DHS LN

WisdomTree US High Dividend UCITS ETF

Published 6 September 2024

Payrolls regained their crown as the key data point for stocks. The payrolls report came in somewhere in between at 142k – higher than the July report 114k but weaker than consensus estimates at 165k. A bigger concern was 85k downward revision for June and July adding to further concerns of softening of the labour market. However, on the positive side, the unemployment rate edged lower to 4.2%, marking the first decline in five months reflecting a reversal in temporary layoffs. In addition, average hourly earnings rose 0.4%.

Overall, the August payroll report came in stronger than July. The US economy continues to disprove sceptics. Growth has certainly cooled relative to the prior year, but it has done so at a gradual pace. The second print of the 2Q US GDP growth surprised to the upside at a robust 3%qoq, led by strong consumption growth of 2.9%. Given that 70% of the US economy relies on the consumer, concerns about the labour market can be eased when the economy sees 2.9% spending growth. Initial jobless claims inched lower to 231k and the four-week moving average dropped to 232k, well below a recessionary level of 300k.

Source: Bureau of Economic Analysis, WisdomTree as of 30 August 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

The August payroll report increased the odds for a 50Bps cut at the upcoming Federal Reserve meeting in September compared to 25Bps rate cut. Yet traders did not see the data as weak enough to definitively predict a 50Bps rate cut at the upcoming meeting. The 2s-10s slope steepened in the aftermath of the data release as shorter yields are declining as traders price in a faster pace of rate cuts by the Federal Reserve.

Source: Bloomberg, WisdomTree as of 6 September 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

As the US yield curve dis-inverts we expect to experience a more normal upward sloping yield curve over the next two years. This matters for investors. The short-term rates matter for stocks, in the case for financial, asset heavy and small cap stocks as they use shorter term funding on their balance sheets. As the yield curve dis-inverts i.e. as short rates decline even as long rates remain stable, the stocks (financial, asset heavy, small cap) that were hurt by the rising short rates could now benefit. While the long duration growth stocks won’t have a similar symmetric advantage as long rates are likely to stay positioned at current levels.

Rate cuts aid the broadening-out trade as defensive dividend paying stocks start to look more attractive. Cyclical stocks in the value trade (financials, energy, materials and industrials) should start performing better in the months ahead as the economy bottoms out.

The WisdomTree approach to blending the high dividend factor alongside the value factor helped the WisdomTree US Equity Income UCITS Index (Ticker: WTHYNUHP Index) outperform the S&P 500 Index (Ticker: SPX Index) by 6.3% over the prior quarter1. The WisdomTree US Equity Income UCITS Index focuses on companies with high dividend yields that pay large cash dividends. The strategy weights the constituents based on the cash dividend being paid over the prior year.

As illustrated in the sector attribution the allocation has been positive, contributing to the tracking difference by 3.1%. The overweight in financials, energy and utilities alongside the selection of stocks within information technology, communication services and healthcare benefited performance over the prior quarter.

Source: Factset, WisdomTree from 28 June to 30 August 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

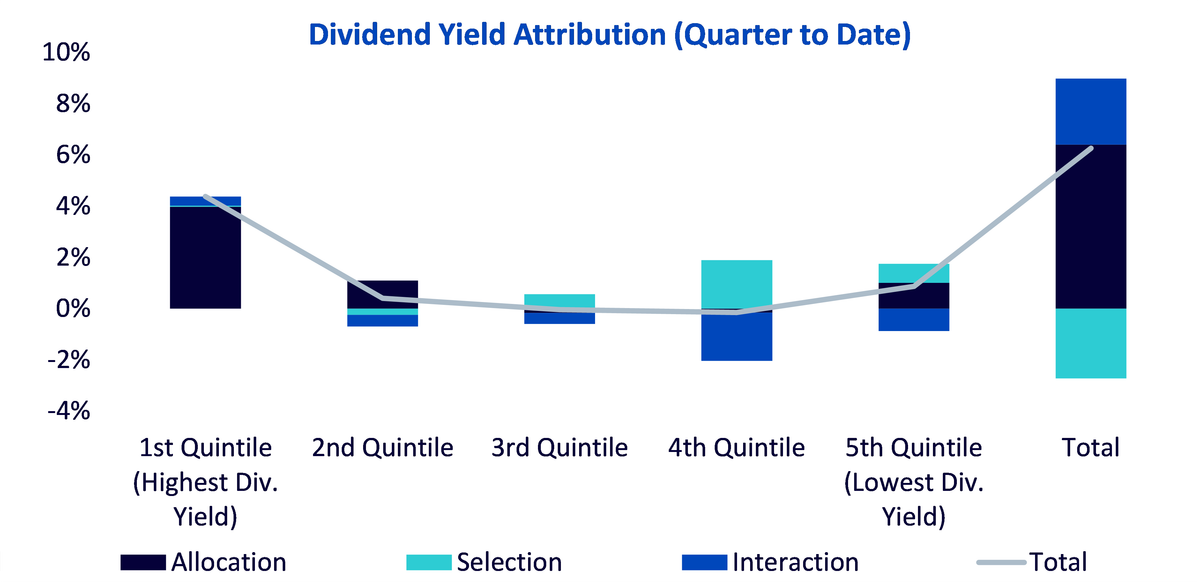

Over the prior quarter, the higher allocation of the WisdomTree US Equity Income UCITS Index to the higher yielding dividend quintiles also contributed to the higher relative performance versus the benchmark.

Source: Factset, WisdomTree from 28 June to 30 August 2024. Historical performance is not an indication of future performance, and any investments may go down in value.

With economic conditions softer, equity valuations stretched, Fed now entering cutting mode, this trend favours the broadening-out call to more undervalued segments of the equity market.

1 FactSet from 28 June 2024 to 30 August 2024.

WisdomTree US High Dividend UCITS ETF

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.