Sterling’s Structural vs Euro’s Political Weakness: ‘Brexit’ Opens Up Opportunities for European Dividend Payers

Published 24 June 2016

The people of Britain have voted to leave the EU. What does this mean for the economy and asset markets in the very short to near term?

Our central thesis, as also highlighted in our previous pieces, that the UK’s structurally economic imbalance, as a result of Brexit, is likely to grow larger. Underpinned by a large current account deficit of 7% of GDP, the UK is going to rely even more on the grace of foreign investors to finance a growing trade deficit, unless the pound devaluates. This is likely to occur as, with the UK losing access to the EU single market, its trade in services – of which the UK is a net exporter to the EU – is likely to see barriers to EU trade being erected, even while its trade in goods – of which the UK is a net importer with the EU – will, for the sake of preserving the export earnings advantage enjoyed by EU members with the UK, remain largely untouched.

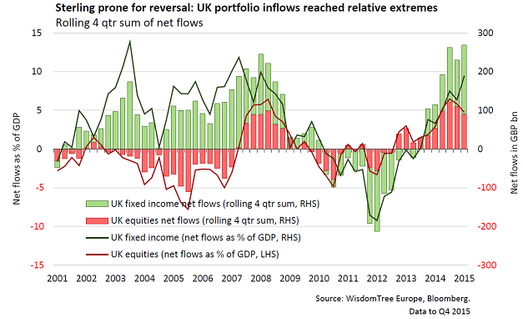

As shown in the chart, portfolio investment flows into UK fixed income and equities in 2015 accumulated to GBP 270 billion, or 14% of the GDP, levels that are extreme compared to years of relative stability during the period post-dotcom bubble and pre-2008 financial crisis. It is unlikely that foreign investors will be as enthusiastic to allocate into gilts and FTSE All-Share companies to that degree, not least because by invoking Article 50 – the only legal way to leave the EU – terms and timetables for new trade agreements are set over a 2-year period by the EU and from which the UK will be excluded. Combined with no reference for an alternative trade model to fall back to, it means undeniable uncertainty for a considerable amount of time and, until the dust settles, would compel asset allocators – at least in the short term – to consider reducing their UK exposure or refrain from asset allocating into the UK altogether.

The pressure point in financial markets will gravitate around the sterling which, while trading more or less range bound since the start, has succumbed to significant intra-day volatility.

+ Hedging UK Mid and Small-Caps - Most prone to such downside risks are smaller-capitalisation stocks whose business models are more focused in the UK or whose trade profile is more concentrated in Europe. Hedging UK mid and small-cap stocks may be warranted, not least given that over 50% of UK trade is with the EU.

+ Hedging major Eurozone broad equity markets and sectors. A dent to confidence will be afflicted to Eurozone’s broad, country and major sector benchmarks. Investors holding bullish positions in broader Eurozone, specific Eurozone sectors, or in German or Italian equities, may want to consider hedging such exposures efficiently, for instance through using leveraged short ETPs.

+ Defensive positioning in UK Large-Cap, High Dividend Yielders - Least prone to unfavourable trade agreements may be UK large-caps. UK’s multinationals with a strong global footprint and lucrative dividend income offer defensive alternatives to the Brexit event which, on net, may benefit from improved exports if the pound weakens. Dividend payers within smaller capitalisation stocks may also provide some quality screen to stocks best able to weather the negative impact on EU trade longer term.

+ Eurozone exporters, hedged - as UK’s exit from the EU could instigate further political instability to potentially lead to euro weakening - which so far has remained relatively immune from Brexit fears - a currency hedged exposure to Eurozone export-tilted large-caps may offer appeal to foreign investors. Ahead of general elections in France (May 2017) and Germany (Sep 2017) where fringe parties’ euro scepticism could fuel souring sentiment on the euro, the currency-hedged overlay may have longer term strategic significance.

Dividend paying exporters, similar to our stance in UK equities, may offer the most defensive equity positioning in Europe.

Fixed Income and Currencies:

+ Gilts: short-term gain, long-term pain. A risk-off sentiment will potentially boost gilts short term, with a strong incentive by the BoE to delay monetary tightening to soften the blow to business confidence and potential weakening economic ramifications. The already record low interest rates in longer dated UK government debt could falling deeper into the ground in the immediate aftermath of the vote. Further out, UK’s large macro imbalance will be laid bare as in anticipation of a volatile and debased currency, sterling’s safe haven status is undermined. With it will be foreign investors’ gilt purchases.

+ Bunds: unassailable haven for safety. An already heavily crowded trade in German bunds may intensify if sentiment in risk assets, particularly within Eurozone banks, sours decisively. A negative yielding Bund may not be a big enough deterrent any longer as almost a quarter of outstanding Eurozone government debt is in sub-zero yield territory anyways. For as long as the ECB’s QE program lasts, Bunds are unlikely to succumb to major downside risks.

+ Euro-dollar: Bearish euro, bullish dollar. The dollar is expected to benefit from bullish sentiment as relative to the euro, US domestic fundamentals are stronger. Banks have stronger balance sheets, the labour market remains resilient and business confidence is proving stable. A relative wide US interest rate differential over the Eurozone means the euro is structurally weak.

Investors sharing this sentiment may consider the following ETPs:

+ WisdomTree Europe Equity UCITS ETF – USD Hedged (HEDJ)

+ WisdomTree Europe Equity UCITS ETF – GBP Hedged (HEDP)

+ Boost Gilts 10Y 3x Leverage Daily ETP (3GIL)

+ Boost FTSE 250 1x Short Daily ETP (1MCS)

+ Boost EURO STOXX 50 3x Short Daily ETP (3EUS)