How does the Euro fit in the Currency Puzzle?

Published 9 July 2018

Global Head of Research

Many clients ask us what we think about the Euro and where it may go in 2018. We agree with them that this is such a central question and will have implications for global asset markets around the world.

Unfortunately, it doesn’t make forecasts any easier. Forecasting currencies is very much like putting together a puzzle, at times requiring just as much art as data.

First, where have we been?

To help in developing a framework to think about where the Euro may go in 2018, we first stepped back and looked at the relative performance against the US Dollar for the last ten calendar years, as well as during the first half of 2018.

Figure 1: Performance of the Euro vs US Dollar through the years

Source: Bloomberg. Periods are calendar years, beginning 31 December 2007 to 29 June 2018.

You cannot invest directly within an Index. Historical performance is not an indication of future performance and any investments may go down in value.

+ 2014 and 2015 were the primary years of Euro depreciation (or Dollar strength). At the end of 2015, we saw a level of $1.08, which, for context compares to $1.37 at the start of 2014

+ 2017 was a standout year for Euro appreciation—over the last ten years we did not see anything close to that type of positive move. Global investors were very surprised in 2017 by the Eurozone’s quite strong economic activity, and many were speculating that the European Central Bank (ECB) might have to stop their easing program earlier than planned

We ended the first half of 2018 with the Euro at a level of about $1.17, as of 29 June 2018.

Three Important Pieces of the Currency Puzzle

There are three concepts that we tend to look at when attempting to forecast currencies. It’s important to note that there are many ways to look at these characteristics and that none of them tells us exactly what the Euro will do.

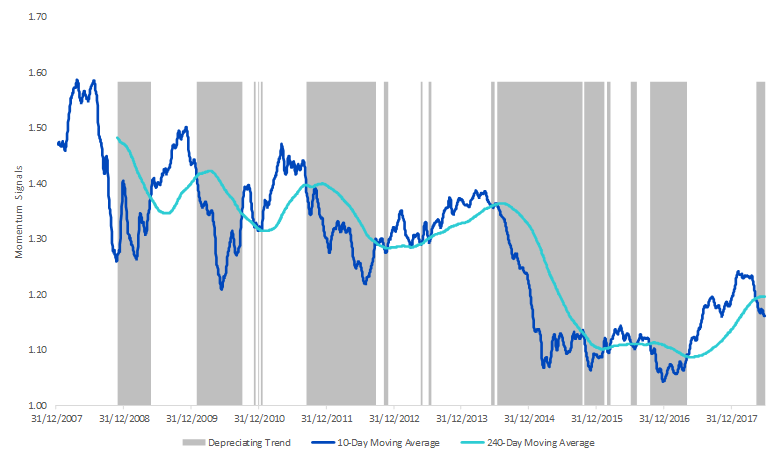

Concept 1: Momentum

While there are many ways to look at momentum, we focus on the 10-day versus the 240-day moving average (MA).

Figure 2: Reading the currency trend

Source: Bloomberg. Data is from 31 December 2007 to 29 June 2018.

You cannot invest in an Index. Historical performance is not an indication of future performance and any investments may go down in value.

+ If the 10-day MA is below the 240-day MA, this means the Euro is in a depreciating trend. These periods are highlighted in grey in Figure 2

+ Conversely, if the 10-day MA is above the 240-day MA, this means the Euro is in an appreciating trend. These periods are not highlighted

Currencies have historically exhibited trending behaviour, and it’s useful to know the trend and think about potential catalysts that could cause it to change in the future. Currently this points more towards further depreciation of the Euro.

Concept 2: Purchasing Power Parity, is the currency cheap or expensive?

Many have heard of the “Big Mac Index” from the Economist—the concept being that a McDonald’s Big Mac, after adjusting for exchange rates, should cost the same around the world. Since this is rarely the case in reality, we can say that currencies are either “too cheap” or “too expensive” relative to each other, thereby inhibiting the similar pricing of substantially the same goods in different global markets.

The current Euro exchange rate (around $1.17 as of 31 May 2018) is very similar to the level that purchasing power parity says it should be. This is a trickier concept—a currency can stay too cheap or too expensive for extended periods. We’d indicate that this signal is basically neutral today.

Concept 3: Shifting Interest Rates

+ 2-Year rates, being on the shorter end, are much more influenced by monetary policy. The US Federal Reserve has been raising rates, whereas the ECB has indicated it will not raise rates for a period of about 12 months. The US 2-Year has extended its yield advantage over the German 2-Year from about 2.5% to 3.2% thus far in 2018.

+ 10-Year rates, being on the longer end, are more influenced by inflation and growth expectations. In 2018, the US 10-Year has extended its yield advantage over the German 10-Year from about 2% to about 2.5% thus far in 2018.

Figure 3: Comparison of 2-Year and 10-Year interest rates between US and Germany

Source: Bloomberg. Periods is from 29 December 2017 to 29 June 2018.

You cannot invest directly within an Index. Historical performance is not an indication of future performance and any investments may go down in value.

In theory, global investors appreciate higher yields over lower yields, so this would point to the potential for Dollar appreciation (Euro weakness) going forward.

Conclusion: 2-0-1 for Euro Depreciation

Therefore, what we see currently are two concepts (Momentum & Interest Rates) pointing toward Euro depreciation, no concepts pointing toward Euro strength, and one concept (PPP) being neutral.

We see the Euro more likely to depreciate in the second half of 20181.

Related products

+ WisdomTree Europe Equity UCITS ETF - USD Hedged (HEDJ)

+ Boost Long USD Short EUR 4x Daily ETP (4USE)

+ Boost Long USD Short EUR 5x Daily ETP (5USE)

+ Boost Short USD Long EUR 4x Daily ETP (4EUS)

+ Boost Short USD Long EUR 5x Daily ETP (5EUS)

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.