BTCW LN

WisdomTree Physical Bitcoin

Published 1 December 2025

Director, Digital Assets Research

UK investors now have exchange-listed access to bitcoin and Ether through physically backed crypto exchange traded products (ETPs), yet many still approach the market with assumptions shaped by an entirely different era of products. Outdated comparisons with early unsecured exchange traded notes (ETNs), confusion over exchange traded fund (ETF) vs ETN labelling, and persistent myths around custody and issuer risk continue to distort how crypto ETPs are evaluated.

This gap in understanding matters. When investors focus on the wrong risks, they overlook the factors that truly determine safety and performance: how the product is structured, where the assets sit, who controls the keys, and what protections apply if something goes wrong.

In reality, today’s physically backed crypto ETPs are straightforward in purpose but sophisticated in design. The mechanics under the hood, not the marketing label, define the quality of the exposure.

Below are four misconceptions that most commonly mislead UK investors, and the facts that matter far more when assessing the strength of a crypto ETP.

This belief refuses to die, but it misses the regulatory logic that drives the labels. The names differ because:

Different words. Same economic exposure as both structures aim to track the price of the digital asset.

The real distinctions investors should care about:

The ETF/ETN divide is regulatory, not hierarchical. The questions that determine risk are about physical backing, collateral segregation and what happens if the issuer fails – not the label on the wrapper.

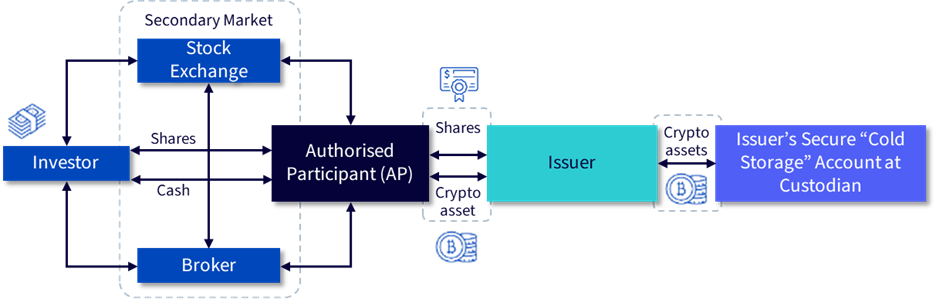

This myth lingers from the early era of unsecured ETNs, where investors were exposed to issuer credit risk. Today physically backed ETPs use a different architecture entirely.

These products are built to reflect exposure to real digital assets, not promises.

Operational risk does not disappear, and crypto custody introduces risks unique to digital assets, from key-management failures to network-level events such as forks, and while transparency helps, these operational risks are inherent to the asset class rather than a function of the wrapper.

This is a historical fear because early ETNs were unsecured credit. Nowadays physically backed crypto ETNs use bankruptcy-remote special purpose vehicles (SPVs) that are designed to shield investors from issuer failure.

But there are limits:

The SPV structure removes one category of risk, not the entire stack.

True for bitcoin as there are no dividends, coupons or cashflows. But proof‑of‑stake (PoS) networks change the equation. By participating in network security, Ethereum ETPs can generate staking rewards that flow back to investors.

However, it is important to note that rewards vary and are not guaranteed, and that staking introduces new risks such as slashing and / or illiquidity. Importantly, investors should assess the net return they are likely to receive – the expected staking reward after accounting for the ETP’s management expense ratio.

Stepping back, the message for UK investors is straightforward: physically backed crypto ETPs simplify access without altering the economic reality of owning digital assets. They:

Myth | Reality | Why it matters |

|---|---|---|

1. ETNs are inferior to ETFs. | Label is regulatory. | Focus on structure, not naming. |

2. Crypto ETPs are unbacked. | Physically backed ETPs hold crypto with institutional quality custodians. | Investors need to avoid outdated credit-ETN confusion. |

3. Issuer bankruptcy wipes investors out. | SPVs ring-fence assets. | Reduces credit risk meaningfully. |

4. No income potential. | ETH and other PoS assets can generate rewards for investors. | Enhances total return profile. |

Source: WisdomTree. November 2025.

However, it’s important to remember that crypto ETPs won’t remove the inherent volatility of the asset class. The role of crypto ETPs is to make crypto exposure simpler and more accessible – not to change the nature of the market itself. Understanding that distinction helps investors use these products with confidence and clarity.

For more insights and educational resources on crypto ETPs, visit our Crypto ETP centre.

1UCITS = Undertakings for Collective Investment in Transferable Securities.

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).