GCC

Enhanced Commodity Strategy Fund

Published May 8, 2024

Head of Indexes, U.S.

Associate Director, Quantitative Research at WisdomTree in Europe

For more than a decade after oil peaked in 2008, commodities exposures were akin to a dirty word because of poor performance that weighed on portfolios. Oil went negative with the COVID-19 pandemic, furthering pressure on commodity indexes, but inflation became a top-of-mind concern as pandemic relief measures were put in place and the economy reopened. Then Russia invaded Ukraine and sent commodity prices higher.

Bonds are no longer hedging stocks in multi-asset portfolios the way they used to because of elevated inflation concerns, causing investors to look for alternatives. We believe that commodities, being a driver and input to inflation, may be one of the most natural hedges for overall portfolios.

When WisdomTree reviewed many of the commodity indexes, we found a heavy concentration of risk, as many commodity strategies have as much as 50% exposure to Energy and three-quarters of the risk is attributed to that one sector. We set out to create a more diversified commodity strategy.

The WisdomTree Enhanced Commodity Strategy Fund (GCC) intends to provide broad-based exposure to four commodity sectors—Energy, Agriculture, Industrial Metals and Precious Metals—primarily through investments in futures contracts. The Fund may also invest up to 10% of its net assets in any combination of shares of one or more exchange-traded products that primarily hold bitcoin and in bitcoin futures contracts. The Fund will not invest in bitcoin directly.

GCC selects contracts on the futures curve, following a rules-based process, to minimize the implied cost of carry.

Investing in the first or second contract can be quite expensive, depending on the shape of the futures curve. Notably, when the curve is positively sloping or in contango (which has historically been the “normal” shape of futures curves), the so-called cost of carry can be a drag on performance. GCC optimizes performance by selecting the contract with the highest roll yield (or, conversely, the lowest cost of carry).

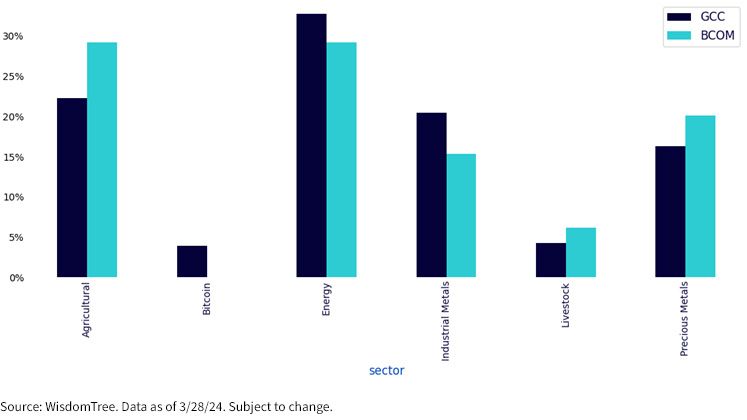

The chart above illustrates the allocation of the GCC and the Bloomberg Commodity Total Return Index (BCOM)—one of the primary benchmarks for broad commodities investing—as of the end of March. Notable differences characterize the GCC: it includes bitcoin, has significantly lower weightings in Agriculture and places greater emphasis on the Energy complex.

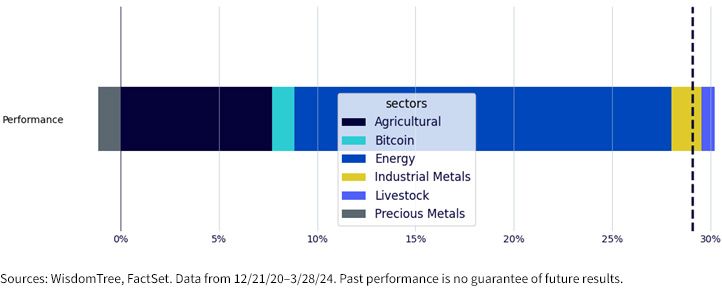

Above, we observe the performance contribution in absolute terms as of the end of March1. The Precious Metals sector has been the only detractor over the full period, while Energy dominates with an almost 20% relative contribution. From a historical perspective, the chart below shows the performance of GCC versus BCOM since the restructuring of the product.

Performance data for the most recent month-end and full standardized performance are available here.

In relative terms, we can broadly divide GCC's history versus BCOM into two distinct periods: from inception up to September 2022 and from September 2022 to date. In the first period, GCC underperformed BCOM, while in the second, it consistently narrowed the gap and almost closed it, demonstrating a remarkable recovery. Through the full period, GCC’s volatility has been 0.70% lower than BCOM’s. The main drivers for this behavior are as follows:

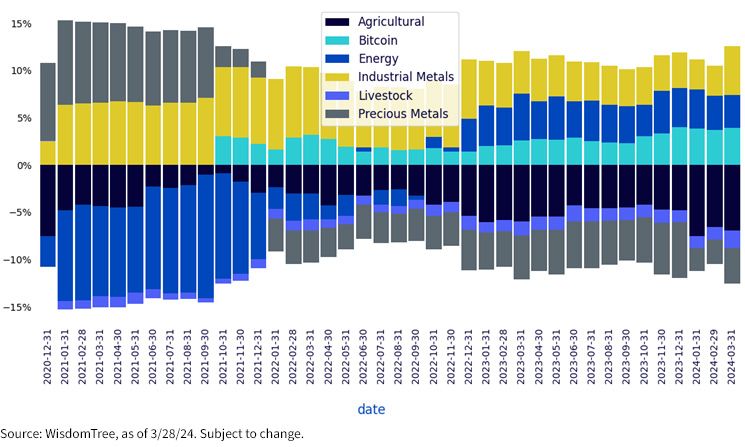

Relative commodity sector over-/under-weights through time can be seen in the chart below.

During the March rebalance, GCC shifted some of its allocations in reaction to moves in individual commodity prices and their curve positioning.

GCC funded a 2.5% position in Tin, in which it had previously been under-weight, by reducing exposure to Bitcoin and Cocoa futures after they experienced a significant run-up. GCC also transferred 1% from Corn to Cotton exposure, given the shape of their curves.

GCC continued to provide investors with a diversified commodity exposure and, despite important exposure deviations from the BCOM, has managed to keep up in terms of performance. We believe that investors who are looking for exposure in this uncorrelated asset class could benefit from GCC's lower relative volatility along with the systematic enhanced roll mechanism.

1 All the contributions refer to the excess return portion of the return, hence excluding the interest rate on the collateral.

An investment in bitcoin equity traded products (ETPs) involves significant risks and may not be suitable for all shareholders. The extreme volatility of trading prices that many digital assets, including bitcoin, have experienced in recent periods and may continue to experience could have a material adverse effect on the value of the shares, and the shares could lose all or substantially all of their value.

There are risks associated with investing, including possible loss of principal. An investment in this Fund is speculative, involves a substantial degree of risk and should not constitute an investor's entire portfolio. One of the risks associated with the Fund is the complexity of the different factors that contribute to the Fund's performance. These factors include the use of commodity futures contracts. In addition, bitcoin and bitcoin futures are a relatively new asset class. They are subject to unique and substantial risks and historically have been subject to significant price volatility. While the bitcoin futures market has grown substantially since bitcoin futures commenced trading, there can be no assurance that this growth will continue. In addition, derivatives can be volatile and may be less liquid than other securities and more sensitive to the effects of varied economic conditions. The value of the shares of the Fund relates directly to the value of the futures contracts and other assets held by the Fund, and any fluctuation in the value of these assets could adversely affect an investment in the Fund's shares. Because of the frequency with which the Fund expects to roll futures contracts, the price of futures contracts further from expiration may be higher (a condition known as “contango”) or lower (a condition known as “backwardation”), and the impact of such contango or backwardation may be greater than the impact would be if the Fund experienced less portfolio turnover. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Enhanced Commodity Strategy Fund

Head of Indexes, U.S.

Alejandro Saltiel joined WisdomTree in May 2017 as part of the Quantitative Research team. Alejandro oversees the firm’s Equity indexes and actively managed ETFs. He is also involved in the design and analysis of new and existing strategies. Alejandro leads the quantitative analysis efforts across equities and alternatives and contributes to the firm’s website tools and model portfolio infrastructure. Prior to joining WisdomTree, Alejandro worked at HSBC Asset Management’s Mexico City office as Portfolio Manager for multi-asset mutual funds. Alejandro received his Master’s in Financial Engineering degree from Columbia University in 2017 and a Bachelor’s in Engineering degree from the Instituto Tecnológico Autónomo de México (ITAM) in 2010. He is a holder of the Chartered Financial Analyst designation.

Associate Director, Quantitative Research at WisdomTree in Europe

Luca is an Associate Director in WisdomTree Europe's Research team, where he conducts quantitative research to enhance or develop new investment strategies, particularly in commodities and thematic equities. He also focuses on portfolio construction and optimisation. Before joining WisdomTree in 2022, Luca worked as a Quantitative Portfolio Manager at Euclidea SIM, a Milan-based fintech where he quantitatively managed multi-asset portfolios and developed and implemented statistical and machine learning models for investment strategies and fund selection. Luca holds a Master's degree in Finance from Bocconi University, Milan.