E is 21 (the U.S.), we have to check for an earnings growth disparity. But we can’t find one, at least not a big one. The Street consensus is for Japanese corporate earnings to grow in the high single-digit area for the fiscal year ending March 2025. This is not far off FactSet’s 2024 S&P 500 earnings growth aggregation, which points to a 10.7% YoY rise.

In Japan’s case, we believe it is a misnomer that earnings estimates would be revised down from the yen’s sudden appreciation; many Japanese corporates were guiding earnings based on an exchange rate in the ¥142–144 range. It was trading there, then it bolted into the ¥160s—and now it has bolted back there once again. A round trip.

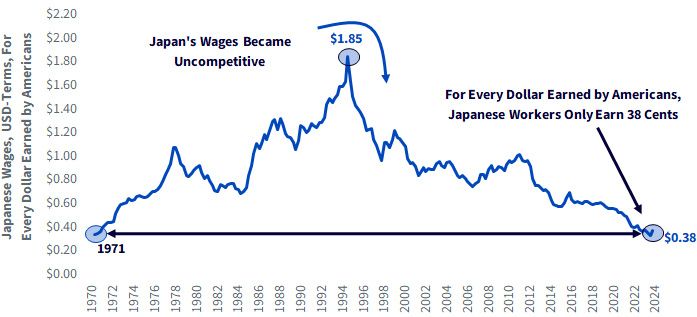

Additionally, we remain stunned at how little attention Japan’s cost of labor arbitrage receives in secular outlooks.

Using averages from the Organization for Economic Cooperation and Development (OECD) in U.S. dollar terms, Japan’s relative wages peaked in June 1995, when workers there earned 85% more than U.S. counterparts (Figure 3). In retrospect, the play back then would have been to sell Japan to buy U.S. equities, especially since the Netscape IPO that kicked off the U.S. tech mania occurred later that summer.

Today, the situation has strikingly changed. Japanese workers no longer earn $1.85 for every buck earned by Americans; they earn 38 cents.

Sources: Refinitiv, OECD, as of Q3/2024 with currency conversion as of 8/6/24.

Remember, we have been doing this for a couple decades, so at this point, WisdomTree has a large number of ETFs that currency hedge and a large number that do not. Which approach to take is often a matter of personal preference but allow us to share the Berkshire case study, which we think is helpful in making the choice.

The reader may be aware that Berkshire bought a half-dozen Japanese trading houses a couple years back. There were two paths that could have been taken with respect to the yen risk.

One was simple: Berkshire could have converted its massive USD cash stockpile (which currently amounts to $277 billion after Berkshire’s recent Apple sales) into JPY to buy the stocks. End of story. In so doing, Berkshire would have philosophically been aligned with something like DFJ, the WisdomTree Japan SmallCap Dividend Fund, which doesn’t hedge the currency.

But instead, Warren Buffett argued that neither he nor his deputies had any special insight into future forex moves. Berkshire instead tapped the market with JPY debt to finance the Japanese equity long. In so doing, Berkshire “went the DXJ route,” and took the yen part of the calculus out of the mix.

What we just witnessed was the worst three-day crash for Japan’s stock market since 1973. After the earlier crashes, the median subsequent 12-month stock market return was 10.9% and the average was 14.6% (Figure 4). This includes the miserable 1990 experience, when Japan’s bubble was bursting. If we draw a line through 1990, which we think is reasonable given the stock market’s bubble status at the time (compared to today’s 10–11 forward earnings multiple), that makes the lookback even more compelling.

As with many market crashes, buying after a panic is generally a profitable move.

Source: Refinitiv, 1/4/1973–8/6/2024, in JPY.

DXJ: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. Investments in currency involve additional special risks, such as credit risk, interest rate fluctuations and derivative investments, which can be volatile and may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

DFJ: There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Funds focusing their investments on smaller companies or certain sectors increase their vulnerability to any single economic or regulatory development. The Fund focuses its investments in Japan, thereby increasing the impact of events and developments in Japan that can adversely affect performance. This may result in greater share price volatility. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Chief Investment Officer

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.

Head of Equity Strategy

Jeff Weniger, CFA, is Head of Equity Strategy at WisdomTree, where he helps shape the firm’s stock market outlook by blending macroeconomic insights with fundamental analysis. With over a decade of experience in investment strategy, Jeff previously served as Director and Senior Strategist at BMO in the office of the CIO, contributing to the Asset Allocation Committee and co-managing ETF model portfolios across the U.S. and Canada. Notably, in 2013, at age 32, Jeff became the youngest member selected for BMO’s Global Investment Forum, joining the firm’s top strategists to craft its long-term investment outlook.