The Bitcoin Halving Is Upon Us

Published April 22, 2024

Christopher Gannatti, CFA

Global Head of Research

Blake Heimann

Senior Associate, Quantitative Research

Key Takeaways

- The bitcoin halving event occurs roughly every four years, reducing the newly issued bitcoin supply by half. This has historically been associated with a rising price.

- The halving reduces the block reward for miners, but our focus remains on sources of potential increased demand across the bitcoin network, especially given all the publicity in the space during 2024.

- Bitcoin's transparent and immutable monetary policy, along with its alternative investment exposure, could make it an attractive option for investors seeking a potential long-term store of value.

The bitcoin “halving” (or “halvening,” as some say) is an event that takes place in the bitcoin network roughly every four years. Newly issued (or mined) bitcoin is cut in half, reducing oncoming supply. At a point near the year 2140, the total supply of 21 million bitcoins will be mined, and no more new supply will become available to the market. Economics 101 would say that, holding demand constant, this tightening of supply would lead to higher prices—which is what has been observed in past events such as this. Will this be the case once again?

Concepts Underpinning the Halving

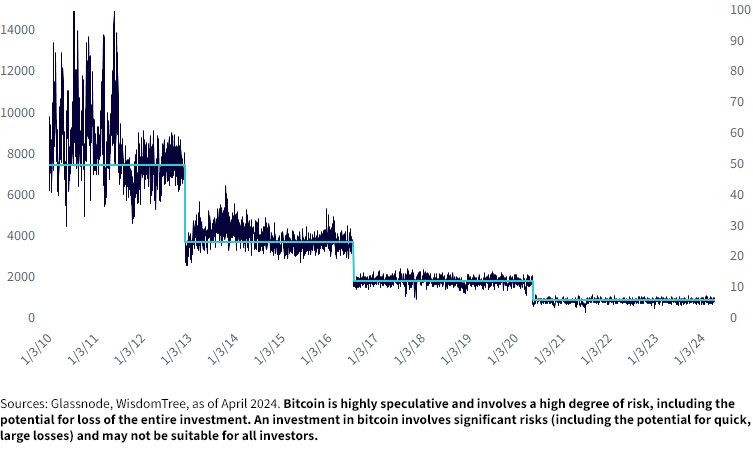

Approximately every 10 minutes, a new block is added to the bitcoin blockchain, recording transactions on the bitcoin network from across the globe. Someone, or some computer, needs to add these blocks to the blockchain. This is the responsibility of bitcoin miners. As they compile transactions into blocks, validating their accuracy in the process and adding these blocks to the blockchain, there is an incentive for them to do so. This incentive comes in the form of the “block reward,” or a newly minted bitcoin, which serves as payment for their efforts. Every 210,000 blocks, which equates to roughly every four years, this block reward is cut in half. As a result, miners get paid less bitcoin to do the same activities, and the newly minted bitcoin coming into circulation is reduced. Daily revenues paid to miners and the prevailing block reward can be seen in Figure 1, with the halving events reflected by the downward steps in the block reward.

Figure 1: Block Rewards and Bitcoin Miner Revenue (BTC)

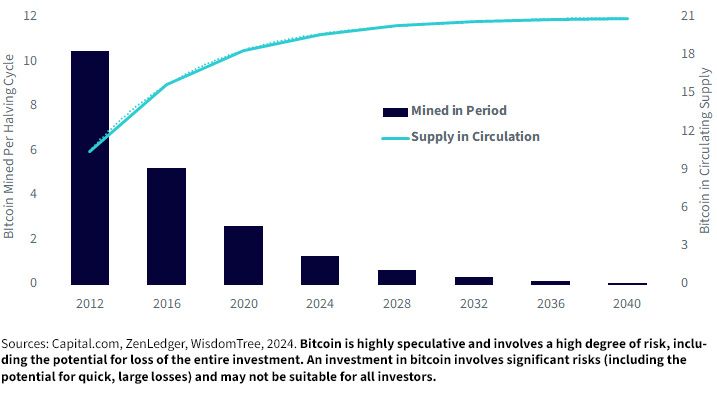

Subsequently, each halving cycle has a fixed amount of bitcoin issuance as a function of the block reward (210,000 blocks x block reward = newly minted bitcoins paid to miners). Halving events repeat until the block reward, and therefore new issuance, becomes negligible. At that point, no new supply comes online, and the prevailing supply is all that will ever be—21 million bitcoins. This can be verified in the code in two places: in the function defining block rewards and in the function explicitly setting the max. These supply dynamics can be seen in Figure 2. Interestingly, the mining process will be ongoing for roughly 100 calendar years, even though the vast majority of the supply will have already been created by 2040.

Figure 2: Bitcoin Mined per Halving Cycle and Circulating Supply, Millions

Implications for Investors

The broad implications of the halving are threefold:

- Reduced bitcoin-denominated payment for miners (reduced block reward)

- Reduced supply coming online, with a max supply of 21 million, which is estimated to be achieved in the year 2140

- An alternative, transparent monetary policy providing an opportunity for an alternative investment exposure

Put simply, bitcoin monetary policy is very different from the monetary policies employed by global governments, which can print as much money as they desire at any time.

The first implication is that holding all else constant, including bitcoin price in USD terms, it can lead to pressure on miners as their input costs come in the form of energy to run the computers doing the work of adding these blocks to the blockchain. If the USD price doesn’t remain above input costs, poorly capitalized bitcoin mining companies may be forced to consolidate, restructure or shut down. Investors with bitcoin mining equity exposure may want to be mindful of this dynamic as we see the price of bitcoin evolve over the coming weeks.

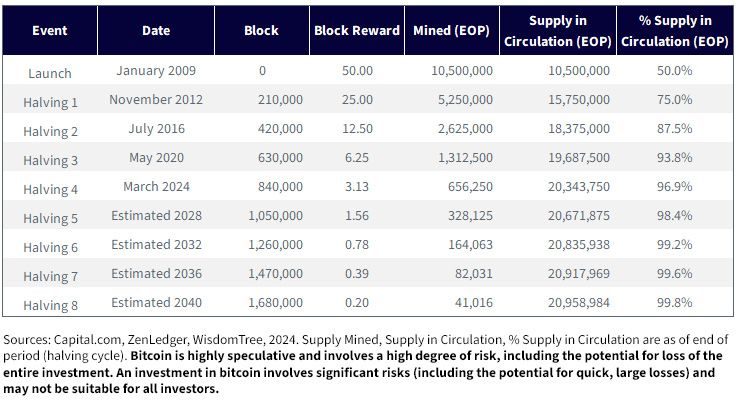

The second implication is to reiterate the overall reduction in bitcoin supply coming into circulation. With only so many blocks processed per day, the miner is rewarded with less newly minted bitcoin for each block. With the current iteration of the halving, these block rewards have been reduced from 6.25 to 3.125 bitcoins, marking a point in time where 19.7 million bitcoins (or nearly 94% of supply) are in circulation. Since these rewards are halved regularly, the overall newly minted bitcoin reduces until we eventually reach 0 for a block reward and a maximum circulating supply of 21 million bitcoins.

The third serves as a reminder of the transparent and immutable monetary policy implemented through the bitcoin software. There is no question about if and when these reductions in issuance take place, nor is there a group of leaders such as central bank policy makers reacting to the data to determine the best policy actions going forward. The bitcoin network is global, operating 24 hours a day, 365 days a year. Use cases of the network may differ depending on where an individual is based and whether that person’s home currency is more stable (think U.S. dollar, Swiss franc, euro, Japanese yen, British pound) or less stable (Turkish lira, Argentinian peso, Nigerian naira).

Is It Too Late?

Given recent performance, investors reading this may wonder if it is too late to consider bitcoin in weighing the applicable risks. Many institutions are only just beginning to allocate or evaluate such investments, meaning bitcoin’s total market capitalization has reached a point of USD 1.3 trillion1. With a significant portion of global capital not yet deployed in this space, it is still early days. We saw this with the introduction of the spot bitcoin ETFs in the U.S.

Figure 3: Bitcoin Halving Cycle Details

To give Figure 4 some additional detail and clarification :

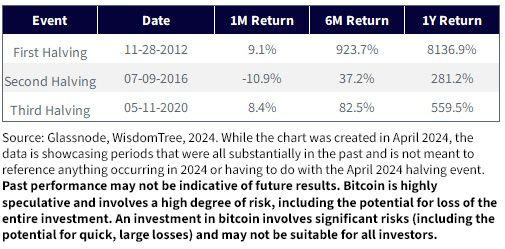

- First Halving: The date of the Halving event was November 28, 2012. 1M is from the halving date to December 28, 2012, 6M is from the halving date to May 28, 2012 and 1Y is from the halving date to November 28, 2013. The price of 1-bitcoin on the halving date was $12.30, whereas 1M forward it was $13.42, 9.1% higher than on the halving date. 6M forward it was $125.87, which was 923.7% higher than on the halving date. 1Y forward it was $1,012.81, which was 8,136.9% higher than on the halving date.

- Second Halving: The date of the Halving event was July 9, 2016. 1M is from the halving date to August 9, 2016. 6M is from the halving date to January 9, 2017. 1Y is from the halving date to July 9, 2017. The price of 1-bitcoin on the halving date was $657.32. The price 1M forward was $585.99, which was 10.9% below that of the halving date. The price 6M forward was $901.68, which was 37.2% above that of the halving date. The price 1Y forward was $2,505.72, which was 281.2% above that of the halving date.

- Third Halving: The date of the Halving event was May 11, 2020. 1M is from the halving date to June 11, 2020. 6M is from the halving date to November 11, 2020. 1Y is from the halving date to May 11, 2021. The price of 1-bitcoin on the halving date was $8,599.78. The price 1M forward was $9,324.48, which was 8.4% above that of the halving date. The price 6M forward was $15,693.91, which was 82.5% above that of the halving date. The price 1Y forward was $56,714.09, which was 559.5% above that of the halving date.

Figure 4: Historical Halving Events

It will be interesting to see how things play out in the coming weeks. This halving is the first that has seen such widespread media coverage—notably traditional financial news outlets like Bloomberg and CNBC—as well as increased access through widely available ETF offerings, improving ease of access and institutions coming onboard.

1 Sources: Capital.com, ZenLedger, WisdomTree, 2024. Supply Mined, Supply in Circulation, % Supply in Circulation are as of end of period (halving cycle).

2 Source, as is referenced under the chart, is Glassnode, in that we use Glassnotes data to pull in the relevant points for the numbers shown.

Important Risks Related to this Article

Crypto assets, such as bitcoin and ether, are complex, generally exhibit extreme price volatility and unpredictability, and should be viewed as highly speculative assets. Crypto assets are frequently referred to as crypto “currencies,” but they typically operate without central authority or banks, are not backed by any government or issuing entity (i.e., no right of recourse), have no government or insurance protections, are not legal tender and have limited or no usability as compared to fiat currencies. Federal, state or foreign governments may restrict the use, transfer, exchange and value of crypto assets, and regulation in the U.S. and worldwide is still developing.

Crypto asset exchanges and/or settlement facilities may stop operating, permanently shut down or experience issues due to security breaches, fraud, insolvency, market manipulation, market surveillance, KYC/AML (know your customer/anti-money laundering) procedures, noncompliance with applicable rules and regulations, technical glitches, hackers, malware or other reasons, which could negatively impact the price of any cryptocurrency traded on such exchanges or reliant on a settlement facility or otherwise may prevent access or use of the crypto asset. Crypto assets can experience unique events, such as forks or airdrops, which can impact the value and functionality of the crypto asset. Crypto asset transactions are generally irreversible, which means that a crypto asset may be unrecoverable in instances where: (i) it is sent to an incorrect address, (ii) the incorrect amount is sent or (iii) transactions are made fraudulently from an account. A crypto asset may decline in popularity, acceptance or use, thereby impairing its price, and the price of a crypto asset may also be impacted by the transactions of a small number of holders of such crypto asset. Crypto assets may be difficult to value, and valuations, even for the same crypto asset, may differ significantly by pricing source or otherwise be suspect due to market fragmentation, illiquidity, volatility and the potential for manipulation. Crypto assets generally rely on blockchain technology, and blockchain technology is a relatively new and untested technology that operates as a distributed ledger. Blockchain systems could be subject to internet connectivity disruptions, consensus failures or cybersecurity attacks, and the date or time that you initiate a transaction may be different than when it is recorded on the blockchain. Access to a given blockchain requires an individualized key, which, if compromised, could result in loss due to theft, destruction or inaccessibility. In addition, different crypto assets exhibit different characteristics, use cases and risk profiles. Information provided by WisdomTree regarding digital assets, crypto assets or blockchain networks should not be considered or relied upon as investment or other advice or as a recommendation from WisdomTree, including regarding the use or suitability of any particular digital asset, crypto asset, blockchain network or any particular strategy.

Categories

Related articles

About the contributors

Christopher Gannatti, CFA

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Blake Heimann

Senior Associate, Quantitative Research

Blake Heimann joined WisdomTree in 2020 and, in his current role as Senior Associate, supports the creation, maintenance, and reconstitution of our indices. Blake began his career in finance in 2017 as an Analyst at TD Ameritrade, and later a Quantitative Analyst with focuses on research and development of machine learning applications in finance. Blake has bachelor’s degrees in Mathematics and Economics from Iowa State University, as well as his Masters in Computer Science at Georgia Tech, with a specialization in Machine Learning. He is currently pursuing a Masters in Finance from the London School of Economics.