WCOA LN

WisdomTree Enhanced Commodity UCITS ETF USD Acc

Published 19 September 2025

Associate Director, Quantitative Research at WisdomTree in Europe

When we first launched the WisdomTree Enhanced Commodity UCITS ETF (WCOA) , our focus was clear: reduce one of the main drags in commodity investing – roll costs – by optimising contract selection along the futures curve. That optimisation worked well: WCOA’s underlying total return index1 outperformed the Bloomberg Commodity Total Return Index by 12.2% since its launch2.

But today’s macro backdrop – persistent inflation risk, recurring supply frictions, and faster-moving curve dynamics – puts pressure on investors to use a more unconstrained, research-driven approach that isn’t overly tied to the benchmark. We’ve upgraded WCOA to keep the same broad Bloomberg Commodity Index (BCOM) universe while adding a factor-based framework that can overweight and underweight commodities as well as select contracts more intelligently, all with disciplined risk controls embedded in the index design.

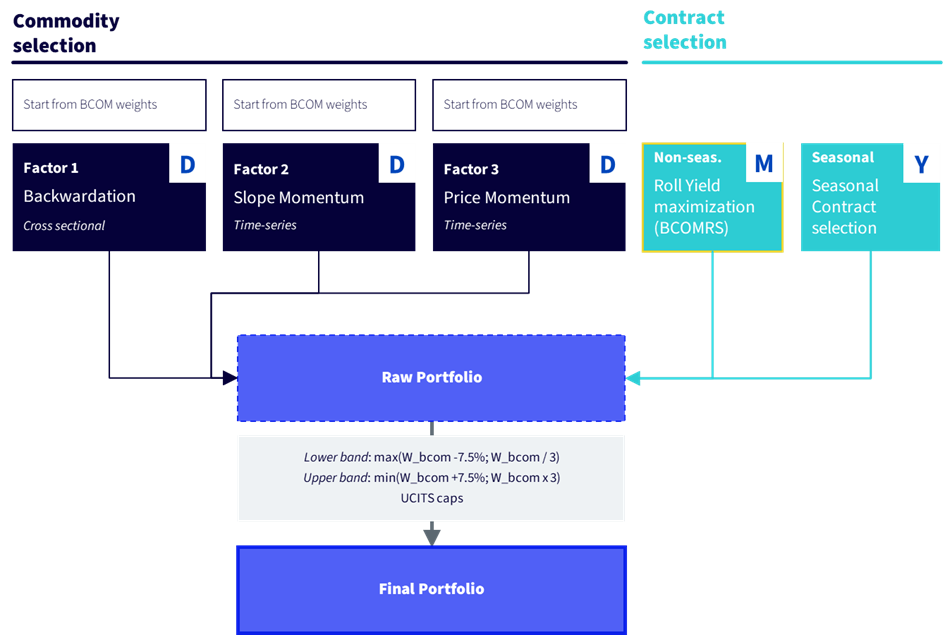

Source: WisdomTree. “D” stands for “Daily rebalance”, “M” stands for monthly rebalance and “Y” stands for annual or semi-annual rebalance. “Non-seas.” Stands for non-seasonal commodities. “Seasonal” stands for seasonal commodities. “BCOMRS” stands for Bloomberg Roll Select Methodology.

Previously, WCOA focused exclusively on contract selection. The updated WCOA combines both contract selection and commodity selection (see Figure 1), offering a more comprehensive toolkit. The improvements can be summarised in three key changes:

One of the main innovations of the new strategy lies in how WCOA allocates across commodities. The strategy starts from the Bloomberg Commodity Index (BCOM) weights but then applies three academically backed factors that have been shown to generate excess returns:

Each factor produces a signal for every commodity, scaled between -1 and +1, where positive values indicate overweight positions and negative values indicate underweights. By combining the three signals equally, the strategy diversifies alpha sources across slow-moving (cross-sectional backwardation), medium-term (price momentum), and fast-reacting (slope momentum) factors, reducing reliance on any single style. Each factor is rebalanced daily.

Notably, the signals are calculated but not applied to gold and silver, which effectively assigns them a neutral baseline factor value. As a result, they act as implicit risk-off hedges within the portfolio: their relative allocation declines when other commodities exhibit strong positive signals and are subsequently overweighted. Conversely, when few commodities are supported by strong signals, gold and silver gain in relative weight, providing a defensive tilt during periods of broader market stress.

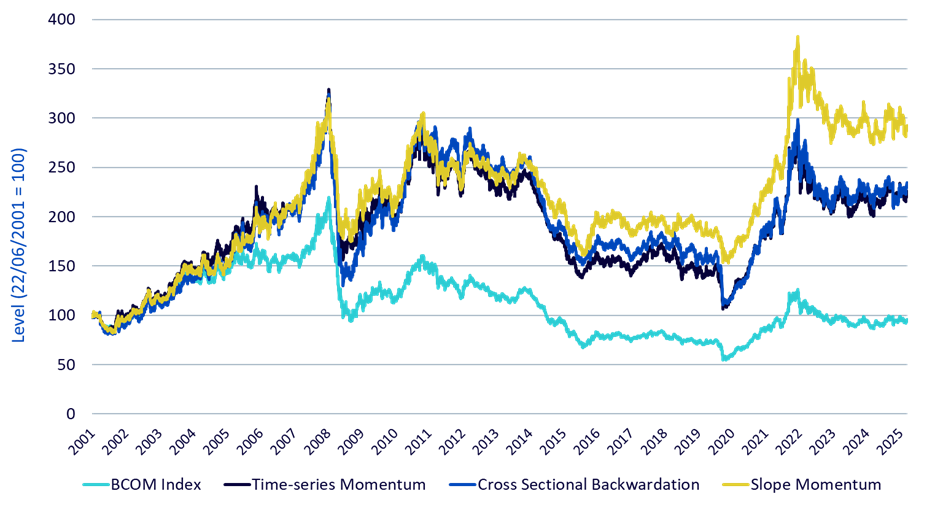

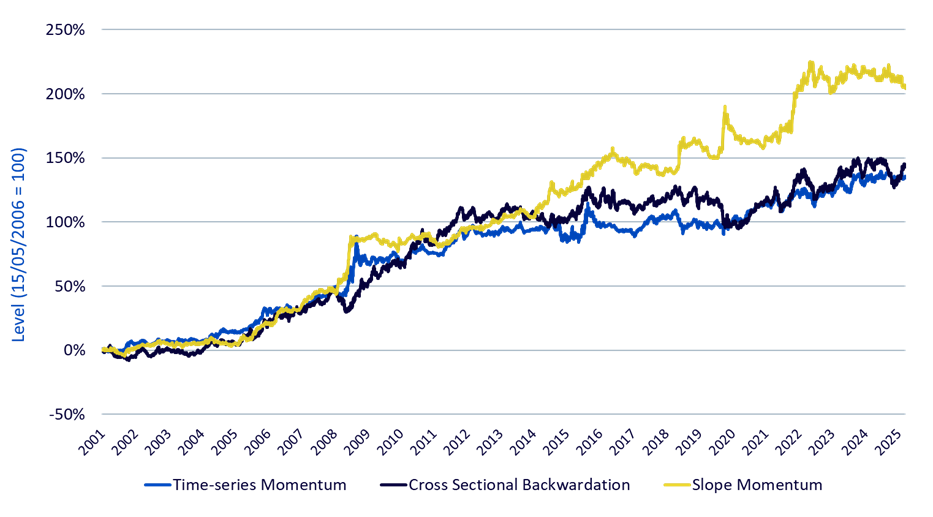

The two charts below show how each factor behaved over time, in absolute terms (Figure 1) and in relative terms (Figure 2) vs BCOM4. As it is clear, in the last 25 years, the three factors delivered substantial excess returns.

Sources: WisdomTree, Bloomberg. Data from 22/06/2001 to 10/09/2025. Calculations are based on excess return indices and include backtested data. Historical performance is not an indication of future performance and any investments may go down in value.

Sources: WisdomTree, Bloomberg. Data from 22/06/2001 to 10/09/2025. Calculations are based on excess return indices and include backtested data. Historical performance is not an indication of future performance and any investments may go down in value.

Futures curves carry valuable information not only about commodity performances but also about the behaviour of individual contracts.

For non-seasonal commodities, the strategy continues to follow a roll-yield maximisation philosophy through Bloomberg’s Roll Select (BCOMRS) methodology. Each month, the methodology selects the contract with the most attractive roll yield, subject to a nine-month maturity cap. This ensures efficient positioning along the curve, further improving the carry profile of the strategy.

For seasonal commodities such as natural gas or agricultural products, the strategy targets the so-called “seasonal contract”, the futures contract whose delivery month aligns with predictable supply–demand cycles. This approach avoids selecting a high roll-yield contract where the signal is driven by seasonality rather than genuine market tightness. At the same time, it allows the strategy to capture the seasonal premium often created by strong hedging pressure. Because this premium typically erodes as maturity approaches, the methodology proactively rolls into the next seasonal contract two months before expiry, ensuring the premium is harvested without being diluted by the convergence of fundamentals.

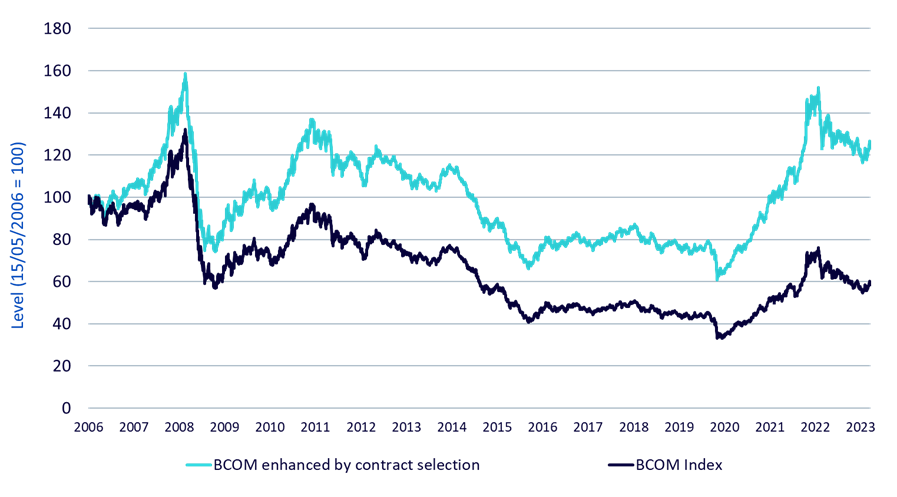

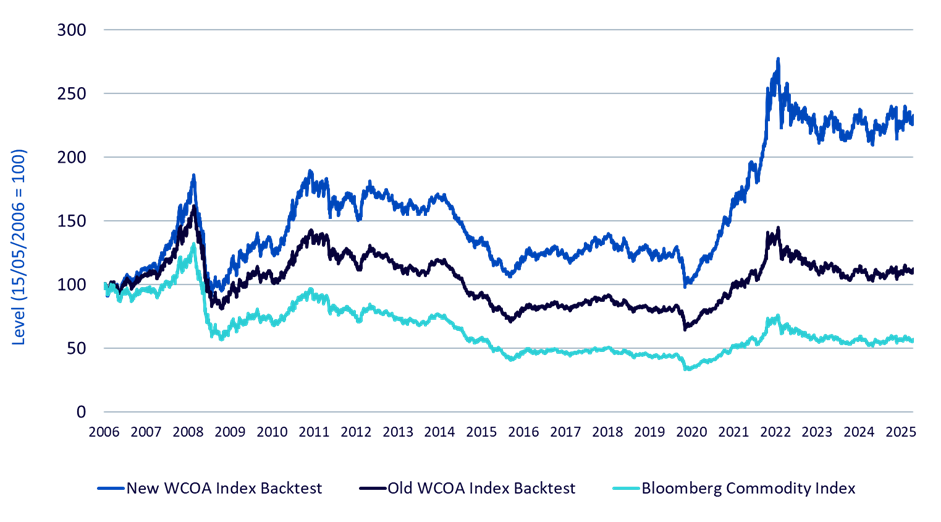

Together, these rules ensure that both seasonal and non-seasonal commodities are handled optimally. The chart below (Figure 4) compares the Bloomberg Commodity Index with an enhanced version that keeps the same BCOM weights but replaces BCOM’s standard contract choices with the contract selection methodology used in the new strategy.5

Sources: WisdomTree, Bloomberg. Data from 15/05/2006 to 10/09/2025. Calculations are based on excess return indices and include backtested data. Historical performance is not an indication of future performance and any investments may go down in value.

Stacking it all up: strategy performance

The new WCOA combines two complementary engines – commodity selection and contract selection – into a single, disciplined framework.

Starting from BCOM weights, three factors – price momentum, cross-sectional backwardation, and slope momentum – adjust allocations daily. Caps and floors keep tilts diversified, ensuring no commodity is excluded while still allowing meaningful factor exposures.

Alongside, contract selection optimises carry: roll yield maximisation for non-seasonal commodities, and seasonal contracts for seasonal commodities to capture the seasonal premia.

The result, shown in Figure 5 and Figure 6, is a clear performance enhancement accompanied by lower volatility (15.7% annualised for WCOA’s excess return index versus 16.5% for BCOM) and a markedly smaller maximum drawdown (-51.1% versus -75.0%). The improvement is also clear vis-à-vis the previous WCOA strategy.

Sources: WisdomTree, Bloomberg. Data from 15/05/2006 to 10/09/2025. Calculations are based on excess return indices and include backtested data. Historical performance is not an indication of future performance and any investments may go down in value.

15/05/2006 - | WTENCME Index | EBCIWTE Index | BCOM Index |

|---|---|---|---|

Cumulative Return | 133.1% | 12.3% | -42.8% |

Annualised Return | 4.5% | 0.6% | -2.9% |

Volatility | 15.3% | 13.8% | 16.0% |

Sharpe | 0.29 | 0.04 | - |

Max Drawdown | -51.1% | -60.1% | -75.0% |

Correlation | 94.7% | 96.3% | - |

Information Ratio | 1.43 | 0.75 | - |

Source: WisdomTree. Historical performance is not an indication of future performance and any investments may go down in value.

In short, WCOA has evolved from a contract-optimised commodity index into a factor-driven, contract-smart strategy that blends academic research with daily discipline – and now rebalances every day to stay aligned with fast-moving markets. Or put another way: same broad commodity exposure, now with smarter tools and faster reactions under the hood.

1The Optimized Roll Commodity Total Return Index (Bloomberg ticker: EBCIWTT Index)

227th of April 2016

3Two types of bounds apply: absolute and relative. The absolute bounds are ±7.5% around each BCOM weight. Relative bounds are one-third and three times the BCOM weight, ensuring no commodity is ever excluded.

4Each factor performance is obtained by multiplying each commodity BCOM’s weight by 1 plus the commodity signal (i.e. commodity weights with signal 1 will see their weight doubled, while commodity weights with signal -1 will see their weight zeroed), before rescaling the weights.

5Source: Wisdomtree, Bloomberg. The non-seasonal commodities are: WTI Crude, Brent Crude, Copper (COMEX), Coffee, Aluminum, Lead, Nickel, Zinc, Gasoil. The seasonal commodities are: Soybean Oil Corn, Cotton, ULS Diesel, HRW Wheat, Live Cattle Lean Hogs, Natural Gas, Soybean, Sugar Soybean Meal, SRW Wheat, Gasoline, RBOB Gasoline. Gold and silver are invested in the front BCOM contract.

WisdomTree Enhanced Commodity UCITS ETF USD Acc

Associate Director, Quantitative Research at WisdomTree in Europe

Luca is an Associate Director in WisdomTree Europe's Research team, where he conducts quantitative research to enhance or develop new investment strategies, particularly in commodities and thematic equities. He also focuses on portfolio construction and optimisation. Before joining WisdomTree in 2022, Luca worked as a Quantitative Portfolio Manager at Euclidea SIM, a Milan-based fintech where he quantitatively managed multi-asset portfolios and developed and implemented statistical and machine learning models for investment strategies and fund selection. Luca holds a Master's degree in Finance from Bocconi University, Milan.