WisdomTree US Efficient Core UCITS ETF: heralding a new era of smart investing

Published 17 October 2023

Head of Research, WisdomTree Europe.

When aiming to improve the risk-return profile of their investments, investors have two main tools at their disposal: diversification and leverage. Diversification uses low-correlation assets to diversify the overall risk and create more efficient portfolios. Leverage can help target the amount of risk that investors are looking for.

Take the example of a US equity/US Treasury portfolio. Adding 40% of fixed income to an equity portfolio helps reduce the volatility from 18.6%1 to 12.2% and, more importantly, move the Sharpe ratio from 0.38 to 0.46. Incidentally, the return is diminished from 10.3% per annum to 8.9%. By leveraging this new portfolio back to equity-like volatility, investors can keep the Sharpe ratio at 0.43 and, therefore, outperform equities (+11.5%) with a more efficient portfolio. Diversification and leverage really work hand in hand to deliver the most efficient portfolios, as illustrated in more detail in our recent blog, Reduce risk in portfolios without hampering returns – introducing ‘Efficient Core’.

While sophisticated investors have been using leverage in their portfolios for decades, the concept of ‘Portfolio Scaling’ (that is, the practice of combining multiple investment strategies or assets through leverage to generate higher returns and improve diversification) is slowly gaining a larger user base. The WisdomTree US Efficient Core UCITS ETF is WisdomTree’s offering to provide a turn-key solution for investors to improve their portfolios.

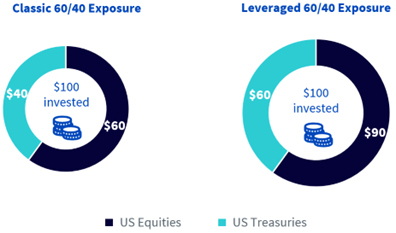

The WisdomTree US Efficient Core UCITS ETF aims to deliver a 90% exposure to ESG-screened, large-cap US equities and 60% exposure to US Treasury Bonds, effectively delivering a 150% leveraged position to the traditional 60/40 portfolio.

Figure 1: Exposure in the WisdomTree US Efficient Core UCITS ETF

Source: WisdomTree.

The exchange-traded fund (ETF) is comprised of three key exposures:

- Equity: the strategy invests 90% physically in a diversified basket of ESG-screened, US large-capitalisation companies

- Bond: the strategy has a 60% exposure in a diversified basket of 5 US Treasury futures contracts laddered across 2 to 30 year maturities

- Cash collateral: the strategy has roughly 10% exposure in cash, which serves as collateral for the US Treasury future contracts

1. The equity exposure

The strategy invests 90% of its assets quarterly in the S&P 500 net total return.

2. The bond exposure

The strategy achieves a 60% bond exposure by investing in liquid US Treasury futures contracts using the 10% of cash collateral to fund the margin account. The futures portfolio comprises an equal-weight basket of US Treasury futures contracts with maturities ranging from 2 to 30 years . The Index implements a ‘rolling’ methodology to replace the ‘first near futures contract’ (the front month contract) into the ‘second near future contract’, which occurs over a one-day rolling period every quarter.

3. The cash collateral

The cash collateral returns the US Secured Overnight Financing Rate.

All weights are rebalanced, and contracts are rolled every quarter on the last business day of February, May, August and November. The strategy allows intra-quarter exceptional rebalancing in case the equity/bond exposures deviate by more than 5% from the target weights.

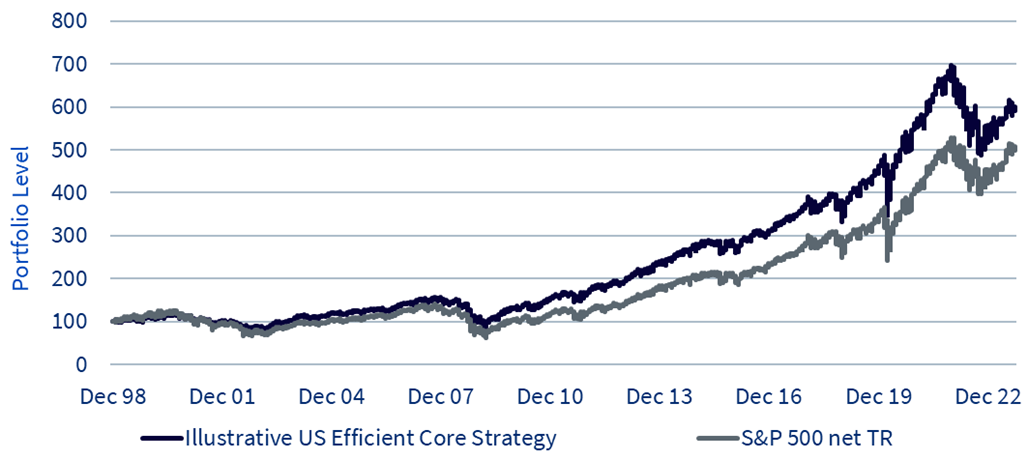

In Figure 2, we run the backtest of the WisdomTree US Efficient Core UCITS ETF since December 1998, with the caveat that we use the S&P 500 for the equity exposure instead of the ESG-filtered basket we use in the ETF itself to increase the length of the backtesting period. This includes the 20 bps TER.

The strategy outperforms a 100% equity investment by 1% a year thanks to its leverage and the diversification brought upon by the bond futures. The volatility is also reduced by almost 3%. This translates into a Sharpe ratio of 0.35 compared to 0.25 for the S&P 500 alone.

Figure 2: Historical backtest of the WisdomTree US Efficient Core UCITS ETF

WisdomTree US Efficient Core UCITS ETF | ||

|---|---|---|

Return | ||

Total return | 521.7% | |

Total return (Annualised) | 7.7% | |

Risk | ||

Standard Deviation (annualised) | 17.0% | |

Skewness | -12.6% | |

Daily VAR 95% | -1.6% | |

Tracking Error (Annualised) | 4.3% | |

Risk Return | ||

Sharpe Ratio | 0.35 | |

Information Ratio | 0.22 | |

Treynor Measure | 6.93 | |

Beta (ex post) | 85.0% | |

Correlation | 98.3% | |

Source: Bloomberg, WisdomTree. From December 1998 to August 2023. Daily data in USD. Historical performance is not an indication of future performance and any investments may go down in value.

One ETF, two potential uses in portfolios

Such ‘Efficient Core’ ETFs could be used widely in investors’ multi-asset portfolios as:

1.An equity replacement

A core equity solution designed to replace existing core equity exposures. By offering return enhancement, lower risk and a better Sharpe ratio historically compared to a 100% equity portfolio, the WisdomTree US Efficient Core UCITS ETF could be used to replace existing equity exposures.

In Figure 3, we compare the performance of the backtest of the WisdomTree US Efficient Core UCITS ETF with all the ETFs and mutual funds domiciled in Europe that track US equities and have at least a 5-year track record. This includes 647 ETFs and funds in the Morningstar US Large Cap Value peer group, the Morningstar US Large Cap Blend peer group, the Morningstar US Large Cap Growth peer group, and the Morningstar US Equity Income peer group.

The Illustrative US efficient core strategy beats 421 of those 647 funds and ETFs. The strategy is, therefore, in the top 35%. Furthermore, it has a better Sharpe ratio than around half of the funds.

Figure 3: Backtest of WisdomTree US Efficient Core UCITS ETF versus all passive and active funds in Morningstar US Large Cap Peer Groups (Value, Blend, Growth, Equity Income)

Source: Morningstar, WisdomTree. December 1998 to August 2023. in USD. Historical performance is not an indication of future performance and any investments may go down in value.

2.A capital efficiency tool

By delivering equity and bond exposure in a capital-efficient manner, ‘Efficient Core’ can help free up space in a portfolio for alternatives and diversifiers. If an investor were to allocate 10% of a portfolio to this strategy, investors would get 9% exposure to US equities and 6% exposure to US Treasuries. This could allow investors to divest 6% from existing fixed income exposures and invest that in alternative assets (such as broad commodities, gold, carbon or other assets). This could be achieved without losing the diversifying benefits of their fixed income exposure.

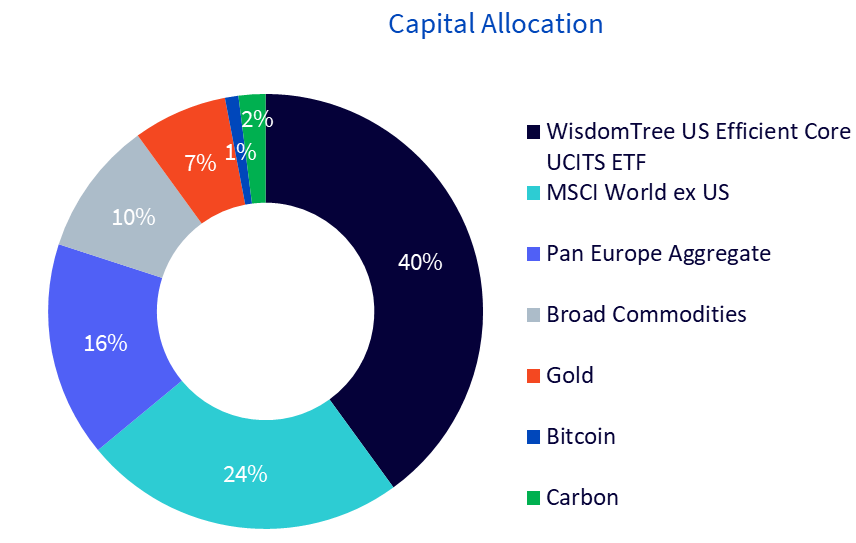

Using the WisdomTree US Efficient Core UCITS ETF, it is possible to keep both the equity and bond allocation steady while fitting new diversifiers. Figure 4 shows a portfolio where the Efficient Core ETF creates space for commodities and other diversifiers. The Illustrative WisdomTree Efficient Core Model Portfolio invests its US equity exposure in the WisdomTree US efficient Core UCITS ETF, creating 20% of space. That 20% could then be invested in assets like broad commodities, gold, bitcoin and carbon, delivering a very diversified portfolio.

Without leverage, the portfolio would be under-invested in equities. However, from an exposure point of view, thanks to the leverage in the Efficient Core strategy, the portfolio delivers 60% to equities, 40% to bonds and 20% to diversifiers.

Figure 4: Capital allocation and exposures in the Illustrative WisdomTree Efficient Core Model Portfolio

Capital Allocation | Equity | Fixed Income | Commodities | ||

|---|---|---|---|---|---|

WisdomTree US Efficient Core UCITS ETF | 40% | 36% | 24% | ||

MSCI World ex US | 24% | 24% | |||

Pan Europe Aggregate | 16% | 16% | |||

Broad Commodities | 10% | 10% | |||

Gold | 7% | 7% | |||

Bitcoin | 1% | ||||

Carbon | 2% | 2% | |||

Total | 100% | 60% | 40% | 19% | |

By offering investors more efficient building blocks, Efficient Core unlocks many possibilities to improve portfolios. The WisdomTree US Efficient Core UCITS ETF could be used to replace existing equity exposure or it could create space in portfolios for well-needed diversifiers.

Related products

Categories

About the contributor

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.