NTSD

Efficient U.S. Plus International Equity Fund

Published March 19, 2026

Global Chief Investment Officer

In 2018, we launched our first 90/60 capital efficient ETF with a simple but powerful idea: investors struggle with creating optimal portfolios that include diversifying alternatives. Creating a better core of stocks with bonds can free up space to add in diversifiers.

By pairing a 90% allocation to U.S. equities with a 60% Treasury futures overlay, we created a structure designed to deliver 150% notional exposure of a traditional 60/40 stock/bond allocation. This specific allocation percentage created a clean heuristic: 2/3 exposure to 90/60 would replicate a core 60/40 with 1/3 of portfolio space available to add diversifying exposures.

Following the launch of the WisdomTree U.S. Efficient Core Fund (NTSX), Cliff Asness, co-founder of AQR Capital Management, commented on the social platform then called Twitter that although he had a “22-year head start” from a research perspective (linking to a piece he wrote in December of 1996 serving as Goldman Sachs Asset Management’s director of quantitative research), WisdomTree managed to “beat him” in launching this type of levered 60/40 idea in an exchange-traded fund.

In Asness’s 1996 piece, titled “Why Not 100% Equities: A Diversified Portfolio Provides More Expected Return per Unit of Risk,” one of his core arguments was that an “investor willing to bear the risk of 100% equities can do even better with a diversified portfolio.”

Much of academic research fails to replicate out of sample—but the Asness piece ‘actually’ worked better in the 30-years since his first publishing of the piece.

Since then, we expanded the capital efficient stock/bond overlay globally with the WisdomTree International Efficient Core Fund (NTSI) (developed markets) and the WisdomTree Emerging Markets Efficient Core Fund (NTSE) (emerging markets), and into commodities with gold overlays (WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE) and WisdomTree Efficient Gold Plus Gold Miners Strategy Fund (GDMN)).

The reason is straightforward: capital efficiency is not a tactical trade—it is a portfolio architecture decision. And in a world with many asset classes offering lower expected returns from high valuations, one strategic decision we believe investors should make is to better optimize portfolios and become more efficient in their allocations.

We are extending our initial stock/bond framework further with a 90/60 strategy combining U.S. equities and international equities through the launch of the WisdomTree Efficient U.S. Plus International Equity Fund (NTSD). The goal: solve one of the most persistent challenges in asset allocation—home country bias—without forcing investors to reduce U.S. exposure.

NTSD applies this concept by holding a core allocation to U.S. equities while using futures to add capital-efficient international equity exposure in a 90/60 structure.

Traditional portfolio construction treats capital as the constraint. If you want to add international equities, you must sell something else—often U.S. stocks.

Capital-efficient ETFs change that equation.

Futures allow investors to gain exposure using short-term financing rates rather than fully funded capital. The cost of leverage is generally tied to the short-term financing rate embedded in futures pricing. If the expected return (equity premium) exceeds that financing cost over time, the structure can enhance portfolio efficiency.

This isn’t financial engineering for its own sake. It is using well-established institutional tools to build better and more accessible portfolios.

The International Equity Premium Is Real

Over long horizons, equity risk premia have not been confined to the U.S. They have existed globally—across developed and emerging markets. Investors have historically been compensated for bearing equity risk internationally just as they have domestically.

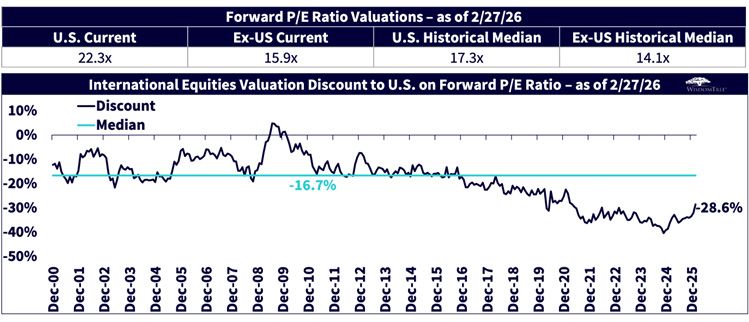

The U.S. has dominated returns in recent years, but that dominance has driven valuation gaps to historically stretched levels. The valuation gap has only begun to slightly narrow in the last 14 months.

Source: WisdomTree, MSCI, S&P. Data begins 12/29/2000 to coincide with inception of the MSCI ACWI ex-US Index. U.S. measured by S&P 500 Index. Ex-US measured by MSCI ACWI ex-US Index. You cannot invest directly in an index. Past performance is not indicative of future returns.

Valuations matter. Starting valuations are one of the strongest predictors of long-term forward returns. Today, many international markets trade at substantial discounts to U.S. equities across traditional metrics. Because the U.S. has some of the world’s leading growth stocks, over the last three decades the international markets traded at a 16% discount to the U.S. But that discount has widened out and bottomed at more than 2x the long-term average. Still today, after the last 12-month performance shift, ex-U.S. equities are still around a 30% discount to the U.S.

If the equity premium exists globally—and valuations are more attractive abroad—the expected forward return differential becomes a critical portfolio consideration.

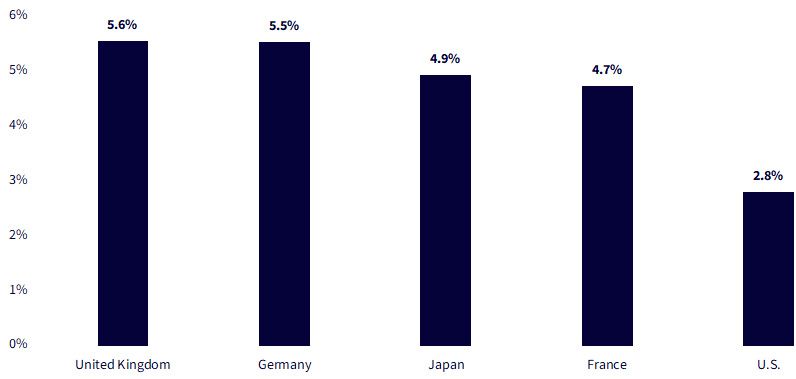

Source: WisdomTree, FactSet, MSCI, Bloomberg, as of 2/27/26. Equity Risk Premium = Forward Earnings Yield minus Inflation Indexed 10-year Government Bond Yield. Government Bond Yields measured by the respective country government bond yields. U.S. Forward Earnings Yield measured by the S&P 500 Forward Earnings Yield. All other countries measured by the respective MSCI Index Forward Earnings Yield. You cannot invest directly in an index.

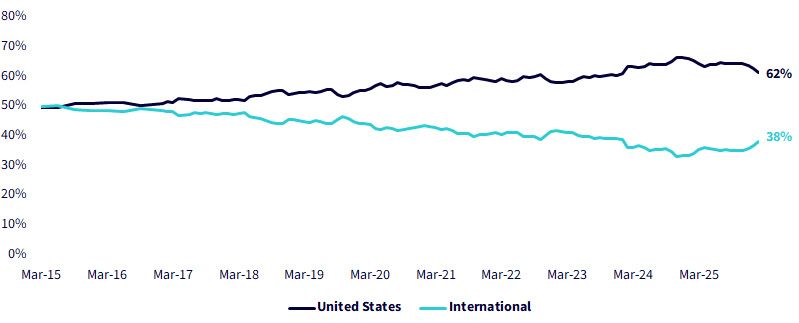

U.S. investors structurally overweight domestic equities relative to global market capitalization. When our Shared CIO portfolio team collaborates with clients, it is common to see portfolios with 80% U.S., with some even 100%.

For years, any talk of including international stocks felt like ‘de-worsification.’ Why add to positions that clients would only get a hard time for when the S&P 500 was the key consideration for most.

But if we rewind the clock just 10-years ago, the global indices were roughly 50% U.S. and 50% international. Today a neutral allocation is roughly 60% U.S. and 40% international.

Source: WisdomTree, MSCI, FactSet, 3/31/15-2/27/26. Weights measured by the MSCI ACWI Index. You cannot invest directly in an index.

There are understandable reasons—familiarity, governance standards, tax considerations—but from a portfolio construction standpoint, home country bias introduces concentration risk.

The challenge is behavioral and structural. When U.S. equities have been outperforming, few investors want to reduce their allocation.

The 90/60 structure used in NTSD addresses this tension directly. It allows investors to maintain core U.S. exposure while layering in additional international exposure through a capital-efficient overlay.

Instead of asking investors to “replace,” we allow them to “add.”

And intriguingly, a 90/60 combination of U.S. Stocks + International Stocks is similar to a 1.5x a traditional global equity mix—just like the 90/60 combination of U.S. stocks and bond was 1.5x a traditional stock/bond 60/40.

A key question: how does the math and leverage inherent to futures exposure work?

The cost of leverage in futures markets is effectively tied to short-term financing rates. Over long periods, equity risk premia have exceeded short-term rates. We think we are adding positive expected returns to a core U.S. position.

This is not a guarantee of outperformance. In periods where short-term rates spike or equity markets struggle, the structure faces headwinds.

But the outlook for short-term rates looks like we will have an accommodative Fed that will continue to reduce short-term interest rates, bringing down the cost of leverage.

If equity outperforms cash, then adding incremental international exposure via capital-efficient structures becomes a compelling strategic decision.

We believe NTSX proved that investors understood the value of combining equities and bonds in a capital-efficient wrapper. NTSI and NTSE potentially extended that logic globally.

GDE sought to demonstrate that overlays could work beyond fixed income—bringing gold exposure into equity portfolios without displacing core holdings.

The newly launched NTSD continues this evolution, seeking to bring capital efficiency to global equity exposure. It represents a broader thesis: Capital efficiency is a structural upgrade to portfolio construction.

Instead of static 60/40 allocations, investors can think in terms of:

All without increasing committed capital.

The traditional asset allocation question is: How do I divide 100% of my capital?

The capital-efficient question is: How do I maximize exposure efficiency while maintaining risk discipline?

That subtle shift opens new possibilities:

Institutional investors have known for decades, exposure management is different from capital allocation. Bringing that framework into ETF vehicles democratizes institutional portfolio tools.

Markets evolve. Products evolve. Portfolio construction must evolve with them.

The launch of NTSD represents the next step in this evolution, giving investors a capital-efficient way to expand beyond U.S. equities while maintaining their core exposure.

We believe capital-efficient ETFs represent one of the most important structural innovations in the history of ETFs and modern asset allocation. They allow investors to think in terms of exposures, premia and diversification—rather than simple capital buckets.

With international valuations where they are today, and with the long history of global equity risk premia, expanding capital-efficient strategies into global equity combinations is not just timely, it is structurally logical.

The objective is better portfolios.

And this is still just the beginning where our capital efficient family will go overtime.

NTSD: There are risks associated with investing including possible loss of principal. The Fund invests in equity securities of U.S. large-capitalization companies and in index futures contracts that provide exposure to international equity securities, and which are used to enhance the capital efficiency of the Fund. The Fund invests in a basket of equity securities of large capitalization U.S. companies generally weighted by market capitalization. The Fund expects to invest most of its assets in the securities of U.S. companies and is therefore, more likely to be impacted by events or conditions affecting the United States.

The Fund invests in derivatives to gain exposure to U.S. equity securities. The return on a derivative instrument may not correlate with the return of its underlying reference asset. The Fund’s use of derivatives will give rise to leverage. Derivatives can be volatile and may be less liquid than other securities. As a result, the value of an investment in the Fund may change quickly and without warning and you may lose money. The Fund’s investments strategy is subject to risks related to rolling. The price of futures contracts further from expiration may be higher or lower, which can impact the Fund’s return.

Investments in non-U.S. securities, including depositary receipts, involve political, regulatory, and economic risks that may not be present in investments in U.S. Securities. While the Fund is actively managed, the Fund's investment process is heavily dependent on quantitative models, and the models may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Global Chief Investment Officer

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.