Diversified and Enhanced Commodities Investing Part II: Broad and Enhanced Commodity Strategy improves Multi-Asset Portfolios Diversification

Published 1 June 2016

In Part I of ‘Diversified And Enhanced Commodities Investing’, we described the unique driving forces attributed to distinct price trends and the high volatility of single commodities. However, when these single commodities are combined to form a broad commodities basket, .

Part II makes the case for the diversification potential of a broad basket of single commodities when combined with conventional multi-asset portfolios comprising equities, bonds and cash. A broad commodities exposure may reduce portfolio risk and – through an enhanced/optimised roll methodology – increase portfolio returns volatility is markedly reduced.

Single commodities are uncorrelated, as are broader commodity baskets to equities and bonds

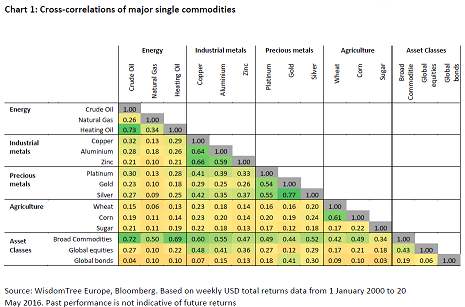

Chart 1 shows a correlation matrix of major single commodities in energy, agriculture, precious and industrial metals. Based on weekly returns of front-month futures, it is evident that single commodities are effectively uncorrelated to each other, with most correlation coefficient readings between different commodity sectors hovering around 0.2[1].

For instance, the lowest correlation reading in the table is between wheat and natural gas futures, which has a correlation of near zero. Natural gas and copper’s correlation is around 0.13 with natural gas and gold at 0.11. Copper and gold correlation is 0.29; copper and corn at around 0.2. Gold and corn have a 0.19 correlation. While correlations are higher within commodity sectors, readings of 0.6 to 0.7 imply that combining heating oil with crude oil; zinc with copper; silver with gold; or wheat with corn will still reduce volatility.

Chart 1 also shows how low correlations are for broad commodity baskets compared to baskets of global equities and global bonds, with readings of 0.43 and 0.19, respectively. Hence, if a broad basket of commodities can work to dampen large price movements of single commodities because of low correlations, it can also work to reduce the volatility of conventional mixed equity and bond portfolios.

[1]Correlations can range between 1 and -1. Correlations describe the extent to which the movement of two asset prices are related. The lower the correlation, the least the prices of two assets co-move, or move in the same direction.

Tilting Portfolio Returns Through Enhanced/Optimised Roll of Commodities

[2]Aside from spot price return and roll yield, there is also collateral yield, or the interest earned on posted collateral when buying commodity futures. While collateral yield was a significant contributor to the total return performance of commodities in the high inflation period of the 80s and 90s, the low inflation and near zero, if not negative interest rate environment in recent years was made the collateral yield relatively insignificant.

[3]Futures markets are in backwardation when near month futures prices are higher than futures prices further out. In such conditions where futures curves are downward sloping, rolling comes as an advantage to investors.

The cost of carry can be significant especially when commodities are held strategically over long investment periods. Consider crude, after it spectacularly crashed in the Summer and Autumn of 2008 – il markets have since been effectively in contango[1]. From 2009 to end of April 2016, the return on WTI crude oil spot prices was 3%, but investors rolling front month futures would have lost 62% in the same period. Similarly this year, amidst sharply rebounding crude oil prices rising 24%, investors only received 5%.

Investors seeking exposure to commodities in both multi-asset portfolios and as stand-alone asset classes should consider enhanced/optimised roll strategies that help minimise the cost impact of contango markets and the erosion to their total returns over time.

The enhanced/optimised roll strategy exploits the concave upward sloping future curves which, due to seasonal factors’ significant impact on supply and demand expectations, are prevalent in energy and agriculture commodities. Broadly speaking, when crude oil markets are in contango, an enhanced/optimised roll strategy would mean staying invested in WTI futures contracts further out where the slope of the futures curve is shallower (and where time and rolling erodes futures prices less). As such, investors suffer from less carry than in the case of a conventional roll strategy where investors stay invested in futures contracts nearer to expiry. This is precisely where the steeper slope of the futures curve suggests time and where rolling actually erodes futures prices faster and harder.

When considering Bloomberg’s broad commodities index (ticker BCOMTR), and its enhanced/optimised roll version (ticker EBCIWTT), the outperformance of the latter compared to the former since inception, has been considerable and fairly consistent. The calendar year returns for both benchmarks since 2004 show that returns for EBCIWTT have been on average 7.5% higher than for BCOMTR, with outperformance in every calendar year bar in 2013, when EBCIWTT underperformed BCOMTR by a mere 0.6%.

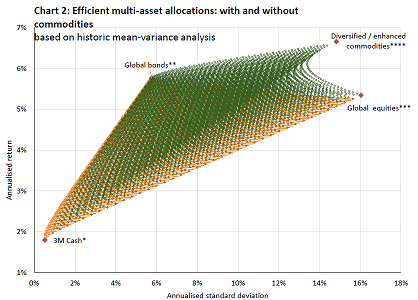

Combined with an enhanced/optimised roll strategy a diversified commodities basket may improve the performance profile of multi-asset portfolios. Chart 2 shows how, using Markowitz’s mean-variance portfolio theory, exposure to such a commodity strategy can improve the performance profile of a multi-asset portfolio comprising global equities, global bonds and cash[2]. Represented by the orange dots, allocations into global equities, global bonds and cash would have provided investors lower returns for given level of risks than if they supplemented this portfolio with some allocation into a broad diversified enhanced commodities strategy, represented here by EBCIWTT. As shown by the green dots, for a given level of risk, a higher portfolio return was achieved through some allocation into the diversified, enhanced commodities strategy.

Source: WisdomTree Europe, Bloomberg. Data based on monthly total returns in USD since May 2001, which is the inception date of the diversified enhanced commodity strategy. Past performance is not indicative of future returns. * 3M US Libor, ** JP Morgan Global Aggregate, *** MSCI All Countries World, **** Bloomberg Optimised Roll Commodities

[1]Assuming the nearer months contracts for WTI crude oil, i.e. between the front and 2nd month futures contract

[2] Proxies for global equities, global bonds and cash are the total returns of MSCI AC World, JP Morgan Global Aggregate and US 3M Libor, respectively

Why consider commodities again?

Bond markets look increasingly dislocated and prone to downside risk as the zero/subzero interest rate environment continues to spread and investors are forced to chase yield in the junk segments. The equity market recovery since 2009 and the unabated rally since 2015 now looks tired, underpinned in part by slowing growth prospects of tech stocks and the deep balance sheet restructuring of bank stocks. Against this backdrop are this year’s rebounding commodities which, against the price trend of the last five years still look depressed. In the face of slowing but stabilising EM growth, a diversified commodities exposure employing an enhanced/optimised roll strategy may likely complement multi-asset portfolios by giving the investors better diversification and improved returns.

Investors sharing this sentiment may consider the following UCITS ETFs.