Japanese exporters outperform as the Yen weakens

Published 15 March 2017

Contributor

Over the past six months the performance of Japanese equities has been driven by the sharp depreciation of the Yen versus the US Dollar. Having languished at levels close to Y100/USD as late as September 2016, the rapid appreciation of the US Dollar in a post-election environment saw the Yen weaken rapidly to over Y118 to the US Dollar and more recently hovering around Y1151.

The main impact of the weaker Yen, which is a core part of the Bank of Japan's policy aims, is to reinvigorate inflation through higher import prices, helping to stimulate demand but additionally to boost exporters and overseas sales and profits. Whilst domestic recovery is a long-term aim, the weaker Yen can have a more meaningful and direct impact on export oriented companies. This has been quick to reveal itself in the outperformance of the export-tilted Japan Hedged Equity Index compared to other Japanese equity benchmarks such as MSCI Japan and the JPX NIkkei 400, all measured with a US Dollar hedge.

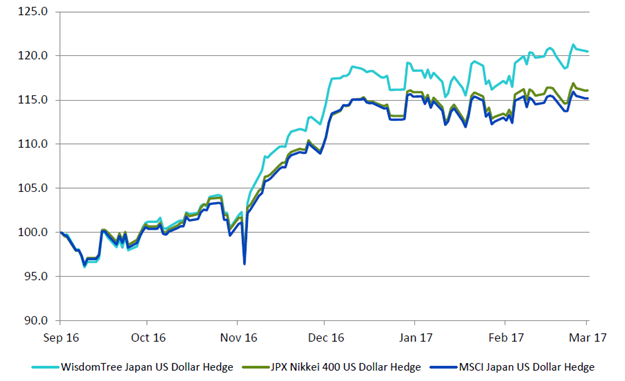

Chart 1: WisdomTree Japan Hedged Equity Index outperforms v JPX Nikkei 400 v MSCI Japan

Source: Bloomberg, WisdomTree

Past performance is not indicative of future results

As the Yen weakened by 12% the WisdomTree Japan Hedged Equity Index rose by over 20%, whilst the other benchmarks rose by 16% and 15% respectively2. Over time it is also evident that the WisdomTree Japan Hedged Equity Index is typically more sensitive to movements in the exchange rate. Chart 2 highlights how WisdomTree's focus on exporters provides for outperformance as the Yen weakens.

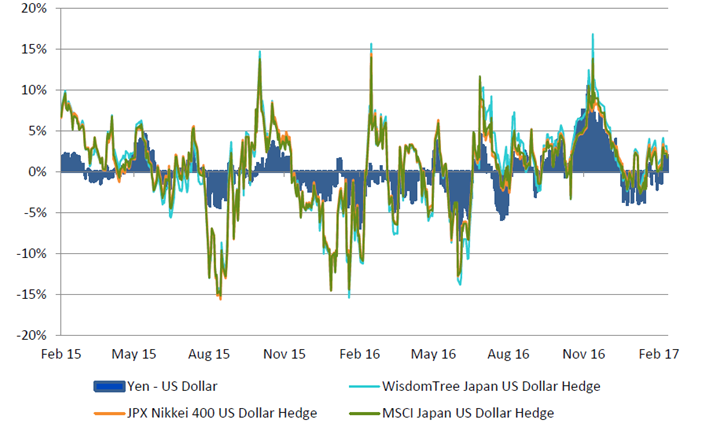

Chart 2: Rolling one month returns: WisdomTree Japan Hedged Equity Index more sensitive to exchange rate

Source: Bloomberg, WisdomTree Past performance is not indicative of future results

There are a number of factors that help drive this performance but the most powerful is the positive impact on profits that comes from changes in the exchange rate. For the Japanese equity market as a whole, as represented by the TOPIX index, there is substantial potential upside to profits should the Yen exchange rate stay at current levels. Compared to previous profit forecasts, with the Yen at around Y115/USD and estimated sales growth of 2%, profits, as measured by earnings per share, would rise by over 30%. Even if the Yen were to strengthen modestly to Y110, with 2% sales growth, profits would be expected to rise by over 23%.

Chart 3: Estimated sales growth v Yen appreciation

Source: Bloomberg

Past performance is not indicative of future results

Japan Hedged Equity Index

WisdomTree's unique export-oriented index for dividend paying stocks, requires companies to have more than 20% of overseas-derived revenue providing a differentiated sector and company composition. This methodology tends to produce an index that has substantial deviations in sector weights compared to benchmarks such as MSCI Japan. These sector over and underweights can deliver significant contributions to performance.

The current largest overweight sector is Consumer Discretionary with a weight close to 25%, a 4.1% overweight, although this has only had a modest impact on performance. Industrials, where the WisdomTree Index is overweight by almost 2.5% has delivered 30% of the outperformance of the past six months. Two areas where the index is substantially underweight are the domestically oriented Telecommunications Services and Real Estate sectors. On a combined basis the WisdomTree index is around 10% points underweight relative to MSCI Japan, and this has delivered 2.4% of outperformance accounting for almost 44% of the alpha generated over the past six months.

The WisdomTree Japan Hedged Equity Index has also outperformed the JPX Nikkei 400 Index, which has a focus on quality factors such as return on equity and operating profits, as well as corporate governance measures.

Japanese equities remain an important single country allocation for the majority of investors with it having the second largest weight in global benchmarks, with close to 9% in the MSCI World Index. Owning Japan based on factors such as the weakening Yen, which is key to the performance of the economy, suggests that investors should consider the WisdomTree Japan Hedged Equity Index due to its focus on export oriented stocks.

Sector comparisons of US Dollar hedge indices

Source: Bloomberg, WisdomTree

Past performance is not indicative of future results

Investors interested in Japan USD hedged exposure may consider the following the ETFs:

+ WisdomTree Japan Equity UCITS ETF USD Hedged (DXJ)

+ WisdomTree Japan Equity UCITS ETF – USD Hedged Acc (DXJA)

+ WisdomTree Japan Equity UCITS ETF - GBP Hedged (DXJP)

+ WisdomTree Japan Equity UCITS ETF - EUR Hedged (DXJF)

+ WisdomTree Japan Equity UCITS ETF - CHF Hedged (DXJD)

About the contributor