COPA LN

WisdomTree Copper

Published 11 November 2024

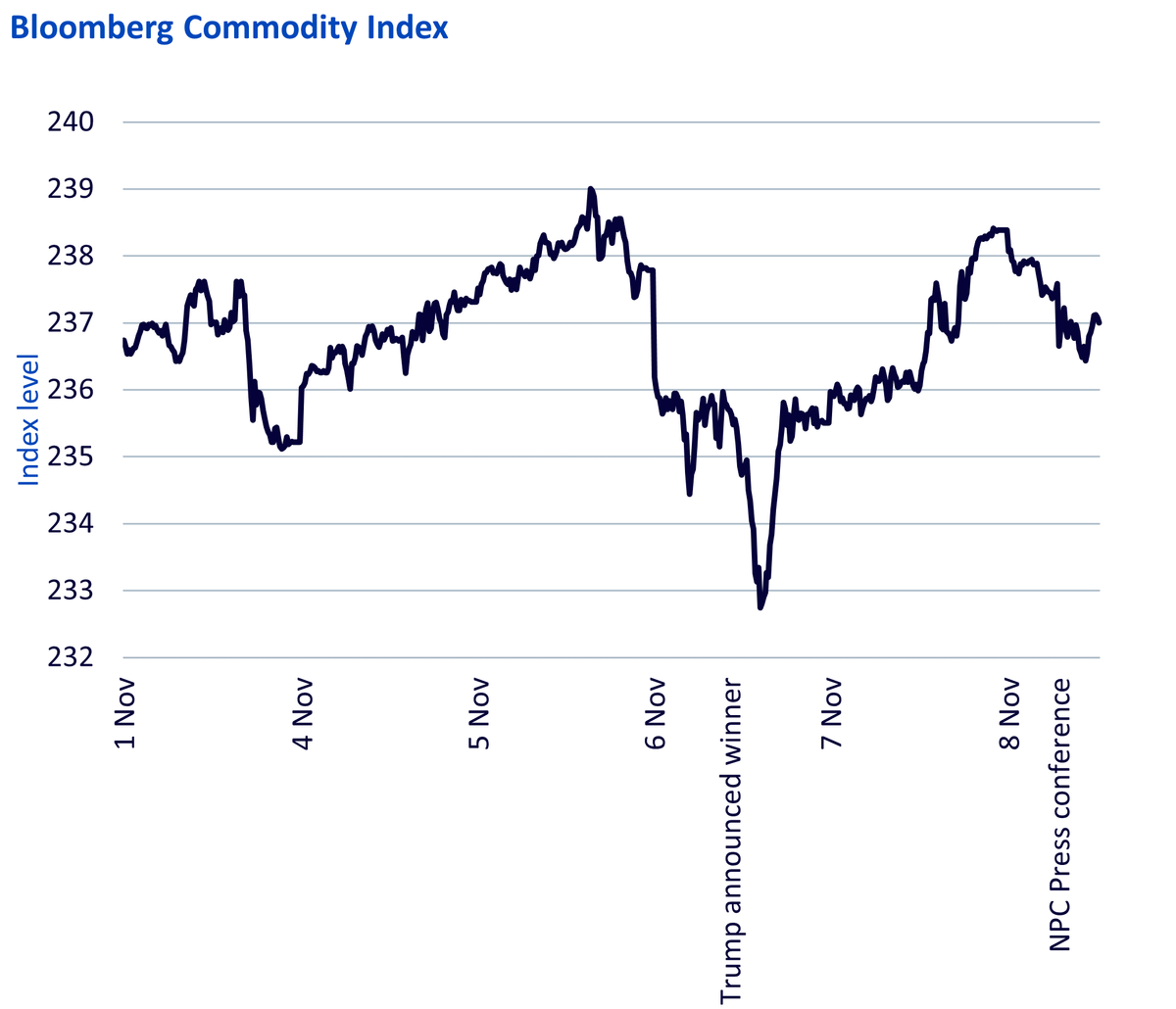

The headlines from last week were negative for commodities:

While commodity prices fell on both announcements, they bounced relatively quickly. Price dips appear to be good entry points, especially if China has left dry powder for a further stimulus in the event of aggressive tariffs.

Source: WisdomTree, Bloomberg. 1am GMT, 1 November – 12 noon GMT, 8 November. President Trump was announced the winner of the US Presidential Election by the Associated Press around 10.30 GMT. National People’s Congress Press conference took place at 8am GMT. Historical performance is not an indication of future performance, and any investments may go down in value.

US President Elect Trump and his running mate, Vance led their campaign platform as trade hawks.

Trump and Vance are also proponents of more domestic oil and gas production.

As we highlight in our Commodity Outlook, lower global trade has historically been negative for commodity prices. The previous Trump Administration-driven trade wars led to a 11% decline in commodity prices in 2018 (based on Bloomberg Commodity Indices).

Trump’s willingness to use Section 301 of the Trade Act of 1974 to expedite trade restrictions was demonstrated in his last presidency, so he may act quickly in delivering his promises.

Global oil markets are already over-supplied and the Organization of Petroleum Exporting Countries (OPEC)’s willingness to sit and watch the US take a larger share of global demand is wearing thin. OPEC has already announced that they will unwind their production restraint that has kept the market in balance over the past two years. On 3 November, they had announced that they will delay the unwind until the end of the year, but it is unclear if they will keep postponing it. Giving up market share has been a painful act, as Saudi Aramco demonstrated last week with a 15% drop in Q3 profits1 from a year ago.

Oil demand weakness stems from China. In 2023 the China accounted for 70% of oil demand growth. This year, it likely only account for 20% of growth2. To be clear, oil demand growth in 2024 is likely to be under 1 million barrels per day, less than half the 2 million barrels per day growth in 20233. We are not expecting a significant pickup in oil demand growth in 2025 either. China’s economy has been weak, and it is electrifying quickly too, reducing its reliance on imported oil.

Whether US producers will expand oil production, even if they have the Federal approvals, is another question. Weak prices may discourage them. But we don’t think OPEC will want to encourage them by boosting prices through aggressive supply tightness.

The Standing Committee of the National People's Congress (NPC) concluded its week-long meeting on 8 November with an announcement of a programme to refinance local government debt. The programme consists of 6 trillion yuan ($839 billion) in new bonds over three years and a further 4 trillion yuan ($558 billion) in previously announced bonds over five years to restructure their finances. In September its central bank, the People’s Bank of China, injected a high dose of monetary stimulus and markets were expecting a fiscal follow-through from the government. Apart from the local government debt refinancing programme the NPC offered no additional announcements of measures to directly stimulate its domestic economy. The package therefore disappointed the markets.

China, as a key target for the new Tump Administration’s trade policy is likely to suffer an economic blow. It is barely healing from the real estate implosion it has suffered over the past two years. China had a choice to get ahead of the tariffs by boosting its domestic economy beforehand. It appears it has chosen to wait and see how damaging the trade restrictions will be before offering its next big move.

We believe the new Administration could begin the process of implementing tariffs shortly after Trump’s inauguration on 20 January 2025. With Republicans controlling the Senate and looking hopeful to have a House of Representatives majority, he may get the backing he needs relatively swiftly.

So, we believe that China will need to deploy its countermeasures relatively soon. Its best option is to stimulate its domestic economy rather than engage in big tit-for-tat trade restrictions. In the last trade war, it restricted US soybean imports. But back in 2017 China sourced a third of its soybean imports from the US4. Now it only imports a fifth from the US5, watering down this threat. China may continue to restrict exports of its own materials that are strategically important, like it has done with gallium, germanium and graphite, but these could be met with further hostility from the US.

If this stimulus is forthcoming, the commodity price dips could open up good entry points in metals.

Oil is less clear-cut given China’s desire to electrify. But a rapid pickup in energy needs won’t be met by electrification alone and hence we think oil could benefit, if OPEC doesn’t use the opportunity to drive up its market share.

WisdomTree has a range of base metal exchange-traded products which could benefit from China using its dry powder in due course. Some examples include:

WisdomTree Copper (COPA) and WisdomTree Aluminium (ALUM) which are fully collateralised, UCITS eligible exchange-traded commodities (ETCs) based on single commodities. WisdomTree Energy Transition Metals (WENT) and WisdomTree Industrial Metals Enhanced (META) provide exposure to baskets of metals. WENT leans into the energy transition and weights each metal by their demand profile in the transition. META uses roll optimisation to reduce drag from markets in contango (upward sloping futures curves).

1 Source: Reuters, Aramco maintains dividend as profits slump

2 Source: International Energy Agency

3 Source: International Energy Agency

4 Source: Bloomberg

5 Source: Bloomberg

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah is a seasoned financial professional with over 24 years of experience in research and investment strategy. As Head of Commodities & Macroeconomic Research at WisdomTree Europe, he leads market analysis and insights across asset classes, with a focus on commodities and exchange-traded products. Previously, he held roles at Moody’s, HSBC Investment Bank, The Pension Protection Fund, and Decision Economics, building expertise in market analysis and strategy. Nitesh earned a master’s degree in International Economics and Finance from Brandeis University and a bachelor's in Economics from the London School of Economics. His insights are frequently featured in financial media, and he is a sought-after speaker at industry events. He also hosts the ‘Commodity Exchange’ podcast, where he discusses trends shaping global markets. Passionate about guiding investors, Nitesh provides actionable insights to help them navigate complex financial landscapes.