Weak energy prices amidst COVID-19 pandemic to drag sugar lower

Published 13 May 2020

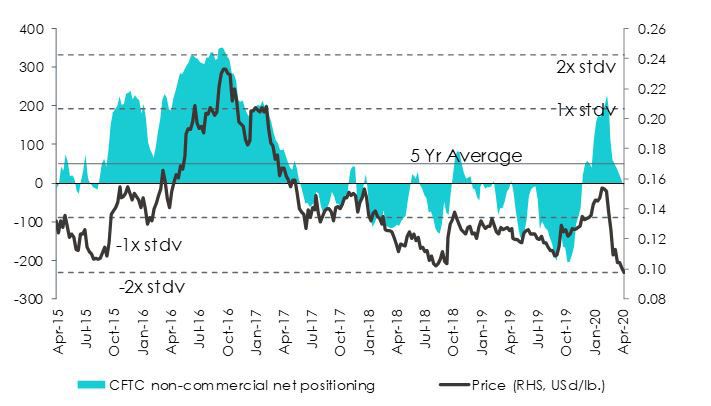

Sugar prices have slumped to 9.34 cents1, reaching its lowest level in a front-month contract since September 2007. The rapid decline of energy prices due to a combination of supply and demand shocks amidst the COVID-19 pandemic is having a widespread negative impact on sugar prices since sugar cane is one of the products used to make ethanol. The slump in energy prices has dragged down ethanol prices making it less attractive to produce. Net speculative futures positioning on sugar futures have declined 120%2 over the prior month owing to a 49% increase in short positions, underscoring the extent of the bearishness towards sugar prices.

Figure 1: Net Speculative positioning on sugar futures decline sharply

Source: Commodity Futures Trading Commission, WisdomTree as of 21 April 2020. Please note: Standard deviation measure of the amount of variation or dispersion of a set of values.

Historical performance is not an indication of future performance and any investments may go down in value.

Lower demand for ethanol in Brazil to weigh on sugar prices

In prior seasons, amidst an ample supply situation, only 34% of the sugar cane was processed into sugar in 2019/20 crop year and 35% in 2018/19 crop year in Brazil. The processing season in Brazil, the world’s largest sugar exporter, is currently under progress. At low energy prices, the demand for alternative fuels such as ethanol decreases, owing to which we now expect a higher proportion of sugar cane to be processed into sugar. Brazil has an extensive fleet of flex-fuel vehicles that can run on either gasoline or ethanol. The Brazilian ethanol sector has requested for financial assistance from the government to enable it to store six billion litres of ethanol in anticipation of a decline in demand for ethanol. In addition, the weak Brazilian real is also weighing on sugar prices. The Brazilian real is the weakest emerging market currency year to date in 20203, which is likely to incentivise higher sugar exports from Brazil on the global sugar market. Since the weaker real encourages producers to offer more sugar on the export markets as it increases their revenue in USD terms.

Sugar consumption to face headwinds amidst the COVID-19 pandemic

Industrial consumption of sugar is likely to weaken as food and beverage plants are negatively impacted owing to production halts at beverage plants and partial lockdown of restaurants. While household sugar consumption is unlikely to see much change and could rise it will not be enough to offset industrial consumption. During the great financial crisis, global sugar consumption growth declined by 2% in the 2008/09 crop year. Using this as an indication, global sugar consumption could slow down by a comparable amount until the lockdowns persist.

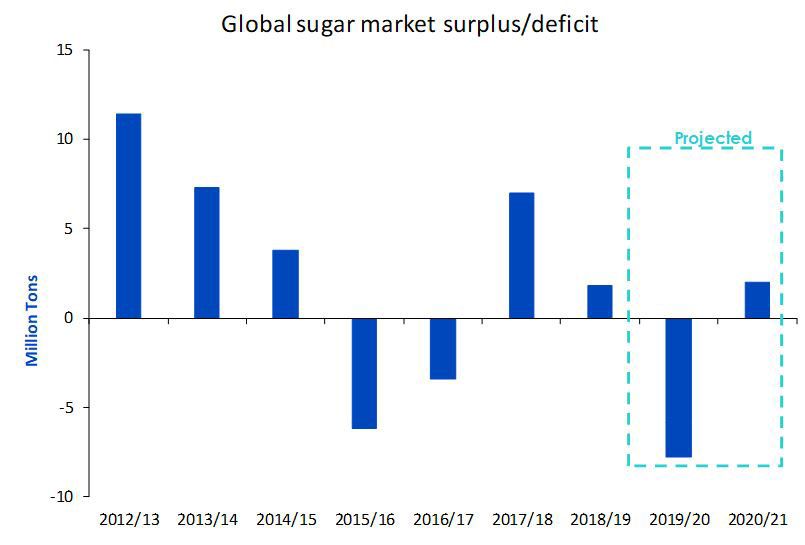

The global sugar market in 2020/21 crop year is likely to rebalance

According to the Brazilian consultant for Job Economia, Brazil is expected to produce 41mn tons of sugar in 2020/21, compared with 30mn tons in 2019/20. The country is also set to export around 30mn tons of sugar in 2020/21.

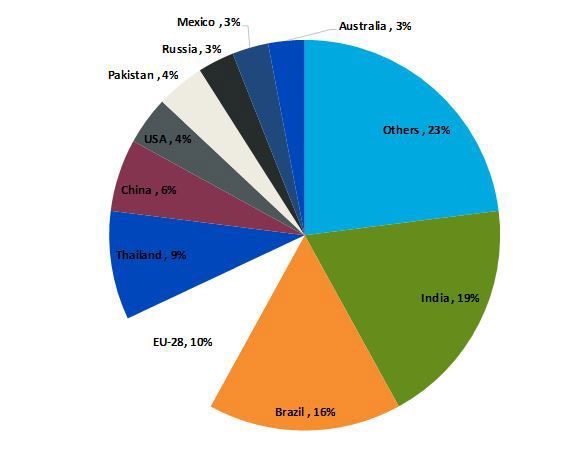

Figure 2: Share of the biggest sugar producers in 2018/19 crop year

Source: WisdomTree, International Sugar Organisation as of 31 December 2019.

However, in Thailand (the world’s second largest exporter) sugar cane processing is likely to have decreased to a ten-year low of 75mn tons in the 2019/20 crop year owing to the drought. In India, the first excess monsoon in 25 years bought major delays to India’s crushing activity this crop year and the COVID-19 outbreak caused a further production delay. Owing to which, sugar production was down 13% year on year by mid-April and should finish the year at a low 27mn tons, before recovering to 2020/21 crop year to above a 30mn ton level. In the European Union (EU) nations, total sugar production is expected to remain flat from last year at 16.2mn tons as crop yields recover from a 5-year low. In China, sugar production looks in line with the last crop year and could end the year at 10mn tons. Against the backdrop of high production from Brazil, one of the largest suppliers, it is becoming more likely that the global sugar market will return to a surplus in the 2020/21 crop year adding further pressure on sugar prices ahead.

Figure 3: The global sugar market is likely to return to surplus in 2020/21 crop season

Source: International Sugar Organisation, WisdomTree as of 24 April 2020. Historical performance is not an indication of future performance and any investments may go down in value. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

1 Bloomberg as on 28 April 2020

2 Commodity Futures Trading Commission from 24 March 2020 to 21 April 2020

3 Bloomberg, Brazilian Real versus the US dollar -26.45% from 31 December 2019 to 28 April 2020

Related blogs

+ Prospect of a surplus to weigh on coffee prices ahead

Related products

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.