Extreme Performance? Try an Equal-Weighted Rebalance

Published 2 September 2020

Global Head of Research

Cloud computing has enjoyed a remarkable amount of attention in 2020. One consequence of the Covid-19 pandemic has been that many companies have decided to accelerate their respective paces of digital transition. The benefits of ‘cloud’ vs. ‘on-premises’ have never been more clear, as many firms are seeing their employees require degrees of flexibility, security and access that had not been executed previously.

The result: Many companies have exhibited EXTREME performance.

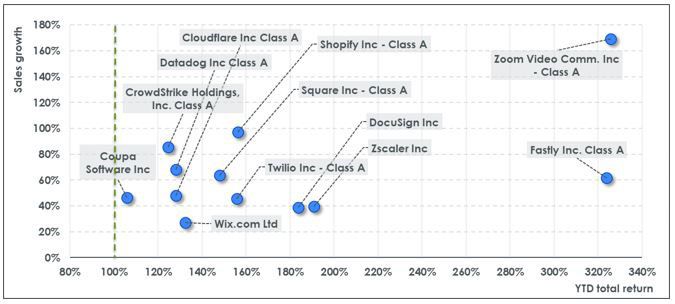

In Figure 1, we showcase the ‘Triple-Digit’ Club.

- Both Fastly and Zoom have delivered returns not only in excess of 100% or 200%, but rather in excess of 300%. On 31 December 2019, Zoom had a market capitalisation of $18.81 billion, whereas Fastly had a market capitalisation of $1.88 billion. As of 24 August 2020, these companies had market capitalisations of $79.6 billion and 8.9 billion respectively1.

- Internet Security & Efficiency: During the Covid-19 Pandemic, a larger number of people have been spending a greater fraction of their lives on the internet. Companies like Fastly, Zscaler, Datadog, Cloudflare and CrowdStrike all perform a variety of functions to make this online experience both more efficient in content delivery and more secure.

- eCommerce: The shift from physical retail to eCommerce was already underway, but it’s possible that the Covid-19 Pandemic has contributed to its acceleration. Shopify has been a standout company in this space, but Wix.com has recently added eCommerce functionality to some of its packages and Square is also well positioned to facilitate digital transactions.

- Digital Communications & Capability: Zoom has been the blockbuster example of a company able to provide video conferencing and webinar solutions at a time when the world greatly needed it. However, few would dispute the convenience offered by a company like DocuSign (especially without access to a printer).

Figure 1: Introducing the ‘Triple-Digit’ Club in Cloud Computing

Balancing the Seesaw: Next few Months vs. Next few Years

After companies have already delivered better than 100% returns in periods less than one-year, it is natural to expect somewhat of a ‘cooling off.’ No one can ever say exactly when it will happen, but history has shown that stratospheric returns frequently can be followed by underperformance and a dying down of the former euphoria.

Some investors may be positioning for the growth of the cloud computing megatrend—something we believe will play out over the course of the 2020’s. We see many clients very bullish on this theme over the course of the next five or ten years, while at the same time recognising that ‘uncertainty’ could characterise the performance over the remaining months of 2020.

Possible Tactic: An Equal-Weighted Rebalance

While equity indices are broadly termed ‘passive’ investments, it’s important to recognise there is a difference between a classical market capitalisation-weighted benchmark and almost any other approach. Equal-weighted indices were amongst the first to be widely considered after market capitalisation-weighted benchmarks had taken hold of the consciousness of the investing public.

- With Market Capitalisation Weighting: Companies start off weighted relative to their proportional market capitalisation size. Over time, if they grow their market cap relative to other constituents, they will see their weights rise; similarly, if they shrink their market cap relative to other constituents, they will see their weights fall. The mechanism by which market cap changes is the share price, so a rising market cap relative to other constituents is a signal of share price outperformance relative to these constituents.

- With Equal Weighting: All constituent companies are always going to be weighted equally at the next rebalance. Outperformers may have grown in weight—they will be trimmed. Underperformers may have shrunk in weight—they will see their weight adjusted upwards. Additionally, a company with a $1 trillion market cap will be treated to the same starting weight as a company with a $1 billion market cap (1000x smaller).

How ‘Passive’ was an Equal-Weighted Index for Cloud Computing Companies in 2020?

The BVP Nasdaq Emerging Cloud Index is, in fact, an equal-weighted index that is rebalanced twice per year—specifically in February and in August. The August 2020 rebalancing process occurred after the close on 21 August 2020. Figure 2 Indicates:

- Companies that saw their weights reduced at this rebalance had delivered average performance of 128% from 31 December 2019 to 21 August 2020. Fastly saw its weight reduced by more than 3.1%, whereas Zoom saw its weight reduced by more than 2.0%.

- The full list of companies shown in Figure 1, our ‘Triple Digit Club’, did see weight reduced. Fastly and Zoom had the largest weight reductions, whereas CrowdStrike had the smallest weight reduction of about 0.64%.

- Companies that saw additional weight as a result of the equal-weighted rebalancing process had delivered average performance of 23.0% from 31 December 2019 to 21 August 2020. Four of these companies delivered negative returns during this period. The company, J2 Global, also delivered a negative return, but it was removed from the BVP Nasdaq Emerging Cloud Index due to a declining share of its business coming from cloud-focused activities.

Figure 2: Equal-Weighting Trimmed Index Weight to Top Performers

Source: Bloomberg, Nasdaq. Company returns (YTD total return) presented on total return basis for the period from 31 December 2019 to 24 August 2020. Companies are constituents of the BVP Nasdaq Emerging Cloud Index. Weights are calculated based on closing prices as of 21 August 2020 and 24 August 2020. Grey markers represent index constituents as of 24 August 2020 (post-rebalance); blue markers - as of 21 August 2020 (pre-rebalance). Lime markers represent index constituents added and crimson markers index constituents removed after the rebalance.

Historical performance is not an indication of future performance and any investments may go down in value.

Meritocracy Determines where we go from Here

We honestly don’t know if some of these companies can deliver as strong or stronger returns from September to December of 2020. Trends in year-over-year sales growth, as of 30 June, for the companies that have reported as of this writing, has still been positive. Still, once 100% returns are achieved within a single year, it can be difficult to surprise markets enough to continue to double from there. What we do know is if we see Fastly or Zoom or another company heading into the top 10 and gathering a 3% or 4% weight—like we saw over the past six months—it would have earned it through strong outperformance over the other constituents.

1 Bloomberg, with data as of specified dates.

+ A Unique Freemium Cloud Model

+ How Early Are We in the Shift to the Cloud?

Related products

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.