WMGT LN

WisdomTree Megatrends UCITS ETF - USD Acc

Published 10 March 2026

Head of Research, WisdomTree Europe.

The debate between top-down and bottom-up investing is as old as asset management. But in multi-thematic portfolios, the trade-offs are unusually stark.

Through years of research, we have developed our own thematic investment philosophy and believe that a top-down framework, starting with theme selection and theme weights, and only then building pure-play, diversified sub-portfolios, is more likely to deliver what investors actually want from a multi thematic strategy:

That philosophy is grounded in a key empirical fact: equity returns are highly asymmetric. In the US, and around the world, a very small minority of stocks has historically accounted for the vast majority of long-term wealth creation1. This ‘winner-takes-all’ effect is key to understanding why multi-thematic portfolios need to be constructed very carefully. To harness thematic growth, the objective is not to avoid every loser, but to ensure you own the winners that will define each theme.

Bottom-up approaches aim to pick companies first and build a portfolio from there. In the thematic space, this usually translates into:

In practice, this often produces four recurring pitfalls:

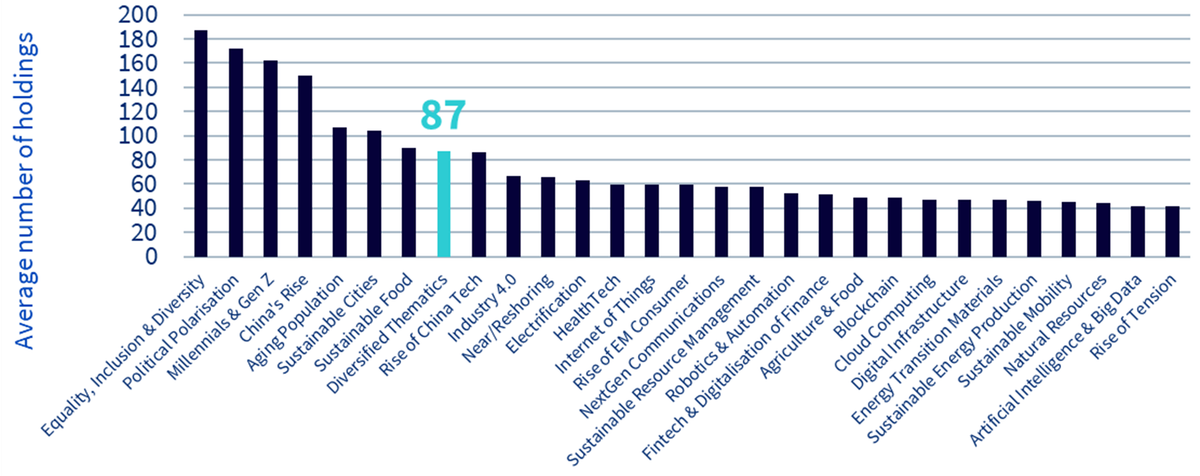

In Europe, diversified thematics (that is, multi-thematic funds) hold around 90 stocks on average (see Figure 1). That number sounds large until you translate it into what it implies: if a manager wants exposure to 10 themes, it means they own around 9 names per theme. Inevitably, the portfolio ends up leaning on the same large all-rounder stocks or being too selective too early in themes, trying to pick winners when the field is still wide open.

Source: WisdomTree, Morningstar as of 31 December 2025. Historical performance is not an indication of future performance and any investments may go down in value.

A bottom-up portfolio often prioritises companies with multiple exposures, as if the goal were to find diversified businesses that touch many trends. In many ways they are built like multi-factor portfolios where the manager aims to find stocks that are good along all the factors. But in thematic investing, the objective is not to find diversified exposure, it is to find meaningful exposure.

When portfolios drift toward generalists (large firms with a little of everything), they often dilute the very exposure investors came for. The result is a portfolio that feels thematic in narrative but ends up like a Nasdaq-100 in disguise.

This is the most underappreciated point. Consider a simple historical example from the internet era. An equal weight basket of the ten biggest internet stocks at end-1998 (which included plenty of failures) still delivered strong long-term results largely because it included the dominant winners.

But when you move to a more concentrated portfolio of only five of those stocks, the outcome becomes highly dependent on whether you owned the ultimate winner. In the analysis, every single five-stock portfolio that included Amazon beat the market; none that beat the market did so without Amazon.

That is the thematic reality: you can choose the right theme and still fail if you miss the winning companies. Bottom-up multi-thematic portfolios, by construction, increase that risk because they pick too few tickets in each.

Multi-thematic portfolios should answer two questions cleanly:

Bottom-up portfolios often struggle on both, because theme exposure emerges as an ex post label rather than a deliberate allocation. The result is limited transparency and weak intentionality, especially when the same mega caps appear repeatedly across different themes.

A good illustration is how certain ‘unavoidable’ tech stocks can dominate thematic holdings. This leads multi thematic strategies to become concentrated tech beta.

A top-down multi-thematic portfolio starts with a different premise: it is easier to have a defensible view on which long-term themes will matter than to predict which single company will dominate each theme.

The idea is to first select the themes and the weights between the themes and then populate each of those sub portfolios with highly relevant stocks. This creates 4 strong benefits for top-down thematic investors:

The top-down lens is not about claiming certainty. It’s about increasing the probability of being positioned in the right places for the next decade, recognising that leadership changes over time and that today’s mega caps are rarely tomorrow’s.

Thematics are a forward-looking way to organise equities: themes link structural drivers like technology, regulation, and social change to portfolio construction. By picking themes first we aim to narrow the field for the stock selection later by focusing on parts of the market that can attract more growth.

A core advantage of multi-thematic investing is inter-theme diversification. Themes are often driven by different catalysts, adoption phases, and idiosyncratic news flows creating potential for lower correlations across themes.

When you build top-down, you can explicitly choose a set of themes that are differentiated (and avoid redundancies) and allocate to those themes to maximise diversification effects.

Once you control the theme weights explicitly, you can:

That’s not market timing for its own sake. It’s acknowledging that themes move in waves and are impacted by catalysts (innovation breakthroughs, regulation, adoption inflections). This is one of the key advantages of a top-down approach as this is not possible to do via bottom-up.

Top-down does not mean buy everything. It means within each selected theme, build an expert-driven, diversified basket of pure-play exposure, wide enough to raise the odds of owning the eventual winners, but disciplined enough to remain investable and differentiated.

This is critical in a winner-takes-all world: investors want enough breadth to avoid the catastrophic outcome, missing the next Amazon, while still concentrating the portfolio’s exposure in the relevant part of the market.

The WisdomTree Megatrends UCITS ETF (WMGT) offers a distinctive top-down approach to allocate across themes. The exchange-traded fund (ETF) uses three successive steps to deliver a portfolio designed to capitalise on shifts in the thematic space:

Overall, the ETF provides exposure to a diversified basket of growing, emerging companies, rather than today’s established tech mega caps.

Thematic investing can be a powerful growth engine in portfolios. But the growth from a theme is not distributed evenly across all stocks in that theme. The winners dominate and so success hinges on two things:

A top-down multi-thematic framework is designed for exactly that: intentional theme exposure, real diversification across different themes, and breadth where it matters, inside each theme, so investors can capture the next Amazon while minimising the potentially disastrous risk of missing it.

1 (Bessembinder, Do Stocks Outperform Treasury Bills?, 2018) and (Bessembinder, Chen, Choi, & Wei, 2019).

WisdomTree Megatrends UCITS ETF - USD Acc

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.