Introducing WisdomTrees True EM Strategy

Published July 11, 2025

Global Head of Research

Key Takeaways

- In July 2025, WisdomTree adjusted the True Emerging Markets Index, which reclassifies South Korea and Taiwan as developed markets and excludes China to better reflect macroeconomic fundamentals rather than operational constraints.

- This bold realignment shifts EM exposure away from stagnant, overrepresented giants toward faster-growing, underrepresented economies like India, Brazil and Saudi Arabia.

- By emphasizing such data points as GDP per capita, the Human Development Index and economic resilience, the Index offers investors a forward-looking, high-growth alternative to legacy EM benchmarks.

In the world of asset management, few things shape investor behavior more than index classifications. Whether a country is labeled “developed,” “emerging” or “frontier” may seem academic, but these labels direct the flows of trillions of dollars. For practical purposes, three firms—MSCI, FTSE Russell (FTSE) and S&P Dow Jones Indices (S&P)—have become the de facto arbiters of these classifications.

Yet these providers don’t agree on everything. They each maintain their own methodology, tailored to their client base and benchmarking practices:

- MSCI centers its framework on three pillars: economic development (using gross national income per capita), market size and liquidity, and market accessibility—with detailed assessments of foreign ownership limits, currency convertibility and information flow.1

- FTSE emphasizes a “Quality of Markets” checklist, requiring markets to meet all 21 criteria (ranging from custody arrangements to short-selling rules) for developed status, in addition to thresholds for income, credit rating and market breadth.2

- S&P, meanwhile, takes a hybrid approach: combining quantitative tests (market capitalization, liquidity, foreign exchange freedom3) with qualitative review and client consultation. It is the only provider to require both multiple market structure criteria and full satisfaction of liquidity, accessibility and macroeconomic thresholds before upgrading a market to developed.4

There’s a fundamental tension at the heart of how we classify markets, in the lived reality of a country versus the operational needs of capital flows. Travelers, entrepreneurs and policy makers experience development through infrastructure, institutional competence and social resilience. Investors managing trillions, by contrast, require FX convertibility, settlement protocols and liquidity screens. Index providers lean hard toward the latter—not because it’s wrong, but because it’s replicable. This is why WisdomTree sees this a timely opportunity to bring focus to the WisdomTree True Emerging Markets Index.

The Case of China

For many investors, the conversation about China has shifted from market fundamentals to politics. While China is the world’s second-largest economy5 and a leader in advanced manufacturing and technology, its classification as an emerging market increasingly clashes with unease about its governance model, capital controls and strategic rivalry with the U.S. Exposure to China is no longer just a financial allocation—it’s a geopolitical position. The rise of “ex-China” investment strategies reflects growing concern that alignment with Chinese policy raises the risk of forced divestment, blacklisting or broader value-system conflicts.

The Ambiguity of South Korea and Taiwan

Nor is it accidental that South Korea and Taiwan—leaders in semiconductors and digital infrastructure—still straddle ambiguous territory depending on the provider.

Bottom line: We at WisdomTree see it as an opportunity to classify South Korea and Taiwan as Developed within theWisdomTree True Emerging Markets Index framework.

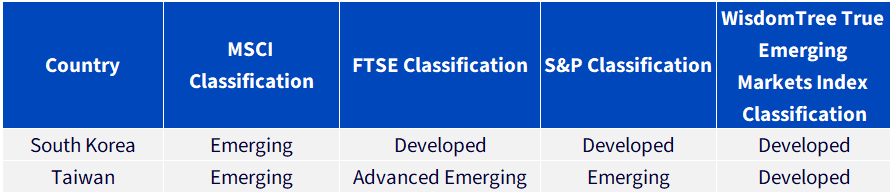

Figure 1: Classifications of South Korea & Taiwan

Sources: MSCI, FTSE and S&P, verified as of 6/27/25. WisdomTree’s classification framework refers only to the methodology of the WisdomTree True Emerging Markets Index, not any other WisdomTree Index. You cannot invest directly in an index. Subject to change.

South Korea

Despite strong macroeconomic fundamentals, South Korea remains classified as an Emerging Market by MSCI due to persistent market access barriers—particularly currency convertibility restrictions, complex foreign investor onboarding and regulatory misalignment with developed standards.6 In contrast, FTSE and S&P both designate South Korea as a Developed Market, citing its advanced infrastructure, operational efficiency, high per capita income and substantial market liquidity.7 The divergence underscores a split between macroeconomic maturity and operational frictions: while the International Monetary Fund (IMF) labels South Korea an Advanced Economy8 based on industrial complexity, export competitiveness and institutional strength, MSCI continues to focus on investor accessibility constraints.

Taiwan

Taiwan remains classified as an Emerging Market by MSCI9 and S&P,10 mainly due to capital repatriation limits, regulatory idiosyncrasies and friction in foreign investor processes. FTSE takes a middle ground, labeling Taiwan an Advanced Emerging Market—a bridge category for economies with developed-like liquidity and infrastructure but lingering policy restrictions.11 Economically, however, Taiwan fits squarely within the IMF’s definition of an Advanced Economy,12 given its leadership in semiconductors, trade surpluses, financial stability and integration into global supply chains. The disconnect between index provider classifications and macroeconomic reality reflects differing thresholds for investor operability versus economic capability to shape global dynamics.

Introducing the WisdomTree True Emerging Markets Index Country Classification Framework

Ask most investors whether a country is developed or emerging, and they won’t start by quoting FX convertibility rules or settlement protocols. They’ll picture it. Can I walk through its cities and feel institutional competence? Do the airports hum with throughput and logistics? Do the people enjoy long lives, good education and purchasing power? Is the economy diversified and resilient, or narrowly tied to a single export? The current frameworks used by MSCI, FTSE and S&P are primarily designed for index replication, not for capturing that intuitive, full-spectrum view of modernity and systemic maturity.

The WisdomTree True Emerging Markets Index’s classification framework—built on such macroeconomic markers as gross domestic product (GDP) per capita, Human Development Index (HDI)13 scores, market depth, creditworthiness and economic resilience—goes straight to the core of how allocators, entrepreneurs and policy makers actually experience a country’s level of development.

The strategy opens the door to spotting transitional stories—like India, Vietnam or Chile—that are developing in substance but still misclassified by legacy rules. And it flags markets—like Saudi Arabia or even parts of Eastern Europe—that may appear investable by liquidity standards but fail to meet the deeper test of broad-based development. Most importantly, it puts investors back in the driver’s seat: using transparent metrics, not inherited heuristics, to define the future of global exposure.

India’s Rise from Opportunity to Anchor

India stands at the crossroads of structural reform and demographic dividend, and the runway for equity growth has rarely looked more powerful. With a multi-decade track record in Indian equities, WisdomTree places India as a strategic pillar in its True Emerging Markets Index, not a tactical allocation. The investment thesis spans multiple layers: deepening domestic capital markets, resilient GDP growth, a rising middle class and sustained digital and infrastructure transformation.14 As South Korea and Taiwan are removed from the WisdomTree True Emerging Markets Index’s exposure, India becomes the gravitational center of the approach. The country’s robust macro indicators—rising consumption, accelerating credit and monetary easing—now converge with institutional continuity and high retail participation, creating a unique combination of scale, liquidity and reform momentum.

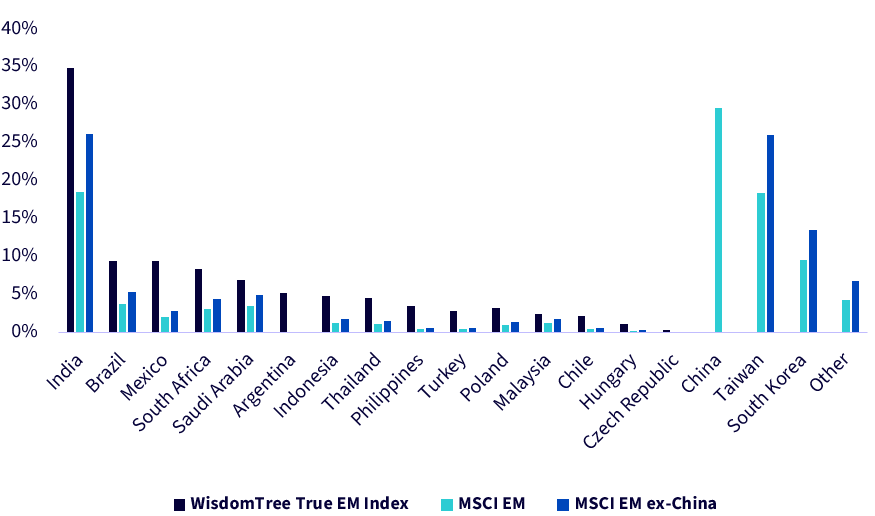

In figure 2, we see:

- WisdomTree’s True Emerging Markets Index reallocates exposure away from East Asia and toward higher-growth, underrepresented economies—most notably India, Brazil and Saudi Arabia—capturing a broader and more forward-looking EM opportunity set.

- While traditional EM benchmarks like MSCI EM remain heavily concentrated in China, Taiwan and South Korea, the WisdomTree True Emerging Markets Index approach reallocates toward countries with rising domestic demand, improving market access and greater diversification potential across regions and sectors.

Figure 2: An EM Allocation for the Next Decade

Sources: WisdomTree, FactSet, with data as of 6/30/25. EM stands for emerging markets. Sector weights are subject to change. You cannot invest directly in an index.

Gauging the Fundamentals

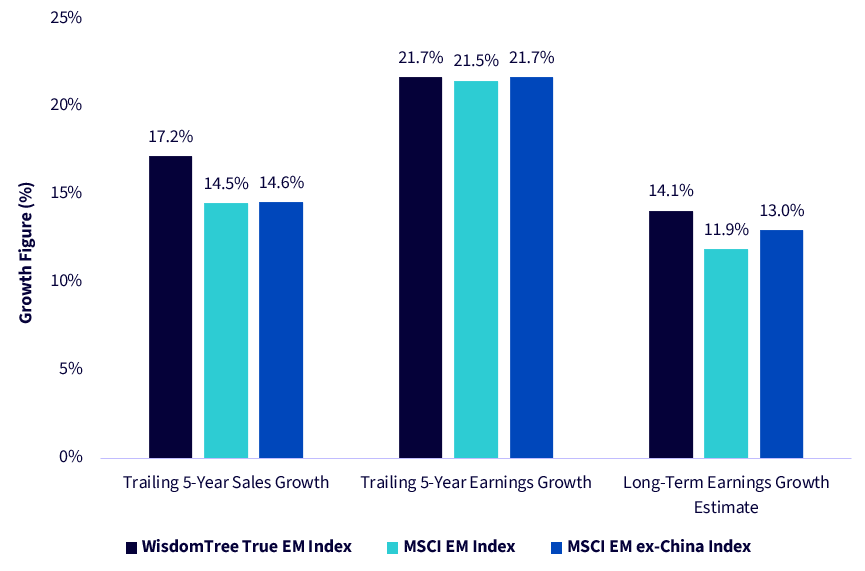

In figure 3, it is clear that:

- WisdomTree’s True Emerging Markets Index delivers superior growth exposure—outperforming on both trailing sales and forward earnings—by intentionally excluding dominant markets like China, Taiwan and Korea in favor of faster-growing, often underrepresented economies.

- While earnings growth has been broadly similar across all EM benchmarks, WisdomTree’s tilt toward more dynamic, reform-oriented economies reveals a meaningful growth premium in both revenue momentum and projected earnings expansion.

Figure 3: WisdomTree’s True Emerging Markets Index: Unlocking Structural Growth Advantages

Sources: WisdomTree, FactSet, with data as of 6/30/25. EM stands for emerging markets. You cannot invest directly in an index.

WisdomTree True Emerging Markets Index: A Framework Built for Where Growth Is Going

At its core, the WisdomTree True Emerging Markets strategy is about realigning EM exposure with how investors intuitively understand progress, potential and risk. By classifying South Korea and Taiwan as developed—and excluding China—WisdomTree clears space for what matters most: meaningful exposure to dynamic, underrepresented economies like India.

1Source: MSCI Market Classification Framework, MSCI Inc., June 2023.

2Source: FTSE Russell, FTSE Equity Country Classification Process – March 2024 Interim Update, FTSE International Limited, March 2024.

3Refers to the freedom and ease with which foreign investors can access and transact in the country’s local currency—particularly for purposes of buying, selling and repatriating investments.

4Source: S&P Dow Jones Indices, Country Classification Methodology, S&P Global, August 2024.

5Source: World Economic Outlook: Navigating Divergent Global Growth Paths, International Monetary Fund, April 2025.

6Source: MSCI Announces Results of the MSCI 2025 Market Classification Review, MSCI Inc., 6/24/25.

7Sources: FTSE Russell, FTSE Equity Country Classification – March 2025 Interim Announcement, FTSE International Limited, 4/8/25; S&P Dow Jones Indices, Market Classification, S&P Global. https://www.spglobal.com/spdji/en/landing/topic/market-classification/

8Source: World Economic Outlook: Navigating Divergent Global Growth Paths, International Monetary Fund, April 2025.

9Source: MSCI Announces Results of the MSCI 2025 Market Classification Review, MSCI Inc., 6/24/25.

10Source: S&P Dow Jones Indices, Market Classification, S&P Global. https://www.spglobal.com/spdji/en/landing/topic/market-classification/

11Source: FTSE Russell, FTSE Equity Country Classification – March 2025 Interim Announcement, FTSE International Limited, 4/8/25.

12Source: World Economic Outlook: Navigating Divergent Global Growth Paths, International Monetary Fund, April 2025.

13The Human Development Index was developed by the United Nations Development Programme (UNDP) to measure and compare levels of human development across countries.

14Source: India Equity Strategy: Catalysts Ahead—3Q25, Market to Rise Rather Than Fall, Morgan Stanley Research, 6/26/25.

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.