HEDJ

Europe Hedged Equity Fund

Published November 6, 2024

Associate, Investment Strategy

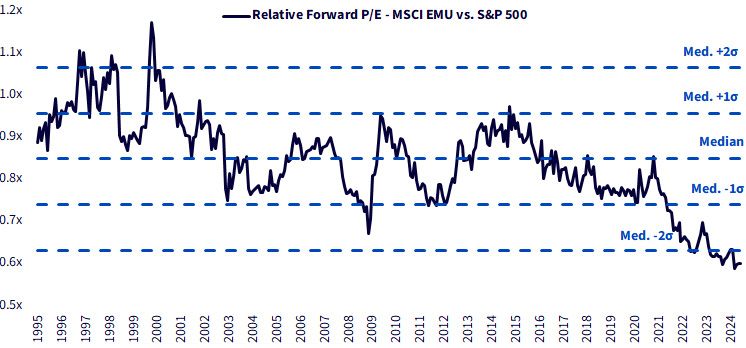

For virtually the entire post-pandemic environment, European equities have been historically cheap relative to U.S. stocks.

This is not surprising. In the nearly four years since the end of 2020, U.S. markets have been propelled by the eminent Magnificent 7 and other beneficiaries of artificial intelligence, resulting in 13.8% annualized gains for the S&P 500. Valuations followed suit, climbing to their highest levels since the throes of the pandemic and inspiring debate about what constitutes a “fair” multiple for the index amid rapidly changing sector and fundamental composition.

Meanwhile, Europe was mired in a low-growth environment with an absence of innovative technology companies to pique the interests of global investors fixated on the U.S.

Today, the U.S.-Europe equity disparity has culminated in the cheapest relative valuations we’ve ever seen. Forward price-to-earnings (P/E) multiples for the MSCI EMU Index (European Economic and Monetary Union) compared to the S&P 500 are more than two standard deviations below their long-term median, where they have remained for over a year.

Sources: WisdomTree, MSCI, S&P, as of 9/30/24. You cannot invest directly in an index.

The valuation differential is finally intriguing Europe-skeptics at a time when post-pandemic U.S. equity superiority and subsequent market concentration is prompting diversification discussions. Discouraged by lofty U.S. multiples and underwhelming forward return expectations, equity allocators are beginning to consider European positions for the first time in recent memory.

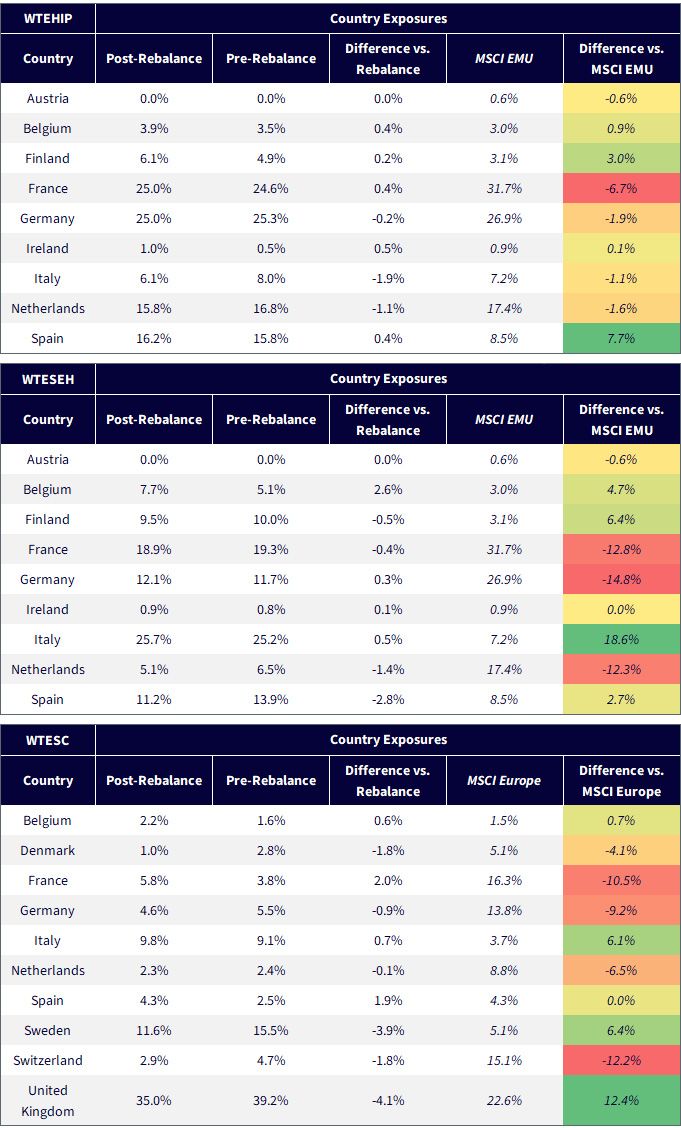

For those newly considering international allocations, we recently rebalanced our suite of European equity Indexes in October.

These Indexes are intended to be broadly diversified and highly correlated to representative market cap-weighted Index variants.

Below we summarize some of the notable changes from the 2024 rebalance.

Sources: WisdomTree, MSCI. MSCI Europe and MSCI EMU country exposures as of 9/30/24. WisdomTree Index country exposures as

of 10/22/24 to represent post-rebalance data. You cannot invest directly in an index.

In WTEHIP, there were no major changes between the pre- and post-rebalance country allocations. The Index retains a heavily over-weight allocation to Spain and to Finland to a lesser extent, and under-weight allocations to France, relative to the MSCI EMU. Under-weight allocations to France and Germany were a result of our Index’s 25% country exposure caps.

For WTESEH, the pre- and post-rebalance changes were also negligible. It has heavily under-weight allocations to France, Germany and the Netherlands relative to the MSCI EMU, which are partially offset by allocations to Italy, Belgium and Finland.

WTESC, which includes the U.K., has more pronounced changes resulting from its rebalance. Relative to the MSCI Europe Index, it has a more than 12% over-weight allocation to the U.K. and an under-weight allocation to Switzerland of the same size. It also has large under-weight allocations to France and Germany, which are partially offset by over-weight allocations to Sweden and Italy.

The opportunity for Europe may be compounded as the attractive valuations discussed earlier coincide with additional macroeconomic stimuli.

The European Central Bank (ECB) is still in the early stages of monetary easing in an effort to stimulate economic growth. It has cut rates three times so far this year and more reductions are expected over the near term. Lower policy rates may weigh on the euro, which would make European-manufactured goods more competitive in the global marketplace.

This could benefit exporters, which is especially valuable as the current growth prognosis for the eurozone remains relatively weak.

With greater dependency on non-eurozone economies, exporters may receive a tailwind from Chinese stimulus and steady growth in the U.S.

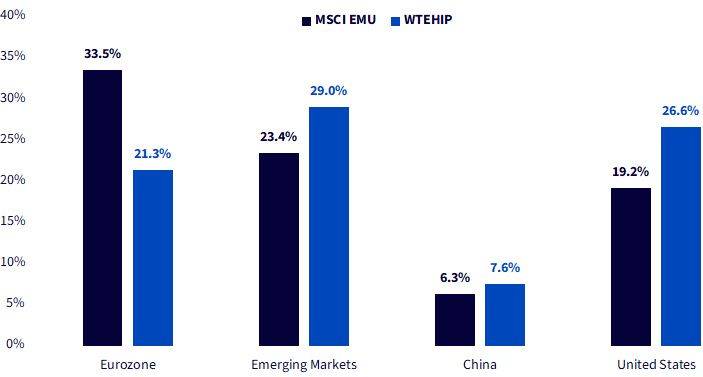

Compared to the broader eurozone index, WTEHIP features greater international linkages. According to FactSet Geographic Revenue (GeoRev) data, the companies represented in WTEHIP receive about 26% of revenue from the U.S., where the economy remains rock solid. That’s about 7% more than the MSCI EMU, in aggregate.

In the emerging markets, the region’s revenue exposure is about 23%, compared to 29% for our Index. WTEHIP also sports a 1% revenue pickup in China. While small in amount, it could be beneficial as China continues to flirt with more economic stimulus. If Chinese stimulus measures disappoint, or if the economy continues to falter, its impact on WTEHIP would likely be modest.

Sources: WisdomTree, FactSet, as of 9/30/24. You cannot invest directly in an index.

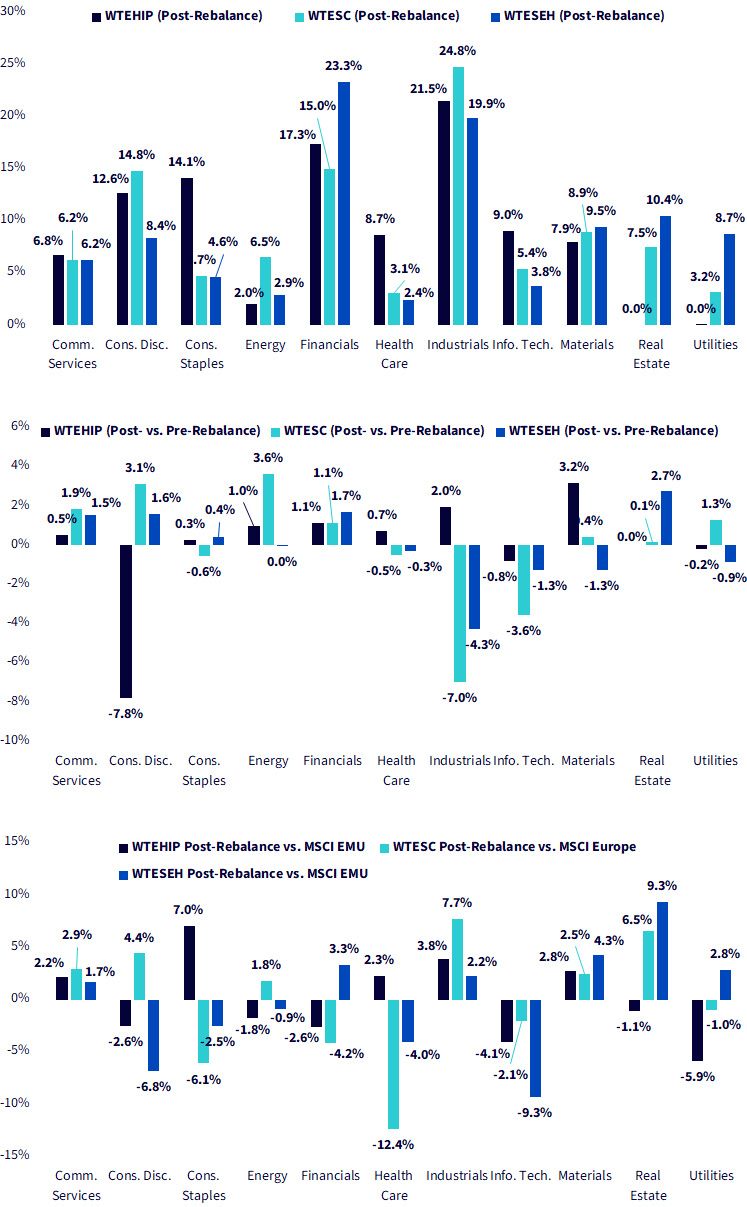

Sources: WisdomTree, MSCI. MSCI Europe and MSCI EMU sector exposures as of 9/30/24. WisdomTree Index sector exposures as of 10/22/24 to

represent post-rebalance data. You cannot invest directly in an index.

At the sector level, the only major changes stemming from the rebalance were to Consumer Discretionary within WTEHIP and to Industrials within the two small-cap Indexes, which are now all underweight their pre-rebalance exposures by about 4%–8%.

Relative to the MSCI EMU, WTEHIP and WTESEH both have considerable under-weight allocations to Information Technology and Consumer Discretionary, which are partially offset by over-weight allocations to Communication Services, Industrials and Materials. Compared to broader Europe, WTESC features larger under-weight exposures to Consumer Staples, Financials and Health Care, and over-weight exposures to Consumer Discretionary, Industrials and Real Estate.

Our annual rebalance tends to make our Indexes even more appealing from a fundamental standpoint, and especially when compared to the market cap-weighted MSCI Europe. This year’s screening process was no exception. As a result:

For additional details on each rebalance, please visit the respective Index pages on the WisdomTree website:

There are risks associated with investing, including the possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

HEDJ: Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time.

DFE: Funds focusing their investments on certain sectors and/or smaller companies increase their vulnerability to any single economic or regulatory development. This may result in greater share price volatility.

EUSC: This Fund focuses its investments in Europe, thereby the impact of events and developments associated with the region can adversely affect performance. The securities of small-capitalization companies generally trade in lower volumes and are subject to greater and more unpredictable price changes than larger capitalization stocks or the stock market as a whole. The Fund uses various strategies to attempt to minimize the impact of changes in the value of the euro against the U.S. dollar and these strategies may not be successful. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs.

Associate, Investment Strategy

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.