Looking Back at Equity Factors in Q4 2024 with WisdomTree

Published January 28, 2025

Head of Research, WisdomTree Europe.

Key Takeaways

- Growth stocks led equity markets in Q4 2024, particularly in the U.S., despite elevated valuations that spark sustainability concerns.

- Emerging markets struggled with an 8% decline, weighed down by trade tensions and weak economic signals from China, while European equities faced political instability.

- As growth continues its dominance, investors may want to consider diversifying across factors like value and quality to navigate potential micro factor rotations in 2025.

Looking back to 2024, global equity markets remained resilient despite a challenging final few weeks. U.S. equities led both annually and quarterly, buoyed by robust corporate earnings, supportive fiscal policies and market optimism following the Republicans’ red sweep in November. In contrast, European and emerging markets exhibited more modest performances, influenced by political uncertainties.

From a factor perspective, growth stocks maintained their leadership, particularly within the U.S. market. However, concerns regarding elevated valuations persist, prompting discussions about the sustainability of this trend.

This installment of the WisdomTree Quarterly Equity Factor Review examines how equity factors behaved during the fourth quarter and their potential impact on investors’ portfolios.

Performance in Focus: Back to Growth

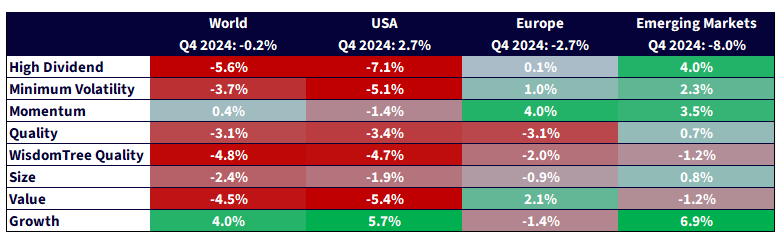

Equity markets stalled in the latter half of Q4 2024 after a strong start, leading to negative performances across most regions. The MSCI Emerging Markets Index declined by 8%, as trade war concerns and a weak Chinese economy weighed on sentiment. Political instability in South Korea and Europe, notably in France and Germany, contributed to the MSCI Europe Index's 2.7% loss. U.S. equities proved most resilient, supported by Donald Trump’s victory, the red sweep, and two rate cuts in November and December, closing the quarter with a 2.7% gain.

On the factor front, the Q3 rotation faded quickly:

- Growth posted the strongest returns in most regions (U.S., developed world and emerging markets).

- Europe stood out, with momentum and value dominating over the quarter.

- Quality continued to suffer across all developed markets, extending the Q3 trend.

- In the U.S., value and high-dividend stocks experienced significant underperformance, impacting world equities due to the U.S.'s substantial weight.

- Size also underperformed in developed markets but to a lesser degree.

- In emerging markets, high dividend performed well, solidifying its position as a medium- to long-term leader. Momentum and minimum volatility also showed notable performances.

Source: WisdomTree, Bloomberg, 9/30/24–12/31/24. Calculated in U.S. dollars for all regions except Europe, where calculations are in euros. Past performance is not indicative of future results.

2024 in Review: Another Growth Year

Despite a weaker Q4, 2024 was strong for equities. Central banks initiated easing cycles, inflation receded and corporate earnings remained robust, defying early-year predictions of slowdowns or recessions. The U.S. achieved the strongest gains at 24.6%, while Europe (8.6%) and emerging markets (7.5%) lagged.

Factor-wise, while the year was less uniform than 2023, growth dominated, especially in the U.S.:

- Growth posted the strongest return in the U.S. and top-three finishes in developed and emerging markets.

- Momentum was a standout in world, European and emerging markets, driven by an exceptional first half of 2024.

- In the U.S., value underperformed the most, followed by high dividends.

- In Europe, quality had the worst returns, with size and growth just behind.

- Notably, quality experienced one of its worst performances in years, underperforming across all regions.

- In emerging markets, high dividend continued to perform well, finishing second for the year with a 3.5% outperformance.

Source: WisdomTree, Bloomberg, 12/31/23–12/31/24. Calculated in US. Past performance is not indicative of future results.

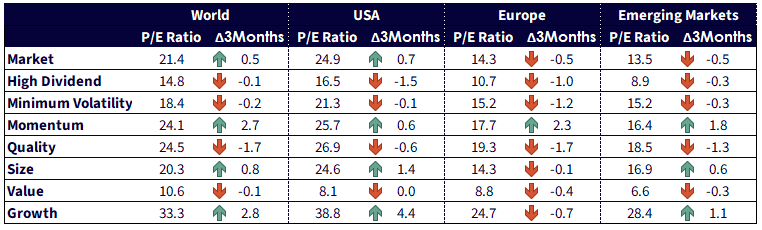

Growth in the U.S. Is Getting Pretty Expensive

In Q4 2024, U.S. market valuations increased, with the price-to-earnings (P/E) ratio rising by 0.7. Growth stocks became even more expensive, with the P/E ratio climbing by 4.4 to 38.8. Years of dominance have led to high valuations for major growth names. In European and emerging markets, valuations declined, with overall valuations appearing inexpensive by historical standards. Value and high dividend stocks are priced at P/E ratios of 10 or lower.

Figure 3: Historical Evolution of Price-to-Earnings Ratios of Equity Factors

Source: WisdomTree, Bloomberg, as of 12/31/24. Past performance is not indicative of future results. World is proxied by MSCI World net TR Index. U.S. is proxied by MSCI USA net TR Index. Europe is proxied by MSCI Europe net TR Index. Emerging Markets is proxied by MSCI Emerging Markets net TR Index. Minimum volatility is proxied by the relevant MSCI Min Volatility net total return index. Quality is proxied by the relevant MSCI Quality net total return index. Momentum is proxied by the relevant MSCI Momentum net total return index. High Dividend is proxied by the relevant MSCI High Dividend net total return index. Size is proxied by the relevant MSCI Small Cap net total return index. Value is proxied by the relevant MSCI Enhanced Value net total return index. WisdomTree Quality is proxied by the relevant WisdomTree Quality Dividend Growth Index.

Looking Forward to 2025

In 2024, growth had a second year of dominance. However, market behaviors differed, with momentum posting the second-best results, unlike quality’s second-place finish in 2023. As we look to 2025, while maintaining a constructive view on equities, concerns about growth stock valuations persist. Investors may benefit from diversifying factor exposure across growth, value and quality, anticipating multiple micro factor rotations.

Pierre Debru is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.’s parent company, WisdomTree, Inc.

Categories

About the contributor

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.