What's Hot: Do commodities offer an avenue to hedge against Russia-NATO tensions?

Published 4 February 2022

The intensifying standoff over Ukraine has led to heightened geopolitical tensions in 2022. Russia has always considered Ukraine to be under its sphere of influence, but as Ukraine has looked towards the west, the dynamic has become less acceptable for Russia. Tensions continue to run high as little progress has been made on the negotiations between Russia and the West. On 31st January, the US formally rejected Russia's demand that Ukraine be barred from North Atlantic Treaty Organisation (NATO). Russia continues to move medical units to support its troops at the Ukrainian border, which the Pentagon has assessed as a Cold War throwback. While uncertainty remains over the outcome, Russia-NATO tensions over Ukraine could trigger further turbulence in already imbalanced energy markets and be decisive for the geopolitics of Europe's defence architecture. Wheat stands to benefit as Russia and Ukraine account for a large share of its exports on global markets. It also has the potential to lend a tailwind to metals such as nickel, aluminium, palladium, and gold.

Rising uncertainty keeps energy markets on tenterhooks

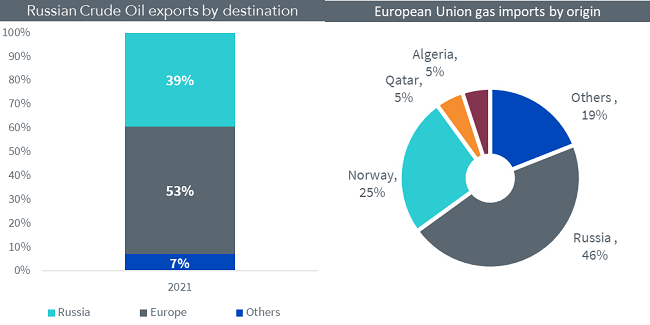

Oil prices are currently trading at a nine-year high buoyed by strong demand and the inability of the Organisation of Petroleum Exporting Countries (OPEC+) to implement its announced production hikes at 400,000 barrels per day. In accordance with its commitments with OPEC+, Russia is currently producing below capacity. Russia is the second-largest oil producer and crude oil exporter in the world. If the West were to impose sanctions on Russia, it would impact a large share of these exports, thereby likely pushing the global oil market further into a deficit and fuelling the oil price rally. Europe is the most reliant on gas supplies from Russia, accounting for nearly 46% of Russia's gas exports1. Supply on the European gas markets is tight, giving Russia leverage to force the West to make political concessions. Europe's ability to cope with an interruption to supply is reduced by the fact that European gas storage stocks in January were at their lowest level since 2011. In a scenario of military conflict between Russia and Ukraine and a potential retaliatory halting of gas exports to Europe, European gas prices would rise significantly higher.

Figure 1: Russian Oil Exports and European Union Gas Imports

Source: BP Statistical Review 2021, Gazprom, Eurostat, WisdomTree as of 31st December 2021

Geopolitical tensions lend a tailwind to wheat prices

Wheat had a strong year in 2021. A tighter supply situation on the wheat market helped prices rise to a nine-year high in November last year. However, since then, the supply situation has been revised upwards due to better crops in Argentina and Australia, leading to a reduction in the supply deficit to 2mn tons from 5mn tons2. Russia (20%) and Ukraine (8.2%) are amongst the eight largest wheat exporters globally3. The U.S. Department of Agriculture (“USDA”) revised its forecast for wheat exports lower due to Russia's higher exports tax and an export quota of 8mn tons that was introduced for the period 15th February – 30th June 2022. According to the Ukrainian Ministry of Agriculture, there are another 8mn tons of wheat available for exports. Based on the above estimates, we expect a total of up to 16mn tons of wheat from Russia and Ukraine could be affected by a possible escalation of the conflict, which would be difficult to substitute from other major suppliers. In the absence of a conflict, we would expect wheat prices to ease in 2022 on the back of a looser supply situation.

Russia's dominance in the metals market

Russia is the world's largest palladium producer. Palladium's performance in 2021 was weak owing to demand destruction from weak automobile production globally. However, the outlook for palladium demand and, in turn, prices in 2022 looks promising as semiconductor supply issues restraining vehicle production in 2021 ease. Given the fact that Russia is a sizeable producer of palladium, an intensification in the Ukraine conflict could further tighten the global palladium market further. Russia is also an important producer of aluminium, nickel, copper, and platinum. However, given the more diversified sources of supply for these metals, we would expect less of an impact in the event of a conflict erupting. Gold has historically performed well in times of financial stress and could stand to benefit the most if the conflict were to escalate.

1 Gazprom, Eurostat

2 International Grains Council as of January 2022

3 United States Department of Agriculture (USDA) Agriculture Projections to 2030

Categories

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.