DEM LN

WisdomTree Emerging Markets High Dividend UCITS ETF

Published 23 February 2026

Director, Research

Senior Associate, Quantitative Research

The fact that the S&P500, America’s most representative equity index, remains close to its historical highs conceals a very different reality beneath the surface.

Since November 2025, the market has not experienced a linear correction. Instead, it has undergone a sharp and selective rotation across investment themes, dramatically reshaping sector leadership.

The segments that have suffered the most are those traditionally classified as “growth”: high-growth technology, software, richly valued semiconductors, premium consumer discretionary and luxury names, and the more speculative and volatile AI-linked stocks. Many of these have experienced significant drawdowns, frequently recording single-day losses exceeding 5–7%.

This dynamic has been driven by two main factors. First, multiple compression in an environment where interest rates remain elevated and monetary policy expectations are less accommodative. Second, the unwinding of ultra-crowded trades, as investors took profits on names that had delivered extraordinary returns over the past 12–18 months. Stocks with the highest valuations and strongest operating leverage have shown amplified volatility.

At the same time, previously overlooked areas of the market, generally categorized as value and traditional cyclicals, have staged a meaningful recovery. Energy, Industrials, Materials, Staples as well as U.S. small and mid-cap stocks, have benefited from expectations of macro stabilization and potential improvement in the domestic economic cycle.

More broadly, the market is rewarding companies with more reasonable valuations and sustainable dividend profiles.

In an environment of heightened uncertainty, investors are favoring stable cash flows and stronger balance sheets over aggressive growth assumptions. What is unfolding is a transition from concentration to dispersion. In recent years, leadership within the S&P500 was heavily concentrated in a small number of mega-cap growth stocks.

Today, a broader and more diversified leadership structure is emerging. The index remains resilient near its highs not because of uniform strength, but thanks to the resilience of new leaders, often outside the well-known “Magnificent 7.”

Investors are migrating toward less expensive and more economically sensitive sectors. So far, this is not a systemic sell-off, but rather a reallocation of risk.

The key question is whether this represents a short-term tactical rotation, following growth’s extended outperformance, or the beginning of a more structural transition toward a market less dependent on mega-cap technology and long-duration growth narratives.

The current phase reflects a recomposition of investor preferences. Exposure to crowded growth themes is being reduced, while cyclical and lower-valuation segments are being rediscovered.

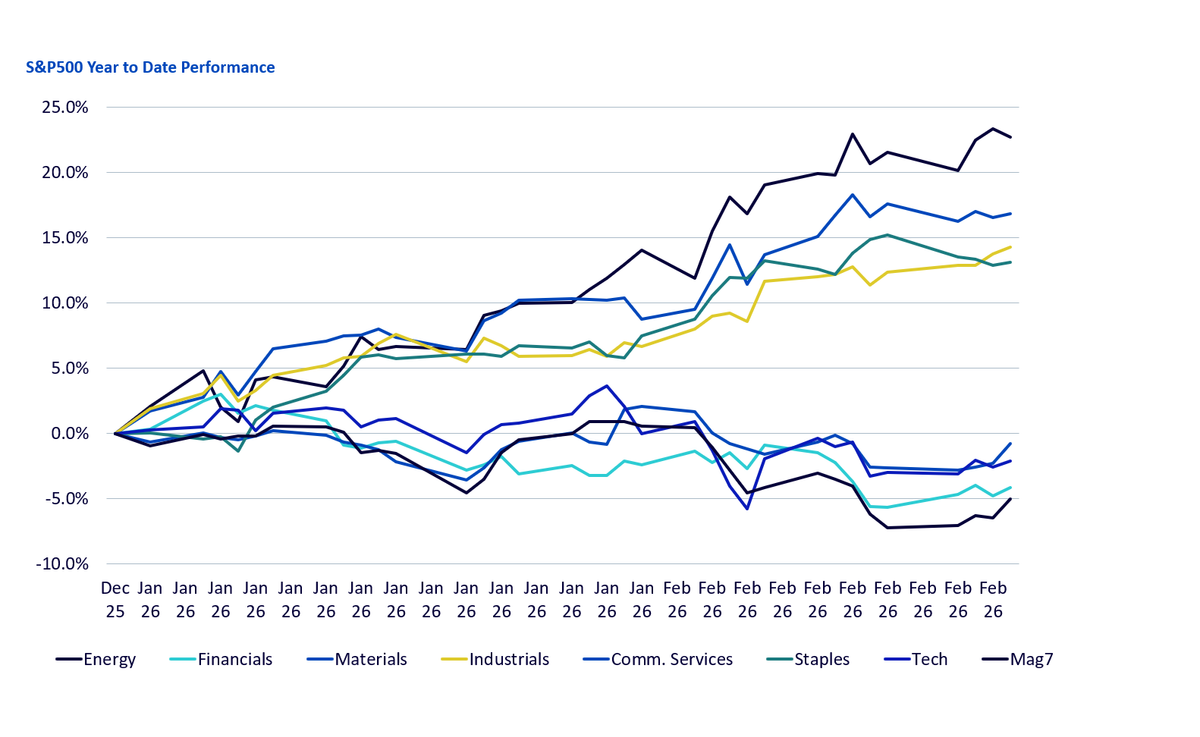

Sector trends clearly illustrate the intensity of the rotation, with concerns surrounding the rapid diffusion of Artificial Intelligence (AI) playing a central role in reshaping the map of winners and losers.

Recent winners include Energy, Materials, Consumer Staples, and Industrials. Meanwhile, Information Technology, Communication Services, and certain areas of Financials have underperformed alongside the Magnificent 7.

Source: Bloomberg as of 20 February 2026. Sector performance represented by respective S&P Select Sector Total Return Indexes. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

The key message is straightforward: the market is not declining; it is changing leadership. The shift is moving from growth and long-duration themes (particularly software-as-a-service and high-performance chips) toward value-oriented cyclicals, defensive cash-flow sectors such as staples, and other parts of the real economy.

A broader re-rating process is underway. Growth and duration-sensitive stocks remain highly sensitive to real yields and interest-rate expectations. As rates stay elevated, multiples contract and profit-taking intensifies.

What is new in this cycle is that AI is no longer perceived solely as a growth story; it has increasingly become a story about capital intensity and potential disruption.

Major technology companies are planning data center investments approaching $650 billion in 2026, raising questions about near-term profitability and capital discipline. Concerns that part of this spending may be less accretive than anticipated have supported rotation toward sectors such as Energy and Materials, which benefit more directly from infrastructure expansion. More broadly, AI is structurally supportive for physical and digital infrastructure — including power generation, grids, data centers, industrial automation, and selected semiconductor niches. Morgan Stanley has described this dynamic as the “HALO trade” (Hard Assets, Low Obsolescence), highlighting assets perceived as less vulnerable to rapid technological displacement.

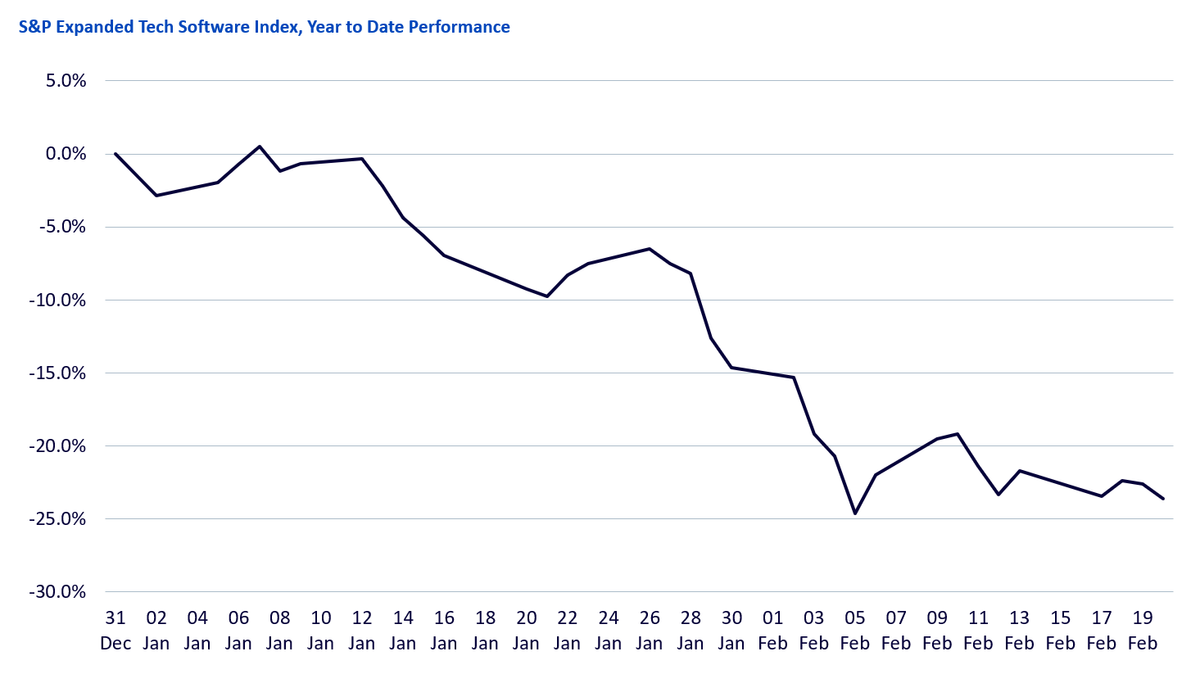

On the other hand, AI introduces the risk of disruption and commoditization. Rather than serving purely as a productivity tool, AI may compress pricing power in areas such as enterprise software, repetitive IT services, data providers, and digital advertising. The reassessment of business models built on recurring revenue and high margins has contributed to sharp year-to-date declines in several large-cap software names — in what some have labeled a “SaaSpocalypse.”

Source: Bloomberg as of 20 February 2026. Software performance represented by the S&P North American Expanded Technology Software Total Return Index. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

An additional catalyst has emerged through the Supreme Court ruling invalidating certain IEEPA-related tariffs. If sustained, the decision could reduce previously quantified earnings headwinds for U.S. industrial and consumer-facing companies. The potential recovery of previously paid tariffs may represent a one-off margin benefit for firms with material exposure, including select exporters in Japan and Europe. This development reinforces the relative strength in cyclical and export-oriented segments.

The S&P500’s proximity to its all-time high masks exceptionally high dispersion beneath the surface. Leadership is in transition, not collapse. AI continues to act as an accelerator of this rotation, driving infrastructure investment while increasing disruption risk across parts of software and digital services.

In this environment, cash-flow durability and valuation discipline are increasingly important. Companies with strong balance sheets and measured AI exposure appear better positioned as dispersion persists. Income-oriented equities, cyclicals, and exporters benefiting from tariff relief continue to reflect the market’s evolving leadership in early 2026.

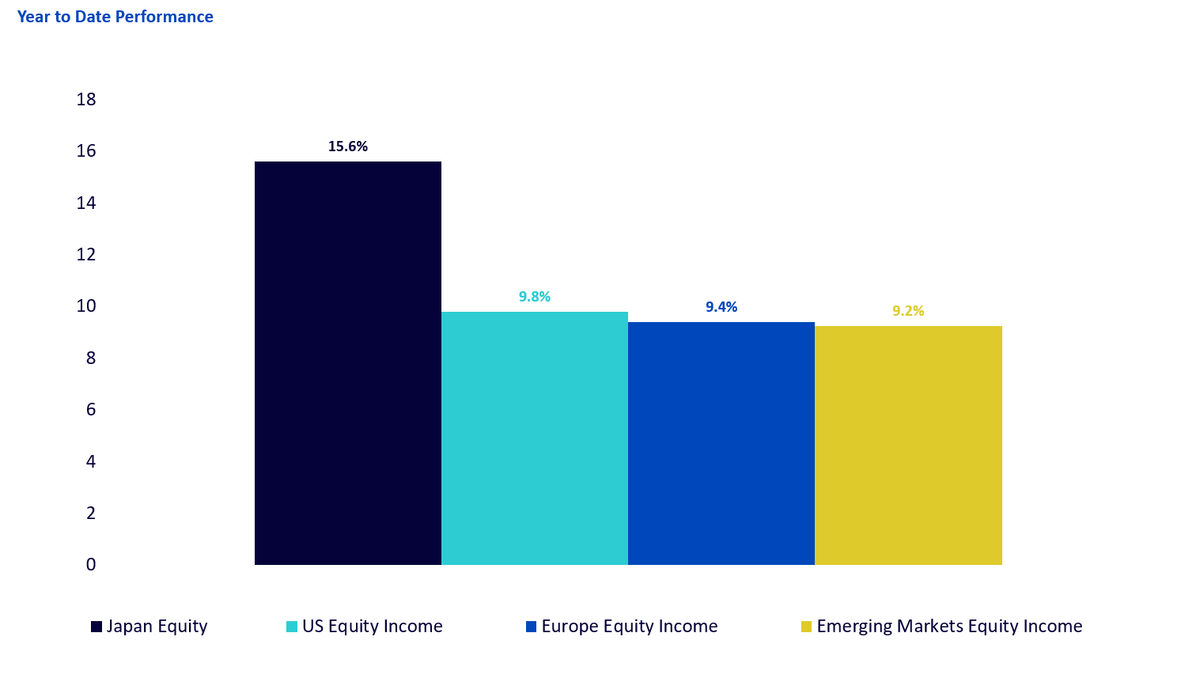

Several targeted fund categories align with the ongoing rotation toward cyclicals, exporters, valuation discipline, and income durability. The WisdomTree Japan Equity UCITS Fund (+15.6% YTD) provides exposure to Japanese exporters benefiting from tariff relief and improving global trade dynamics, while mitigating yen volatility.

The WisdomTree Emerging Markets Equity Income UCITS Fund (+9.2% YTD) and WisdomTree Europe Equity Income UCITS Fund (+9.4% YTD) offer diversified exposure to dividend-paying companies with cyclical and export-oriented characteristics in regions demonstrating relative strength.

Complementing these, WisdomTree US Equity Income UCITS strategies (+9.8% YTD) emphasize durable cash flows, reasonable valuations, and strong balance sheets — characteristics that align with the current shift away from speculative growth toward income stability and valuation discipline.

As dispersion persists and leadership continues to broaden into early 2026, income-oriented and internationally diversified exposures may offer a structured way to participate in the reallocation while reducing concentration risk tied to mega-cap growth.

Source: Bloomberg as of 20 February 2026. Software performance represented by the S&P North American Expanded Technology Software Total Return Index. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Director, Research

Piergiacomo is Director of Research at Wisdomtree. He has over 20 years of experience within the financial services industry, having served as the Head of Discretionary Portfolio Management at Banca Albertini Spa in Milan before joining WisdomTree. Prior to this, he held roles at Rasbank Spa (currently AllianzBank Financial Advisors) as Head of Equity Research and Head of Equity Desk. Piergiacomo has an M.Sc. in Financial Markets Economics from Bocconi University in Milan. He is also a chartered member of the Aiaf (Italian Association of Financial Analysts).

Senior Associate, Quantitative Research

Blake Heimann joined WisdomTree in 2020 and, in his current role as Senior Associate, supports the creation, maintenance, and reconstitution of our indices. Blake began his career in finance in 2017 as an Analyst at TD Ameritrade, and later a Quantitative Analyst with focuses on research and development of machine learning applications in finance. Blake has bachelor’s degrees in Mathematics and Economics from Iowa State University, as well as his Masters in Computer Science at Georgia Tech, with a specialization in Machine Learning. He is currently pursuing a Masters in Finance from the London School of Economics.