WCOA LN

WisdomTree Enhanced Commodity UCITS ETF USD Acc

Published 6 May 2026

Associate Director, Quantitative Research at WisdomTree in Europe

Inflows into UCITS commodity products were robust in 2025, with approximately €1.7 billion entering the asset class. Year-to-date, however, flows have almost reached €2 billion as of 16/04/2026, highlighting increased investor interest.

However, despite this notable growth, investor behaviour toward commodities remains largely tactical. Investors tend to turn to the asset class only after the move has already happened, effectively locking the stable door after the horse has bolted. Buffett’s long-standing stigma of commodities as an “unproductive” asset class may still be echoing in the background. The asset class remains significantly underinvested in both institutional and retail portfolios. Recent developments have, in turn, reinforced the relevance of commodities both tactically and strategically.

Broad commodities, as measured by the Bloomberg Commodity Total Return Index (BCOM), delivered a 22.9% year-to-date return, while WisdomTree’s Enhanced Commodity UCITS ETF (WCOA) outperformed over the period, increasing 27.4%1. The first quarter of 2026 provided a powerful reminder of why commodities remain uniquely sensitive to geopolitics, supply disruptions and curve dynamics, and why active positioning can matter materially in such an environment.

The opening months of 2026 felt like an accelerated course in commodity investing. Over the brief period of three months, we witnessed the following:

That backdrop made Q1 the first meaningful stress test for the new WisdomTree Enhanced Commodity UCITS ETF (WCOA) framework. Effective 18 September 2025, the exchange-traded fund’s (ETF’s) underlying index transitioned to the WisdomTree Enhanced Commodity Total Return Index (WTENCMT). The new approach still begins with the Bloomberg Commodity Index (BCOM) universe and its weights but introduces daily factor-driven tilts. These are evenly split across backwardation, slope momentum and price momentum, while remaining within UCITS constraints relative to BCOM. Contract selection is also more dynamic: non-seasonal commodities use roll-yield optimisation, seasonal markets follow seasonal contract rules, and precious metals remain positioned in the front contract.

Let’s take a closer look at how the new WisdomTree Enhanced Commodity UCITS ETF performed during its first real test in Q1.

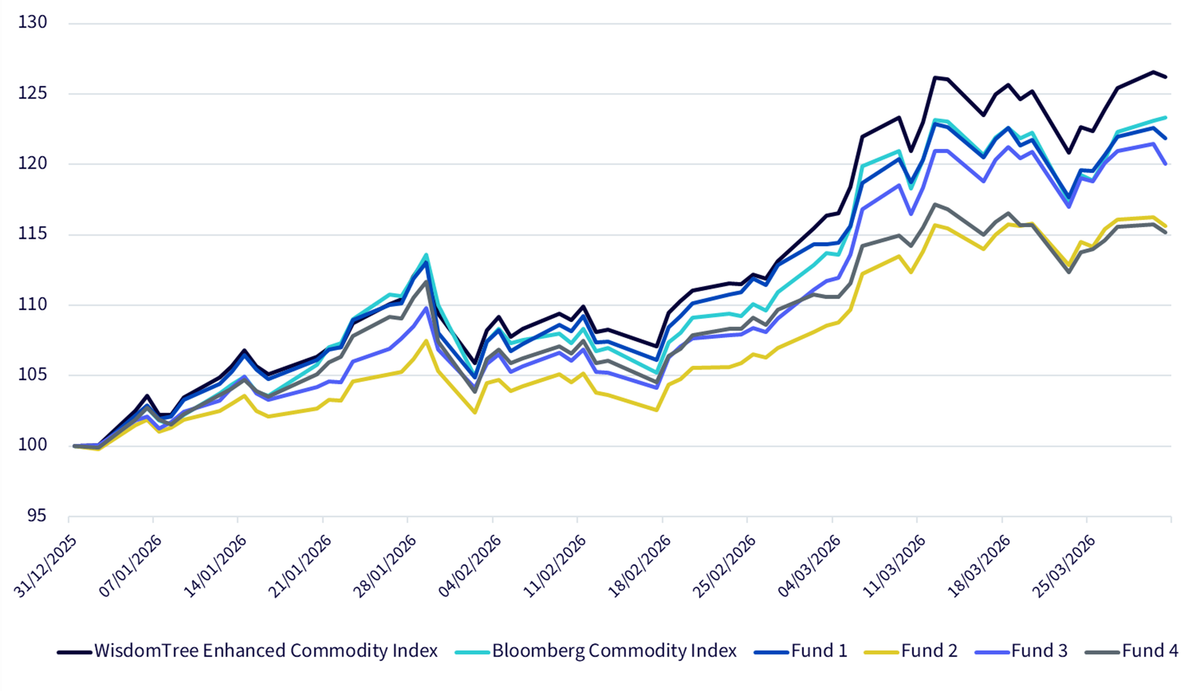

Over the first three months of 2026, the WisdomTree Enhanced Commodity UCITS ETF Index delivered an excess return of +26.21%3, outperforming the Bloomberg Commodity Total Return Index by +2.91%. This outperformance is notable given a market backdrop that was not particularly favourable for enhanced strategies4. The chart below compares Q1 excess return performance across the Bloomberg Commodity Index, the WisdomTree Enhanced Commodity UCITS ETF Index (WTENCM) and the indices of the four largest enhanced commodity UCITS ETFs.

The WisdomTree Enhanced Commodity UCITS ETF, like other enhanced strategies, relies on two main levers to outperform its benchmark: contract selection and commodity selection (i.e. overweights and underweights relative to the benchmark). In strongly rising markets, the first lever becomes less effective, as performance is typically concentrated in the front contract, where the Bloomberg Commodity Index is also positioned. As a result, outperformance in such environments depends primarily on the effectiveness of commodity selection.

Source: WisdomTree, Bloomberg. Data from 31/12/2025 to 31/03/2026. Calculations are based on excess return indices. Comparisons are shown for illustrative purposes only. Funds 1, 2, 3 and 4 are the four largest enhanced commodity UCITS ETFs. The strategy differs from these indices in terms of composition, sector exposure and risk profile. Historical performance is not an indication of future performance and any investments may go down in value.

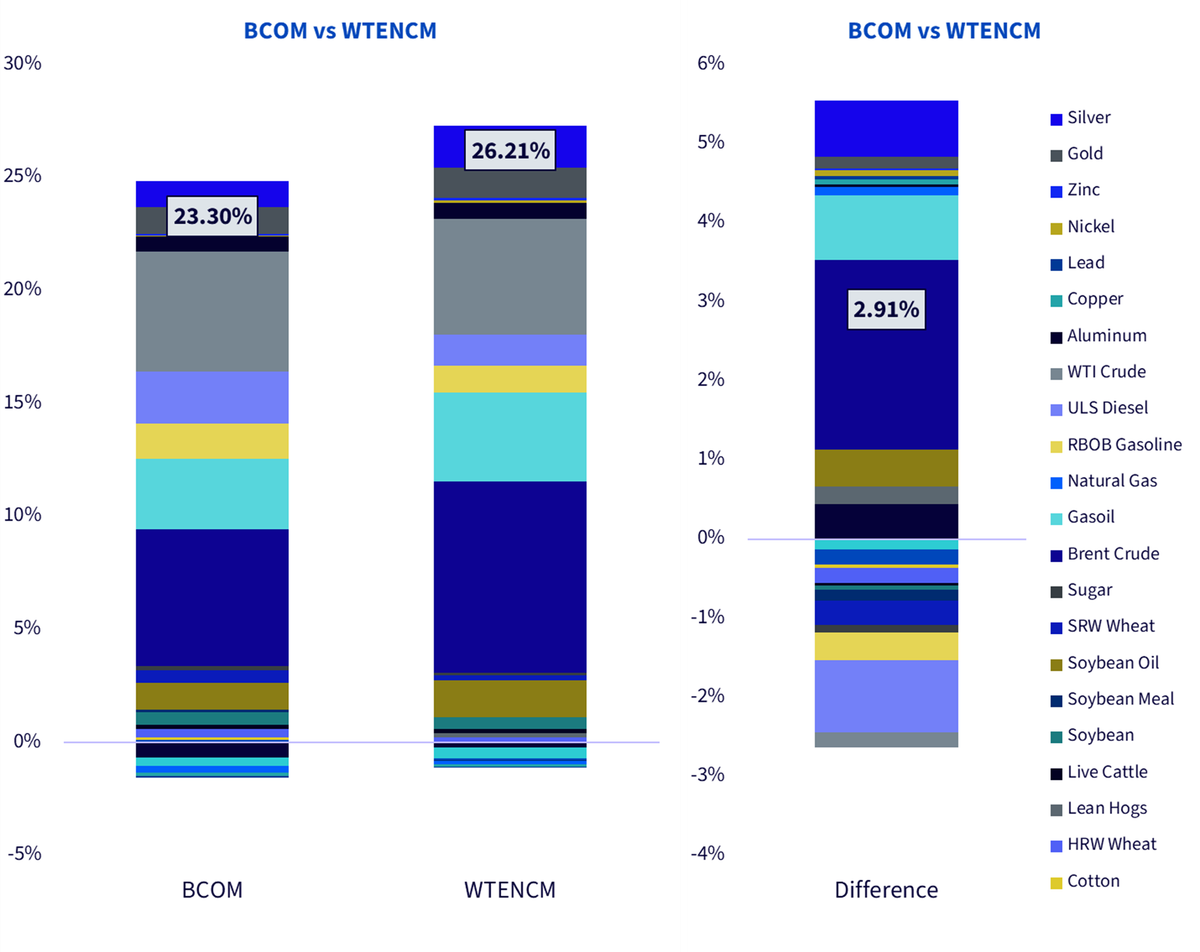

The image below shows the performance contribution by commodity for the Bloomberg Commodity Total Return Index and the WisdomTree Enhanced Commodity Index. Unsurprisingly, most of the quarter-to-date performance comes from the oil-related commodities. In relative terms, the largest positive contributions were given from Brent and Gasoil, while ULS Diesel and Gasoline have been the largest detractors.

Source: WisdomTree, Bloomberg. Data from 31/12/2025 to 31/03/2026. Historical performance is not an indication of future performance and any investments may go down in value.

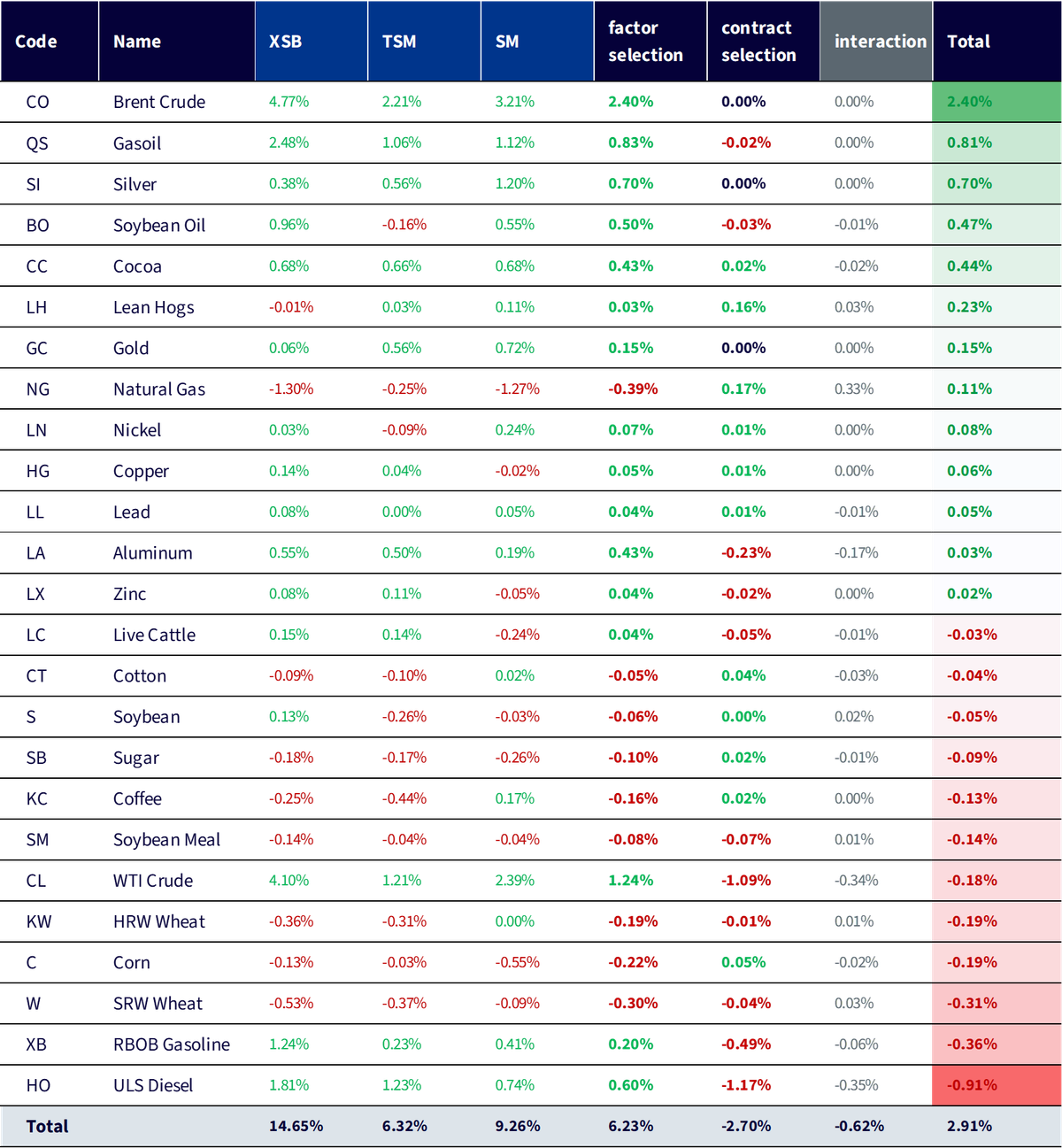

Table 1 presents the WisdomTree Enhanced Commodity Index’s active return relative to the Bloomberg Commodity Total Return Index at the commodity level. Each figure shows the percentage-point contribution to relative returns, broken down into allocation, selection and interaction (with interaction as the residual). Allocation reflects the impact of overweighting or underweighting individual commodities versus the Bloomberg Commodity Index, while selection captures the effect of holding different futures contracts. At a high level, allocation was the main driver, contributing +6.23%, partially offset by contract selection, which detracted -2.70%.

Source: WisdomTree, FactSet, Bloomberg. As of 31/03/2026. SM refers to the Slope Momentum factor and TSM refers to the Time-series Momentum factor. XSB refers to the Cross-sectional Backwardation factor. Historical performance is not an indication of future performance and any investments may go down in value.

Among factors, the strongest contributor has been Cross-sectional Backwardation5 (XSB column in the table), lifted by the very strong and early overweight in the oil complex. Slope Momentum and then Time Series Momentum followed in this order.

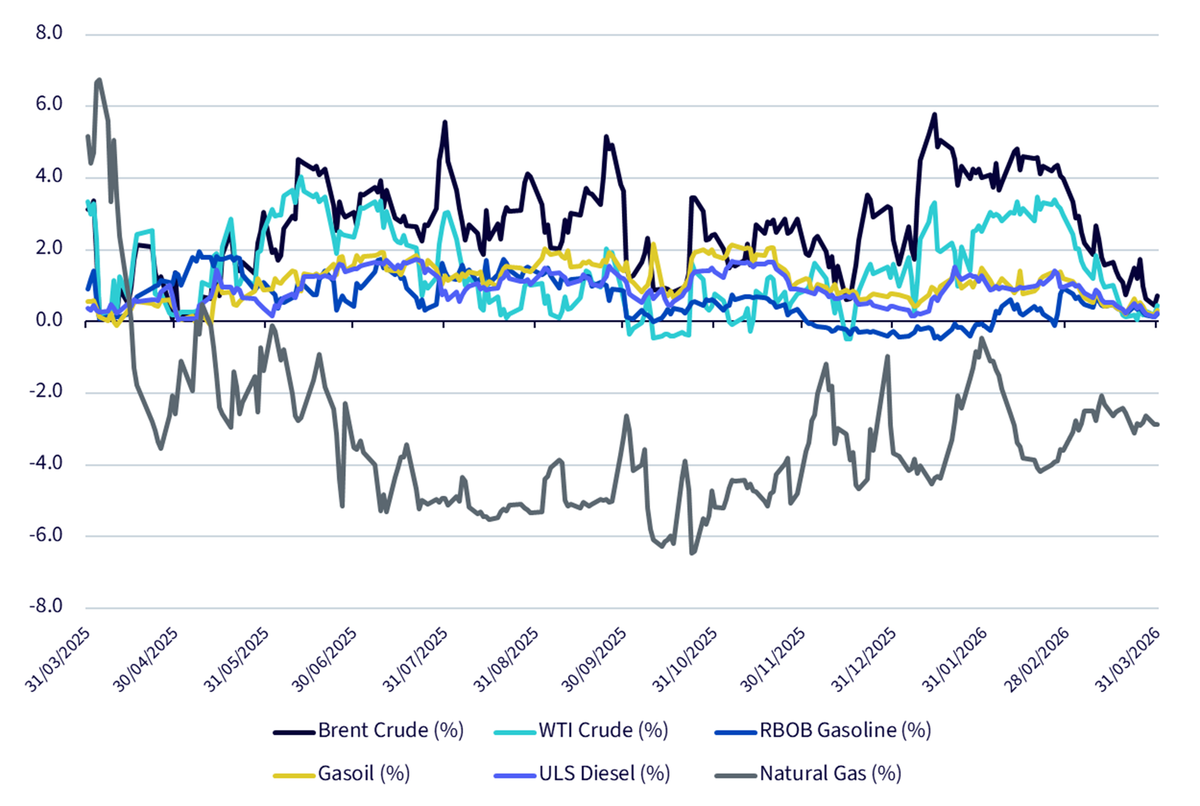

Energy was unsurprisingly the main driver of performance over the quarter. From the start of the year, the strategy was overweight all energy commodities except Natural Gas (Figure 3), which allowed it to capture the first leg of the oil rally after the conflict began. That positioning was deliberate: crude curves were already in backwardation and had steepened further ahead of the conflict, and the daily rebalancing framework allowed the strategy to reflect those signals quickly. The backdrop was a clear supply-risk shock: by mid-March, oil had risen more than 40% over the month at one point, Brent had moved above $103/bbl, and the Strait of Hormuz remained largely shut.

After the war began, the overweight in the oil complex was gradually reduced for two reasons. First, signals in other commodities improved, so the model reallocated part of the active risk more broadly across the basket rather than keeping it concentrated in energy. Second, the scope to maintain very large oil overweights was mechanically constrained by UCITS diversification limits, which cap how far the strategy can lean into any single commodity group.

Source: WisdomTree, FactSet. From 31/03/2025 to 31/03/2026. Historical performance is not an indication of future performance and any investments may go down in value.

Table 1 shows that Brent crude contributed approximately 2.40% to relative performance, with Gasoil adding a further 0.81%, bringing their combined contribution to around 3.21%. By contrast, WTI crude, RBOB gasoline and ULS diesel detracted roughly -1.50%, primarily due to contract selection. ULS diesel was the largest drag, as the seasonal contract selection pointed to the December contract during the rally (see Figure 4), while the Bloomberg Commodity Index remained positioned in the more responsive May contract. In a front-led rally, this difference in contract maturity led to underperformance relative to the benchmark. However, the structural overweight in these commodities helped offset some of this impact. Overall, the oil complex remained the primary driver of the WisdomTree Enhanced Commodity UCITS ETF’s outperformance versus the Bloomberg Commodity Index.

Natural gas also saw significant volatility, but for different reasons. In January, performance was negatively impacted as the strategy was underweight and positioned in the December 2026 contract, while the Bloomberg Commodity Index held the March 2026 contract. Colder-than-expected US weather drove a sharp rise in front-month prices, resulting in a drag of more than 2% by the end of the month. In February, this reversed: milder weather, ample inventories and strong production weighed on prompt prices, allowing the underweight and deferred positioning to recover losses. By quarter-end, natural gas contributed only around 11 basis points to relative performance, a relatively modest impact for a typically influential commodity.

Agriculture also played a meaningful role. Soybean oil contributed approximately +47 basis points, supported by strength across the energy and biofuel complex, with the strategy positioned overweight. Cocoa added around +44 basis points, driven by the opposite dynamic: the strategy was underweight a market that declined as demand softened and West African supply improved.

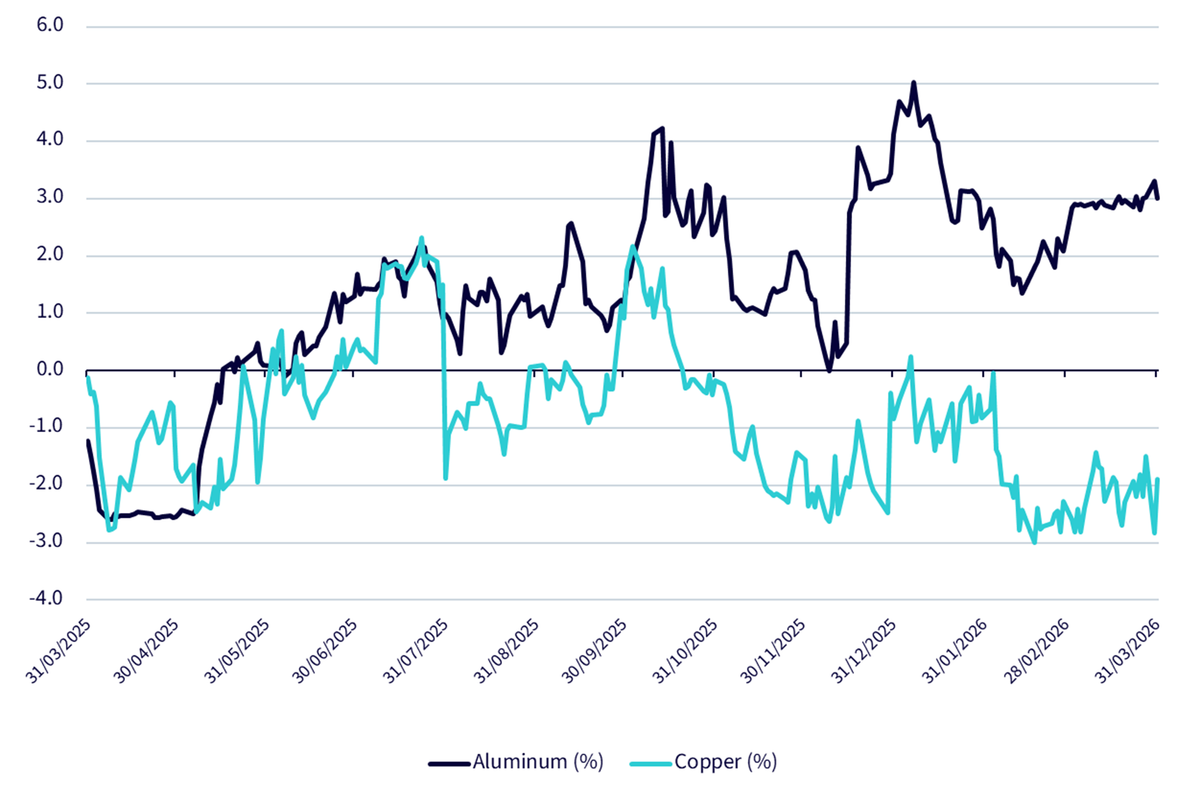

Industrial metals were not a major driver overall, but they illustrated the robustness of the process. Before the conflict, market sentiment favoured copper, while the strategy signals leaned towards aluminium. This positioning proved effective as the two metals diverged after the conflict began. Aluminium benefited from supply disruptions in the Gulf, including damage to facilities and shipping constraints, while copper faced pressure from weaker demand and rising inventories. Over Q1, aluminium returned 16.6%, while copper declined by 2.2%. The strategy added value through allocation across both metals, although some of this was offset by contract selection.

Source: WisdomTree, FactSet. From 31/03/2025 to 31/03/2026. Historical performance is not an indication of future performance and any investments may go down in value.

Q1 2026 saw strong benchmark performance, with front-end contracts leading and geopolitical developments reinforcing momentum-driven market conditions. In this environment, the WisdomTree Enhanced Commodity UCITS ETF Index still delivered relative outperformance, supported primarily by commodity allocation. Overall, the quarter provided an early test of the updated framework, highlighting how a curve-aware and factor-driven approach can remain effective across different market conditions, including periods of strong benchmark performance.

The broader takeaway from Q1 is how the WisdomTree Enhanced Commodity UCITS ETF behaved in a strong benchmark environment. The post-September framework maintained exposure to rising commodity markets while also generating relative gains, even in conditions where contract selection was less influential. Many enhanced commodity strategies tend to perform best when benchmark returns are weaker or when carry is a primary driver.

The WisdomTree Enhanced Commodity UCITS ETF invests in commodity futures and is exposed to the risks of commodity markets, which can be highly volatile and driven by geopolitical events, supply and demand dynamics and macroeconomic conditions. The fund uses a factor-based approach that may not perform as expected and can result in periods of underperformance. Concentrated exposures, particularly to energy, and the use of futures contracts introduce additional risks, including roll yield variability and liquidity risk. The value of investments may go down as well as up and investors may not recover the amount originally invested.

1 Source: WisdomTree, Bloomberg. Data from 31/12/2025 to 31/03/2026. Historical performance is not an indication of future performance and any investments may go down in value.

2 We refer to first generic natural gas contract, “NG1 Comdty” ticker in Bloomberg.

3 Ticker: WTENCME Index

4 By enhanced we mean an ETF which is departing from the Bloomberg Commodity Total Return Index in terms of contract selection and weighting.

5 Factor performances are calculated before applying caps and floors.

WisdomTree Enhanced Commodity UCITS ETF USD Acc

Associate Director, Quantitative Research at WisdomTree in Europe

Luca is an Associate Director in WisdomTree Europe's Research team, where he conducts quantitative research to enhance or develop new investment strategies, particularly in commodities and thematic equities. He also focuses on portfolio construction and optimisation. Before joining WisdomTree in 2022, Luca worked as a Quantitative Portfolio Manager at Euclidea SIM, a Milan-based fintech where he quantitatively managed multi-asset portfolios and developed and implemented statistical and machine learning models for investment strategies and fund selection. Luca holds a Master's degree in Finance from Bocconi University, Milan.