Looking Back at Equity Factors in Q2 2025 with WisdomTree

Published August 5, 2025

Pierre Debru

Head of Research, WisdomTree Europe.

Key Takeaways

- A pause in U.S. tariff threats and a weakening dollar fueled an 11.5% Q2 surge in global equities, with growth and momentum leading thanks to AI-driven earnings strength among mega-caps.

- Despite global headwinds, value outperformed year-to-date, especially in Europe and emerging markets, as cyclical stocks rode policy easing and currency tailwinds, while quality lagged across the board.

- Size made a strong comeback in Europe and EM, supported by rate cuts and domestic demand sensitivity, positioning small caps as key beneficiaries of easing cycles and valuation discounts.

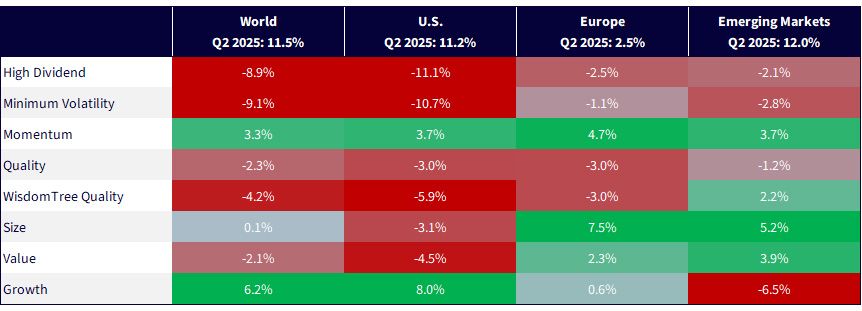

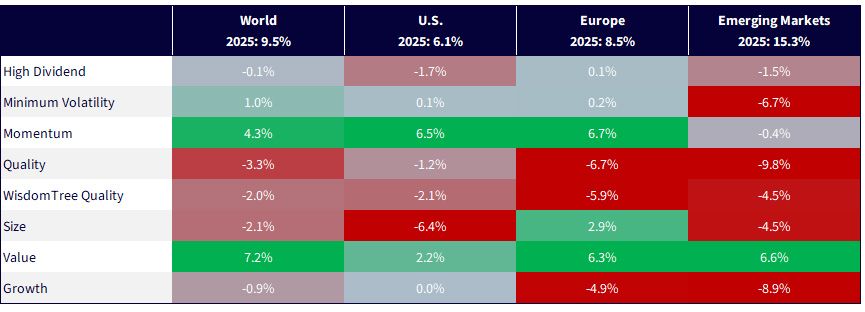

Global equities powered through the second quarter of 2025, as a 90-day pause on fresh U.S. "reciprocal tariffs" reignited risk appetite and helped the MSCI World Index return 11.5%. The MSCI USA returned an almost identical 11.2%, while emerging markets (EM) benefited strongly as well, at 12.0%. Europe, on the other hand, faltered after a strong start, with 2.5%. Q1's rally left the year-to-date (YTD) scorecard at 9.5% for world equities, 6.1% for the U.S., 8.5% for Europe and 15.3% for EM.

The policy pause was reinforced by softer core inflation prints and a 10% slide in the dollar index, its steepest consecutive quarter drop in three decades. Meanwhile, the European Central Bank (ECB) delivered cuts of 25-basis points (bps) in April and June, taking the deposit rate to 2%, while the Federal Reserve stayed on hold despite intensifying political calls for a 300-bp easing cycle.

From a factor perspective,

- Growth and momentum led Q2 on AI-related capex strength across global and U.S. equities. All other factors struggled in those regions.

- Value is 2025's global winner (+7.2% vs. MSCI World) as cyclicals catch the dollar tailwind, whereas quality is the laggard (−3.3% vs. MSCI World).

- Regional divergences: Europe's unremarkable performance in Q2 hid a strong size pulse; EM saw value and size surge on policy easing.

This instalment of the WisdomTree Quarterly Equity Factor Review examines how equity factors behaved during the second quarter and their potential impact on investors' portfolios.

Quarterly Performance in Focus: Tariffs, Tech and a Size Revival

The tariff pauses and weaker dollar propelled equities higher, with mega-cap tech re-accelerating in the U.S. and a rates-sensitive rebound in EM. Europe trailed as profit revisions lagged, and energy names underperformed despite the ECB easing.

On the factor front, Q2 showed a strong rotation from value to growth:

- Growth andmomentum thrive on AI earnings: Blockbuster Q2 results from the Magnificent 7 lifted growth in the U.S. and globally; momentum was the most consistent and added 3%–5% across regions.

- Risk-off factors retreat: The volatility fade and flatter yield curves hurt high dividend and min-vol.

- Size comeback in Europe and EM: Lower real yields and tariff optimism boosted European industrials and EM exporters, propelling size.

- Value pockets of strength: Value beat in EM and Europe on better cyclicals, even though it lagged in the U.S. amid tech dominance.

Figure 1: Equity Factor Outperformance in Q4 2024 across Regions

Source: WisdomTree, Bloomberg, for the period 3/31/24–6/30/25. Calculated in U.S. dollars for all regions except Europe, where calculations are in euros. Past performance is not indicative of future results.

H1 in Review: Value Ascendant, Quality in Retreat

Despite tariff scares, global equities have added 9.5% YTD, helped by disinflation and early-cycle rate cuts outside the U.S. The ECB's cumulative 200-bp easing contrasts with a Fed on pause, widening rate differentials and supporting non-U.S.-dollar assets, leading to a strong 8.5% from the MSCI Europe and 15.3% from MSCI Emerging Markets YTD.

On the factor front, value dominated in H1

- Global value leadership: Cheaper cyclicals and financials rallied on higher nominal growth and a weaker dollar, lifting value 6%–7 % above benchmarks worldwide.

- Momentum still potent in the U.S. and Europe: Sustained earnings revisions kept momentum atop regional tables even as growth cooled in Q1.

- Quality under strain: Rising duration risk premiums and fading mega-cap safe-haven demand left quality weakest everywhere aside from a more risk-averse period around February and March.

- Small caps still split: Size enjoyed a revival in Europe and EM but remains under water in the U.S. (-6.4 %), where policy uncertainty lingers.

Figure 2: Equity factor Outperformance Year to Date across Regions

Source: WisdomTree, Bloomberg, for the period 12/31/24–6/30/25. Calculated in U.S. dollars. Past performance is not indicative of future results.

Size Strikes Back: Are Rate Cuts Lighting a Small-Cap Revival?

After years in the wilderness, small caps and mid-caps are finally outperforming large caps in Europe and emerging markets, helped by the ECB's back-to-back 25-bp cuts in April and June and a softer U.S.-dollar backdrop. The MSCI Europe Small Cap is up 11.7 % YTD versus 8.7% for the MSCI Europe and only 0.4% for the Russell 2000. Overall cheaper valuations and rising earnings beta to domestic demand are driving this potential size revival.

In EM, policy easing and a semiconductor rebound in Korea/Taiwan have lifted the MSCI EM Small Cap to 19% versus 13.8% for MSCI EM since the start of Q2.

Figure 3: Small Caps Have Dominated in the Last 3 to 4 Months in Europe and Emerging Markets

Source: WisdomTree, Bloomberg, for the period 12/31/23–7/15/25. Calculated in U.S. dollars for EM and euros for Europe. The graph represents the performance differential (calculated as a ratio of the normalized performance of the two indexes) between MSCI Europe Small Cap net and MSCI Europe net for one line and MSCI EM Small cap net and MSCI EM net for the other. Past performance is not indicative of future results.

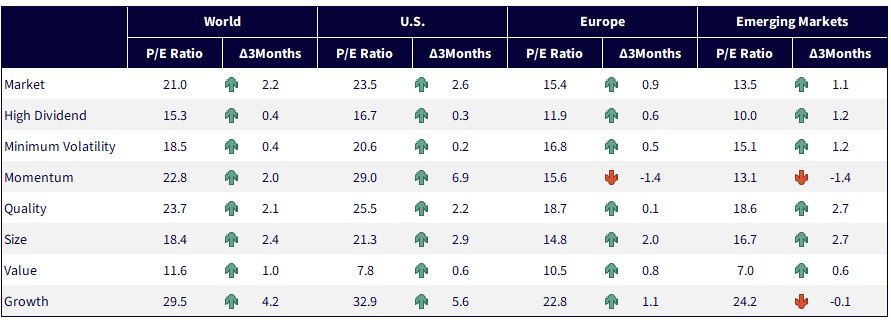

Growth Remains Very Expensive across the Board

Valuation increased almost across the board in Q2 2025, with growth, size and quality experiencing mostly above-market rises, while the valuation of other factors suffered smaller increases. Momentum in Europe and EM stands out as the exception to the rule with clear drops in valuation this quarter.

Figure 4: Historical Evolution of Price-to-Earnings ratios of Equity Factors

Source: WisdomTree, Bloomberg, as of 6/30/25. Past performance is not indicative of future results. World is proxied by MSCI World net TR Index. U.S. is proxied by MSCI USA net total return index. Europe is proxied by MSCI Europe net TR Index. Emerging markets is proxied by MSCI Emerging Markets net total return index. Minimum volatility is proxied by the relevant MSCI Min Volatility net total return index. Quality is proxied by the relevant MSCI Quality net total return index. Momentum is proxied by the relevant MSCI Momentum net total return index. High dividend is proxied by the relevant MSCI High Dividend net total return index. Size is proxied by the relevant MSCI Small Cap net total return index. Value is proxied by the relevant MSCI Enhanced Value net total return index. WisdomTree Quality is proxied by the relevant WisdomTree Quality Dividend Growth Index.

Positioning for a Divergent Second Half

With U.S. policy still data-dependent, the ECB mid-cycle in easing mode and several EM central banks already cutting, investors face an increasingly asynchronous macro map. A soft-landing scenario—gradual disinflation, modest growth and no new tariff escalation could:

- Sustain growth and momentum leadership in the U.S. if AI capex and earnings beats persist.

- Extend the value-size catch-up in Europe and EM as cheaper cyclicals benefit from easier policy and a weaker dollar.

Conversely, a tariff relapse or sticky U.S. inflation would argue for selective quality, high dividend and min-vol hedges.

Facing such a market, investors could look at a barbell between quality growth (for secular compounders) with smaller-cap value (for cyclical beta). Also, an overweight European value and EM momentum where monetary loosening is most advanced could be helpful as well.

Pierre Debru is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management Inc.'s parent company, WisdomTree, Inc.

Categories

About the contributor

Pierre Debru

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.