USSH

1-3 Year Laddered Treasury Fund

Published August 7, 2024

Head of Investment and Fixed Income Strategy

It has certainly not been a slow start for the dog days of August in the money and bond markets. The combination of a dovish Fed Chair Powell post-FOMC presser and cooling labor market setting provided more fuel for Fed rate cuts. In fact, post-jobs, the debate is no longer centered on the number of potential easing moves for the remainder of 2024, but rather on how large they could possibly be. That brings us to part two in my Money in Motion series: how to play along more directly with Fed rate cuts.

Before we get to the solutions portion of this blog post, let’s first provide some insights. There is a belief that whatever happens to the Fed Funds Rate will then be passed along to the Treasury yield curve in a similar fashion. While directionally, the idea of the Fed Funds Rate and UST yields moving up or down in tandem is somewhat accurate, the magnitude and timing of the changes tend to be less straightforward.

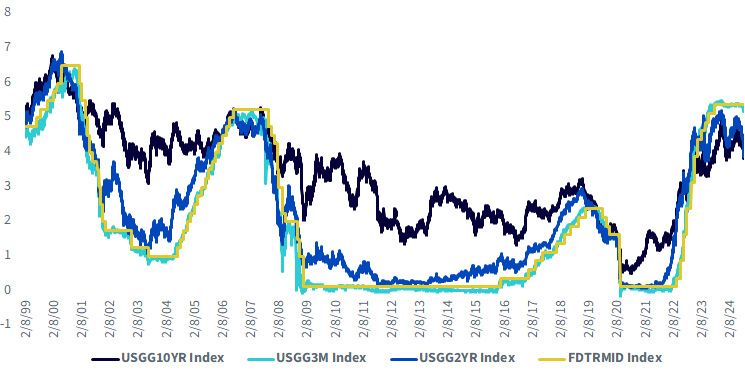

Source: Bloomberg, as of 8/2/24. For definitions of indices in the chart above, please visit the glossary.

Obviously, one begins with the Fed Funds target range, which represents overnight money. As a result, the closer the maturity is to Fed Funds, the more positive the correlation is going to be. The above graph highlights the relationship over the past 25 years between the mid-point of the Fed Funds target range and the UST 3-month t-bill, as well as the UST 2-Year and 10-Year note yields. The UST floating rate note could also be considered in this analysis given the fact that it “floats,” or is referenced, to the weekly UST 3-month t-bill auction.

As you would expect given my above statement, the correlation between Fed Funds and the 3-month t-bill is extraordinarily tight, while the relationship with the 2-Year note is also very positively correlated. However, the positive correlation begins to lessen considerably the further one goes out on the yield curve as illustrated by the spread between Fed Funds and the UST 10-Year note. While directionally these two rates tend to move in a similar way, the correlation in yields is noticeably lower when compared to maturities that are closer to Fed Funds.

Intuitively, this makes perfect sense. A maturity structure that is not too far removed from the Fed Funds Rate will be anchored and directly linked to trends in overnight money (Fed rate hikes/cuts). But, as you continue to move away from this anchor, other factors besides the Fed begin to come into play, and thus, investors demand a “term premium,” or an additional return or yield for the potential risk incurred by holding a security that is longer-term in maturity. In addition, inflation and future economic expectations also play a role.

While market talk for a 50 basis point rate cut from the Fed in September is now increasing, based on Powell’s comments post-FOMC and the policy statement, I would say this was the type of jobs report the Fed needed to first confirm a cut of any kind. This puts Powell’s Jackson Hole (August 22–24) appearance squarely front and center for rate cut forward guidance. Although rate cuts are now definitively a base-case scenario, what they ultimately look like will remain a fluid consideration.

Against this backdrop for rate cuts, WisdomTree offers two solutions that investors can use to potentially take advantage of this scenario, which should be very correlated to changes in the Fed Funds trading range.

USSH: There are risks associated with investing, including the possible loss of principal. Because the Fund is new, it has no performance history. U.S. Treasury obligations may provide relatively lower returns than those of other securities. Changes to the financial condition or credit rating of the U.S. government may cause the value to decline. Fixed income securities are subject to interest rate, credit, inflation and reinvestment risks. Generally, as interest rates rise, the value of fixed income securities falls. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

QSIG: There are risks associated with investing, including the possible loss of principal. Fixed income investments are subject to interest rate risk; their value will normally decline as interest rates rise. Fixed income investments are also subject to credit risk, the risk that the issuer of a bond will fail to pay interest and principal in a timely manner or that negative perceptions of the issuer’s ability to make such payments will cause the price of that bond to decline. While the Fund attempts to limit credit and counterparty exposure, the value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile. Prior to 7/08/24, the Fund’s ticker symbol was SFIG. The Fund’s name, objective and strategy were not affected at that time.

Head of Investment and Fixed Income Strategy

Kevin serves as the Head of Investment and Fixed Income Strategy. In this role, he writes macro and fixed income-related content and works closely with the sales, research and marketing teams. In addition, Kevin conducts client-facing webinars and meetings, providing expertise on WisdomTree’s existing and future bond ETFs. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S. in Finance from Fairfield University.