Time to seize the European small cap equity opportunity

Published 15 November 2019

Green shoots appearing in European economic data

Macro-economic data in Europe has been weak since the start of 2018. Global macro headwinds linked to the US – China trade wars coupled with domestic structural issues such as tightening of emission regulations are to blame. Sentiment towards European equities is at its weakest point evident from the record outflows of US$8.1Bn from European linked Exchange Traded Funds (ETFs) in the first 10 months of 2019. We believe investors’ loss of confidence is probably overdone. As of late European economic data is starting to stage a turnaround especially when compared to US macro-economic data evident from the chart below.

Figure 1: European economic data starts to improve

Source: WisdomTree, Bloomberg as of 21 October 2019. Historical performance is not an indication of future performance and any investments may go down in value.

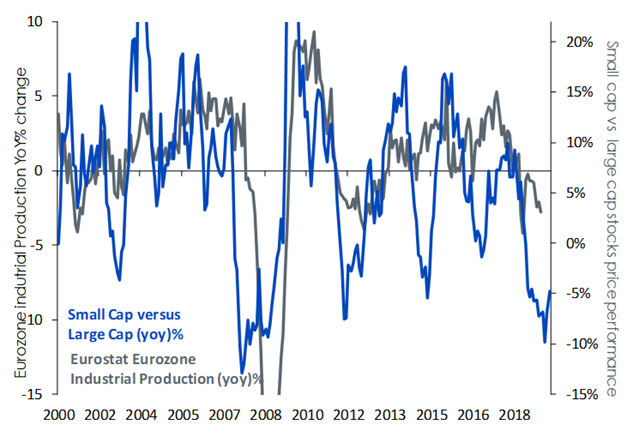

Early lead of small caps price performance could signal further upside in macro data

European small cap stocks have historically tracked the annual change in Eurozone industrial production since 2000. The chart below illustrates the annual change of industrial production in the Eurozone with a 3-month lag plotted against the performance of small versus large cap European stocks. Its worth noting that the industrial sector constitutes the highest sector weight across European Small caps (22%) in comparison to large caps (11%)1. The improvement in price performance of small versus large cap European stocks has historically signalled a rebound in Eurozone industrial production.

Figure 2: Small vs large cap stock performance compared to EU Industrial Production (3-month lag)

Source: WisdomTree, Bloomberg as of 30 September 2019. 1 Historical performance is not an indication of future performance and any investments may go down in value.

Brexit and German Fiscal boost – the next catalysts for European small caps

There are a few catalysts on the horizon that could trigger further upside in Eurozone industrial production, such as (1) improvement in Organisation for Economic Co-operation and Development (OECD) lead indicators (2) additional fiscal easing from Germany (3) easing of Brexit related uncertainty as the odds of a No-deal reduces. While the withdrawal bill passed Parliament “in principle” on 22 October, the government was defeated on the fast-tracking of the implementation. The EU has agreed to postpone the Brexit deadline until 31 January 2020 to allow Boris Johnson more time to persuade members of Parliament to ratify the deal he struck on October 17. The UK will now hold a general election on December 12 in an attempt to break the deadlock. The United Kingdom (UK) is the largest and oldest small cap market in Europe, representing 33% of the small cap universe in Europe. As we receive more clarity on the path UK might follow in its departure from the EU, we believe it will pave the way for further upside across European small cap stocks permitting a greater willingness to invest. The next largest small cap region by market cap is Germany – accounting for 11% of European small cap market share1. Germany, Europe’s largest economy has been hit hardest by trade, the Chinese slowdown and the ongoing US-China trade wars. The fact that Germany has a continent-wide supply chain that accounts for 29% of Eurozone GDP raises the probability of Germany’s slide into recession negatively impacting other Western European economies. So far, the German government announced a €54Bn climate spending package aimed at reaching the 2030 emissions reduction target on 20 September 2019. This is expected to be financed from existing surpluses in the energy and climate fund implying a minor net fiscal net boost of less than 1.6% of GDP. We believe this is far from sufficient to fight the downturn of the German economy. We expect the recent run of weak economic data releases from Germany to eventually persuade the German finance minister Olaf Scholz to unleash a more meaningful round of fiscal stimulus.

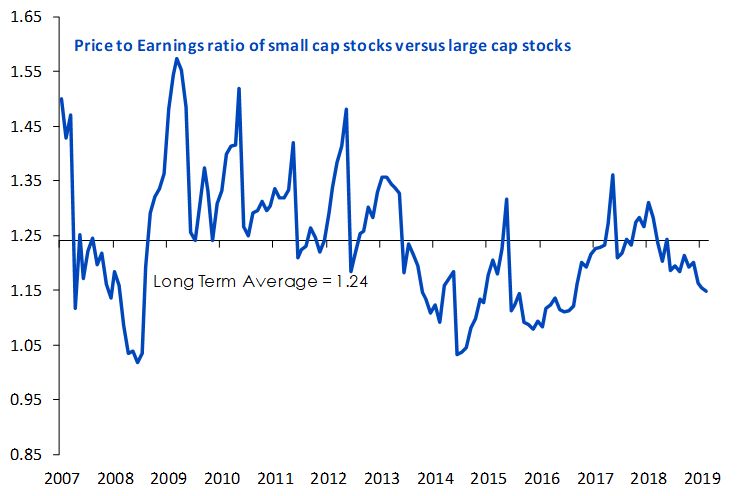

Small cap stocks are not a value trap

European small cap stocks are attractively valued compared to large cap stocks. The Price to Earnings ratio (P/E) of small versus large cap European stocks is trading at a 7% discount compared to its long-term average since 2007. The estimated dividend yields for MSCI Europe Small Cap real time Index at 2.97% is in line with the long-term average since 2007. Leverage for small caps is only slightly higher that of its large cap peers, confirmed by Net Debt to Earnings before interest, tax, depreciation and amortization (EBITDA) at 3.91 vs 3.79x respectively. Owing to the cautious outlook on Europe, there has been an overcrowding in defensive sectors which constitute a larger proportion of large caps compared to small caps.1Free cash flow yields of European small cap stocks also remain healthy at 3.62x.

Figure 3: Small cap vs large cap European stocks are trading at a 7% discount to their long-term average

Source: WisdomTree, Bloomberg as on 30 September 2019. 1 Historical performance is not an indication of future performance and any investments may go down in value.

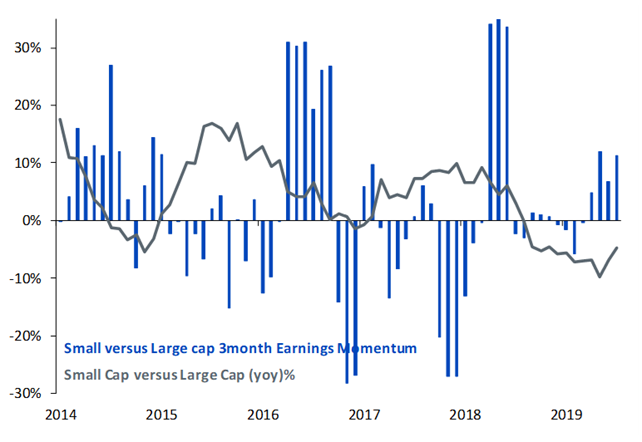

Interestingly relative earnings momentum of small versus large cap European stocks has started to improve over the second half of 2019 and this is clearly being reflected in the outperformance of small versus large cap European stocks, which we believe is still at a nascent stage.

Figure 4: Small cap vs large cap European price performance versus earnings momentum 3 month % change

Source: WisdomTree, Bloomberg as on 30 September 2019. 1 Historical performance is not an indication of future performance and any investments may go down in value.

European small cap stocks are known to be more inefficient than large caps which offers a greater possibility of alpha generation. While sentiment remains weak across Europe, favourable valuations, positive earnings momentum coupled with a slowly improving macro backdrop could provide a timely opportunity to invest in European small cap stocks.

Related blogs

+ Will 2019 be the year of small caps in Europe?

+ It's a small world after all

Related products

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.