The Dollar Remains King

Published June 6, 2024

Macro Strategist, Model Portfolios

Key Takeaways

- The U.S. dollar has remained dominant as the king of currencies for the past 50 years, despite predictions of its impending downfall.

- The most important precondition for the U.S. dollar to lose its dominance would be the existence of a viable alternative currency, which currently does not exist.

- The threat of sanctions is a significant driver of the angst and rhetoric against the U.S. dollar’s dominance, as many countries lack access to the dollar and face consequences if they do not comply with sanctions.

And there is no apparent successor. For the better part of 50 years, there has been one prediction that has been persistently in the headlines and persistently wrong—the impending implosion of the U.S. dollar. The sheer dominance of the dollar makes it a clear target. Eventually, the U.S. dollar must share its crown as the king of currencies. Right?

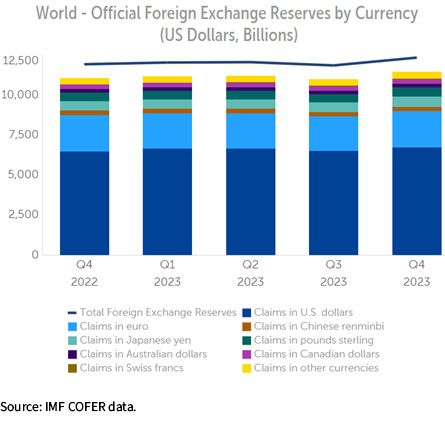

Maybe. But there are a few preconditions that are far from being met. The most important would be a viable alternative to the dollar. The Chinese yuan is frequently cited. It should not be. China has a closed capital account meaning there is a limited ability to transact in the currency. That precludes it from being a viable alternative to the dollar. In fact, China’s Belt and Road lent around $1 trillion in dollars not yuan. That is more signal than noise in the supposed “de-dollarization” narrative. There is a reason the dollar share of reserves has remained stable despite the threat of sanctions (more on that in a bit).

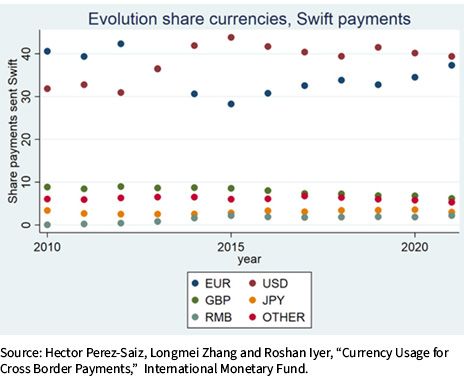

There is an important, often overlooked distinction between “transaction” and “reserve.” The dollar and euro compete for the crown as the transactional currency king. Everyone else competes for a distant third-place trophy.

But the headlines are incessantly calling for the impending downfall of the dollar system. Frequently, these talk about threats from Russia, Iran, North Korea, Venezuela and similar actors. The question that should be asked is, “So what”? Many of the countries saber rattling against dominance are doing so because they lack access to the dollar. Sanctions—and the threat of sanctions—are the primary driver of the angst and rhetoric.

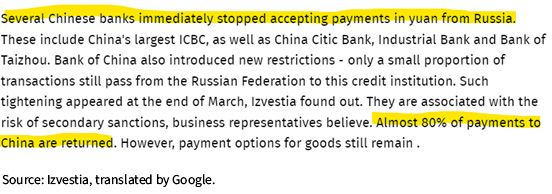

Sanctions are often underestimated. The above quote is a stark reminder of how powerful the threat of sanctions can be in the global financial system. Some of China’s larger banks are unwilling to accept payments in China’s own currency from Russia, because there is the real, tangible threat of being cut off from the broader financial system. Yes, there are ways to evade sanctions. Yes, Russia is pursuing those channels. No, it is not cheap or simple. It takes middlemen and haircuts to avoid sanctions, which raises prices and risks to both parties.

King Dollar is not at risk of losing its crown any time soon. There are always competing economic blocs. That will never change. Sometimes they matter more than others. But—for now—there is simply no other alternative to the dollar. Occasionally, hyperbolic headlines matter. This is not one of those times.

Categories

About the contributor

Macro Strategist, Model Portfolios

Samuel Rines is a Macro Strategist at WisdomTree, where he extends the firm's custom model portfolio management capabilities. Before joining WisdomTree in 2024, he was the Managing Director at CORBU, LLC, leading the PolyMacro advisory product. With over a decade of experience in economics and finance, Samuel has held significant roles such as Chief Economist at Avalon Investment & Advisory and Economist and Portfolio Manager at Chilton Capital Management LLC. He is also the author of "After Normal: Making Sense of the Global Economy," and holds a Master’s degree in Economics from the UNH Peter T. Paul College of Business and Economics, as well as having studied Economics at the University of Oxford.