Near-term headwinds, long-term support

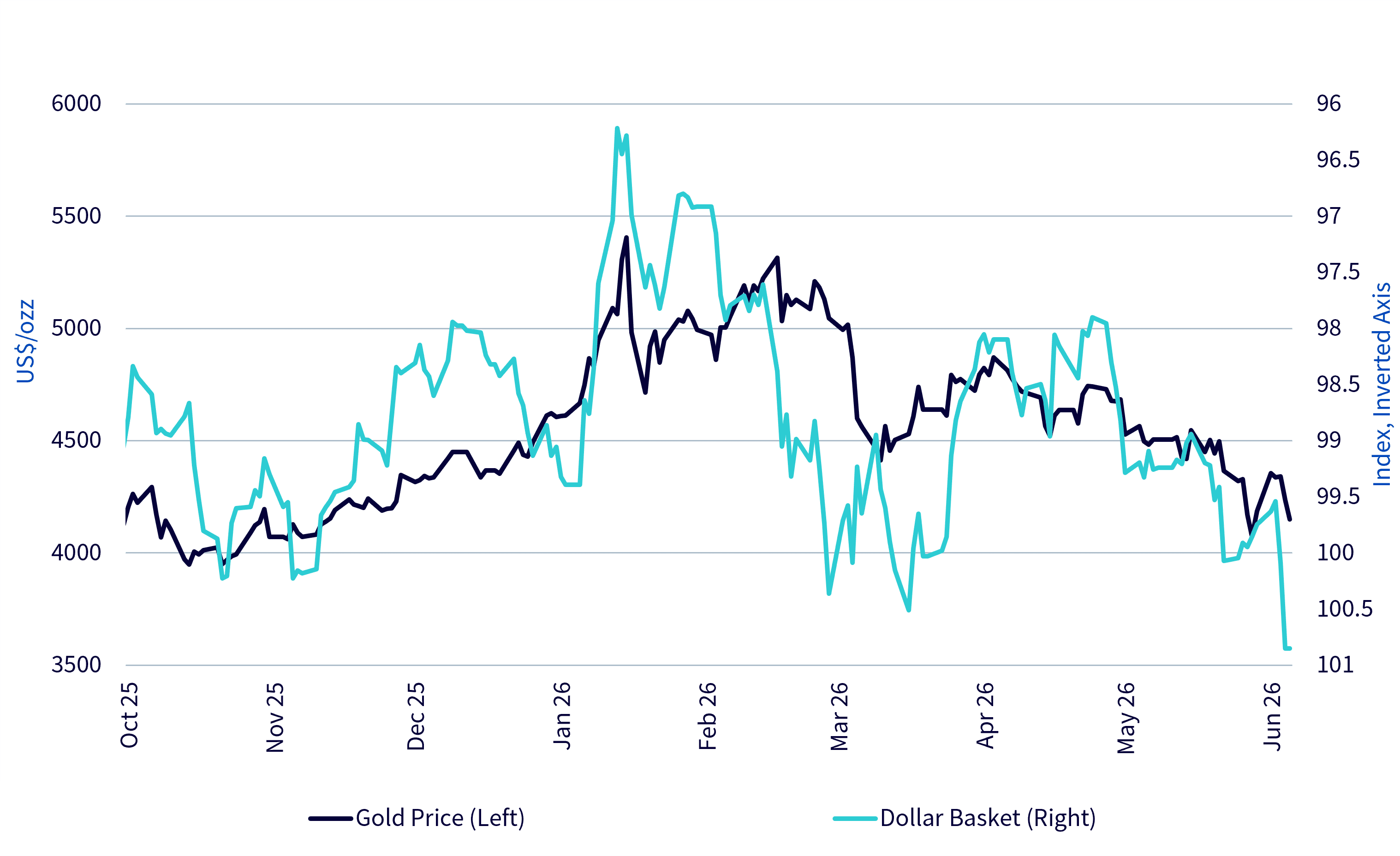

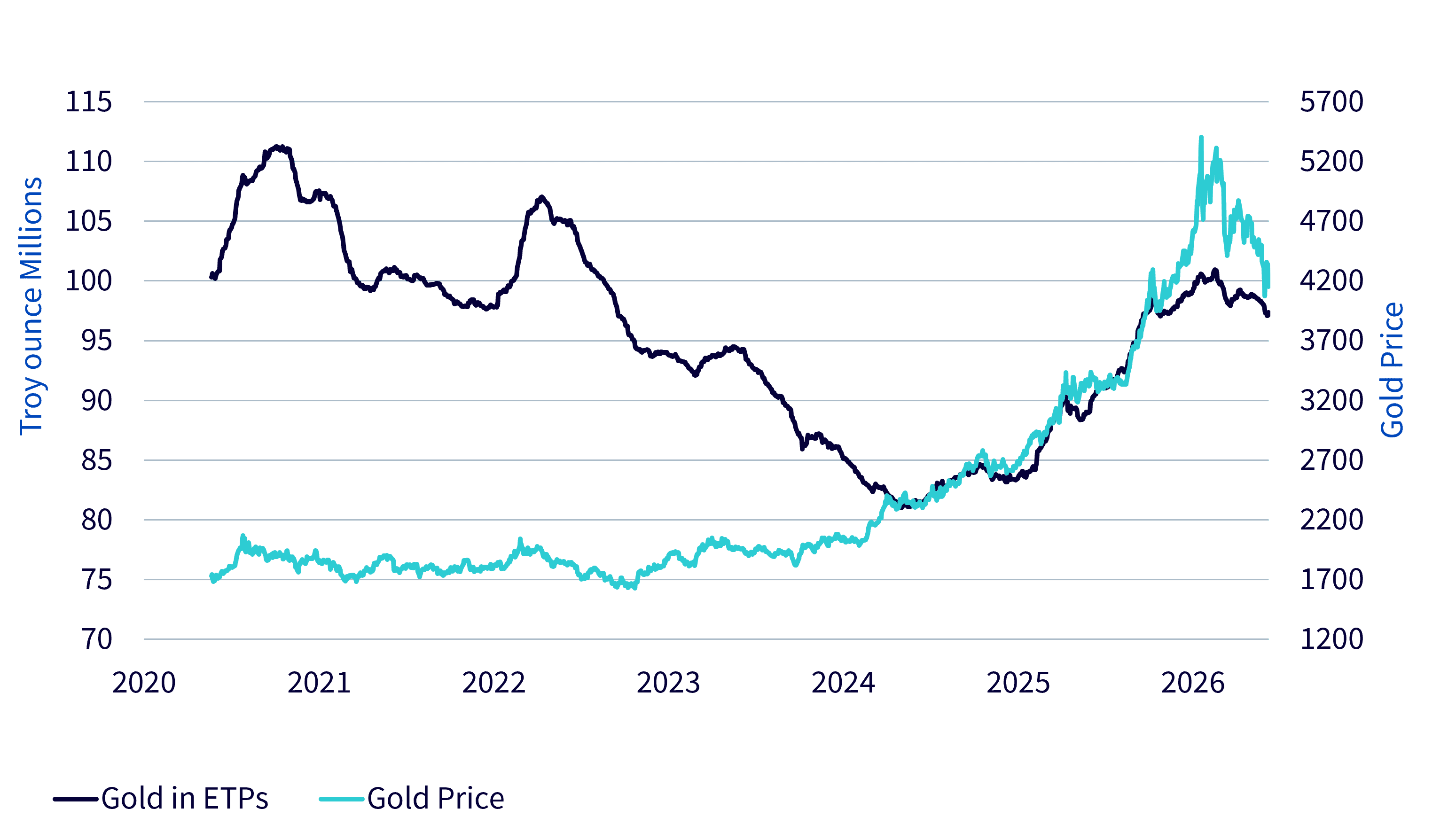

Gold prices are now below their level at the start of the year. This is a surprising outcome given that January 2026 saw the largest monthly increase in gold prices on record (measured by nominal US dollar gains rather than percentage returns). As a result, gold has experienced its most volatile first half of the year since it became a broadly investable asset.

Gold has come under pressure from rising interest rate expectations. The war in the Middle East has contributed to this shift in sentiment, as the inflationary effects of disruptions to shipping through the Strait of Hormuz led markets to anticipate a monetary policy response aimed at containing price pressures. For a brief period, gold rallied when the United States and Iran signed a Memorandum of Understanding (MoU), as investors hoped that lower energy prices would ease pressure on central banks. However, the rally proved short-lived after the Federal Reserve's June Federal Open Market Committee (FOMC) meeting signalled a more hawkish policy stance.

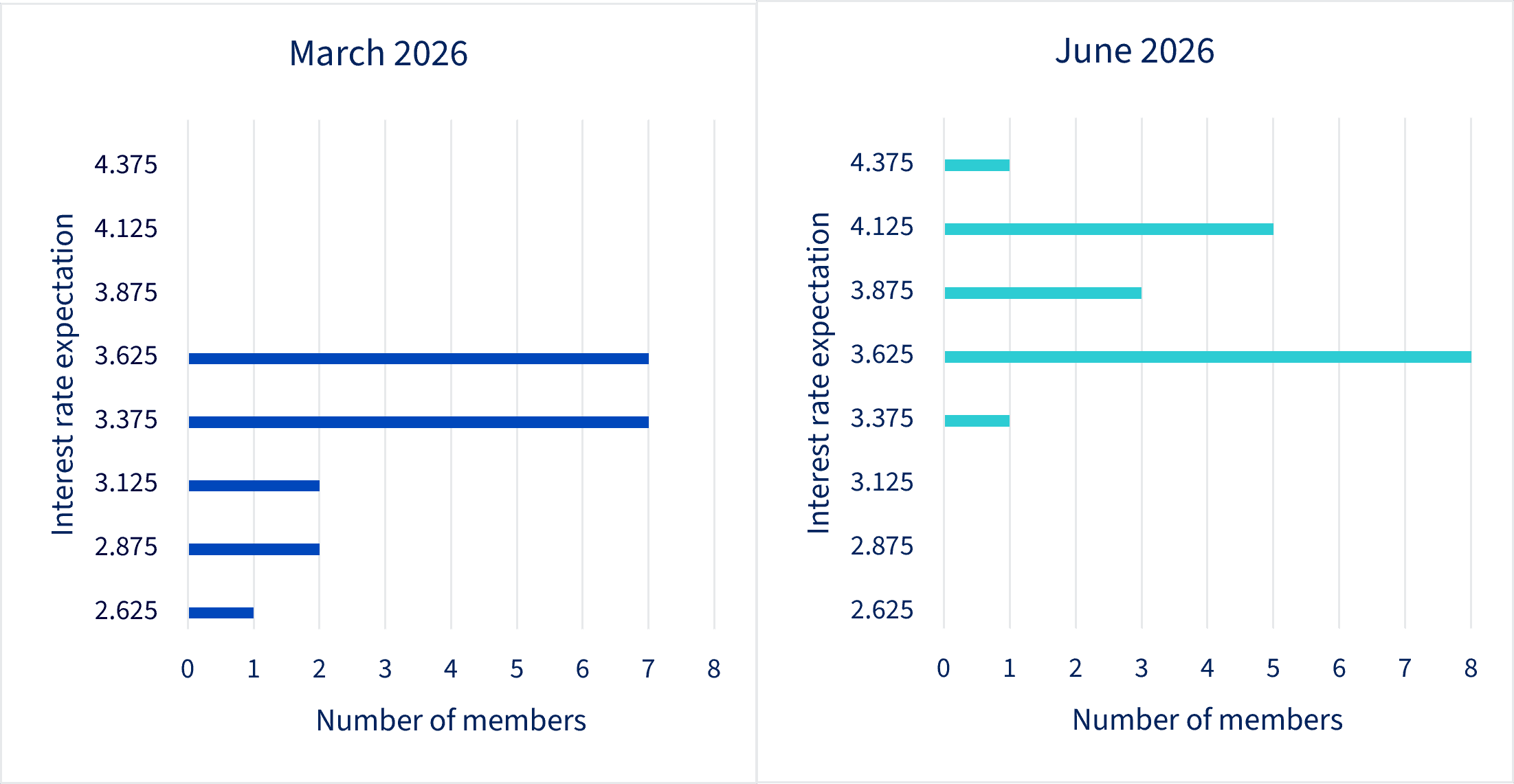

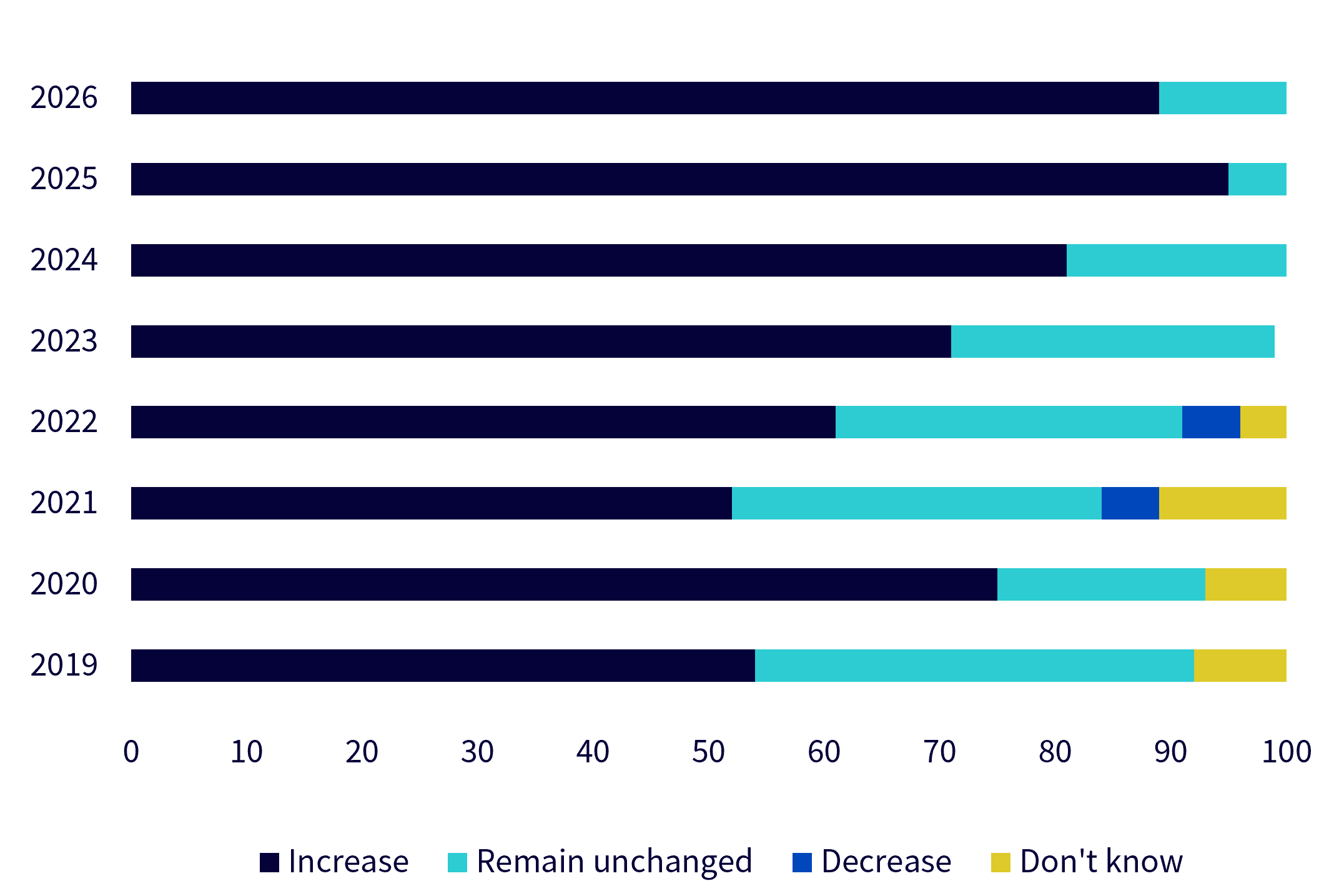

The first FOMC meeting under Chairman Kevin Warsh featured a streamlined policy statement, marking the beginning of a broader reduction in forward guidance. As a result, markets are likely placing greater emphasis on the guidance that remains. The so-called ‘dot plot’, which shows where individual policymakers expect interest rates to be at year-end, revealed that nine of the eighteen participants projected at least one rate hike by the end of 2026 (Figure 1).

Although markets had already been pricing in a rate increase this year, the latest projections reinforced those expectations. Fed funds futures are now pricing a full rate hike as early as October, compared with expectations closer to December prior to the meeting. Strength in the labour market, reflected in firmer payroll growth, alongside persistently elevated inflation readings, has strengthened the case for tighter monetary policy.

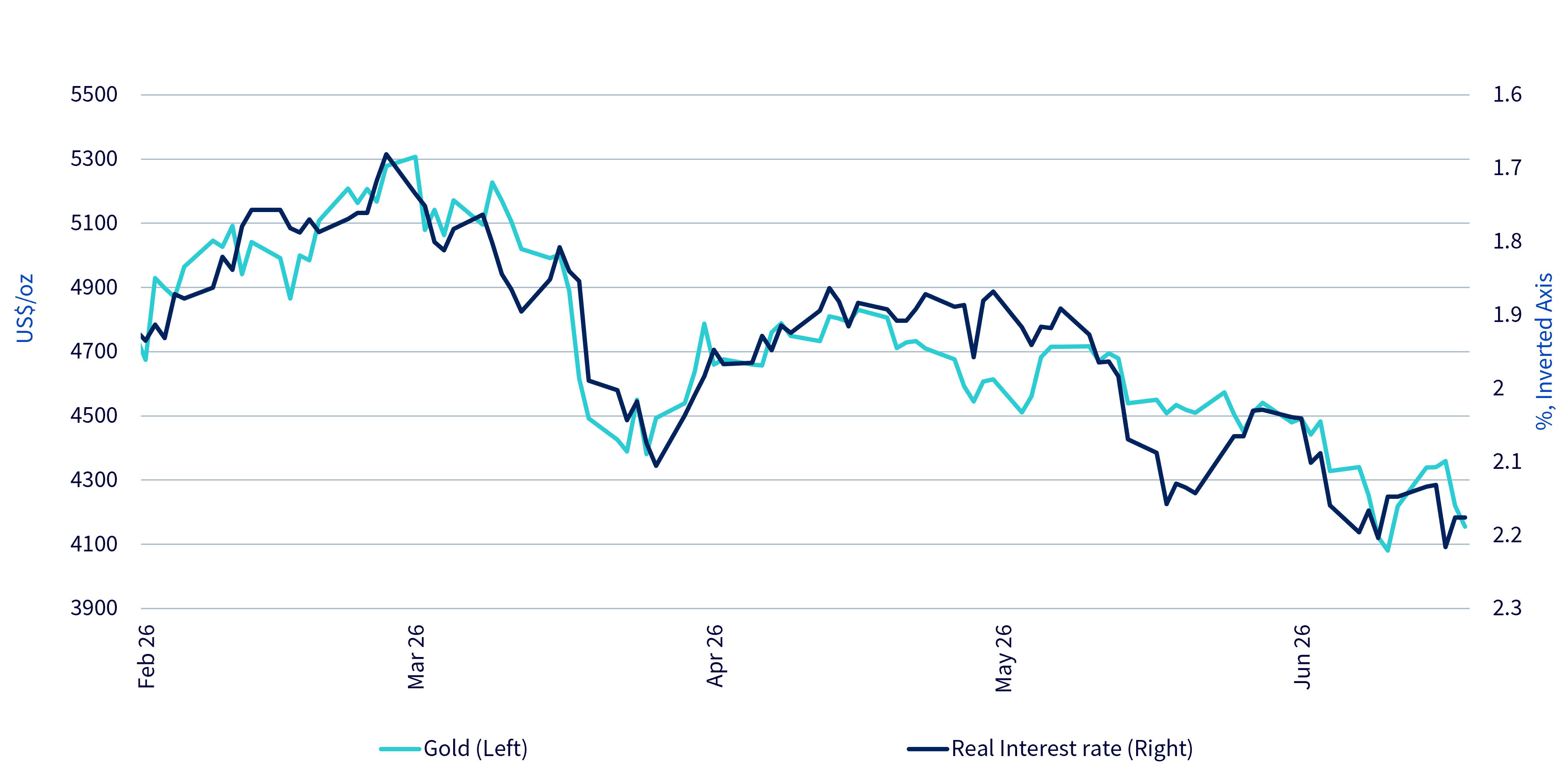

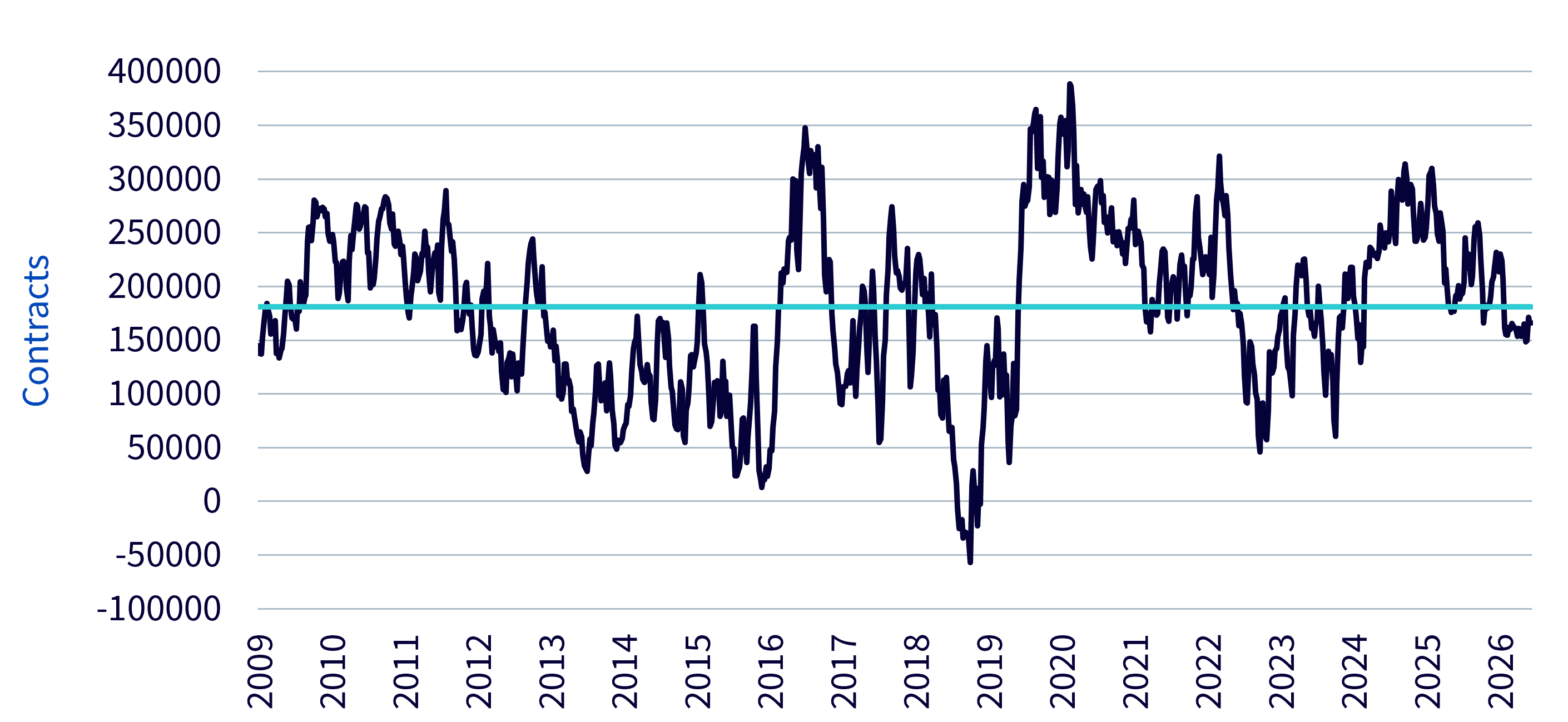

Real rates, as measured by Treasury Inflation-Protected Securities (TIPS) yields, have been rising and have therefore exerted downward pressure on gold in recent months. While gold and real yields appeared to decouple for several years, their historically negative relationship seems to have reasserted itself more recently (Chart 2).