Corn reaping the benefits of Chinese demand

Published 27 April 2021

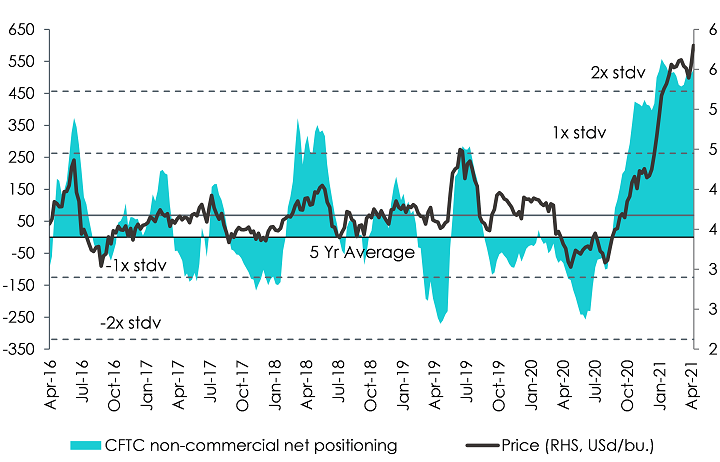

Corn is trading at an 8-year high1. Corn is primarily used as livestock feed, with much of the remainder processed into a wide range of food and industrial products including fuel ethanol. While the first phase of the US-China trade deal has some role to play in the increase of imports, it is not the only reason. China’s rising demand for animal feed for its recovering pig herd following the African Swine fever (over 2018 and 2019) is fuelling corn’s recent price surge. According to the Ministry of Agriculture in China, China’s pig herds were 26.9% higher in October 2020 over the prior year, paving the way for higher demand for animal feed. Net speculative positioning2 in corn has risen 2,768% since August 2020 and is now more than two standard deviations3 above its five-year average, as illustrated in the chart below. Forward-looking data suggests continued strong Chinese buying of US corn owing to widening domestic deficits.

Figure 1: Historical comparison of global Corn Price and CFTC net positioning

Source: Bloomberg, Commodity Futures Trading Commission (CFTC), WisdomTree from 5 April 2016 to 13 April 2021.

Historical performance is not an indication of future performance and any investments may go down in value.

Rising Chinese corn imports support demand

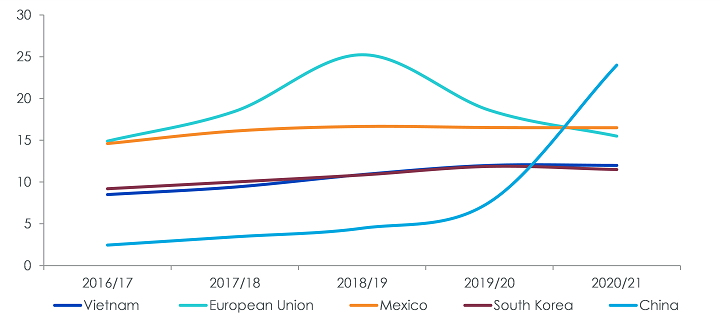

In 2020 China resumed its position as one of the top export markets for US agricultural products after signing the Phase One trade agreement. The United States Department of Agriculture (USDA) reported that US total sales and shipments to China stood at a record 17.7mn tons for 2020/21, at the end of January. Reflecting this large volume, Chinese imports estimates for 2020/21 have been raised by 6.5mn tons from January 2021 to 24mn tons by the USDA. This marks a threefold increase in Chinese corn import estimates from 7mn tons in October 2020 to 24mn tons in March 2021. According to China Customs Statistics and US Grain Inspections data indicate that imports will exceed China’s Tariff Rate Quota (TRQ) level of 7.2 million tons in 2020/21, we expect to see the Chinese government raise TRQs. As illustrated in the chart below, Chinese corn imports are expected to triple in 2020/21 according to the USDA. If the forecast were to be realised, it would make China the largest importer of corn by a sizeable margin outpacing the European Union and Mexico.

Figure 2: Global Corn Imports, 2016 – 2021 (Million Tonnes)

Source: USDA, Foreign Agricultural Services

Historical performance is not an indication of future performance and any investments may go down in value.

Another reason driving China’s corn imports were higher domestic corn prices which rose throughout the calendar year 2020, reaching US$3784 per ton in November 2020, marking its highest level since July 2015. With domestic corn prices continuing to run at record levels, China is expected to be a key player in global trade for corn.

Supply under strain owing to poor weather conditions in key growing areas

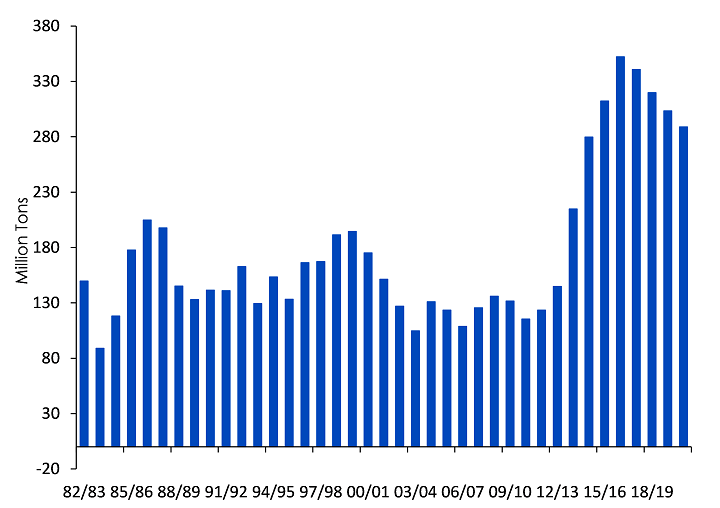

The global corn market is likely to be in a deficit for the fifth consecutive year in 2021/22, according to the International Grains Council (IGC). On a global level, corn ending stocks are set to decline to 284 million tons, which constitutes a downward revision of almost 4 million tons. The decline of US corn stocks is mainly responsible. In its April monthly report5 USDA predicted that US corn stocks would decrease to just 1.35 billion bushels by the end of the current 2020/21 crop year versus 1.5 billion bushels forecasted in the prior month. Despite the rise in corn prices, US corn acreage is expected to rise only marginally at less than half a percent.

Figure 3: Corn Ending Stocks (Annual data from 1982 – 2020)

Source: USDA, Bloomberg, WisdomTree as of 12 April 2021.

Historical performance is not an indication of future performance and any investments may go down in value.

Current cold temperatures in the US which are forecast to continue, are hampering the progress of the initial growth of the seeds. Expectations for the Brazilian corn crop are also being negatively impacted by dry conditions over the past few weeks. We expect deteriorating climate conditions for the second harvest of the year in key growing regions is likely to widen the current deficit estimates on the global corn market. The short end of the corn futures curve is backwardated, providing a positive roll yield of 2.6%, which suggests near term tightness on the corn market.

Conclusion

Corn has had a strong run over the past year, and we expect strong fundamentals coupled with improving sentiment to continue to support its upward trajectory.

1 As on 20 April 2021.

2 Commodity Futures Trading Commission (CFTC).

3 Standard deviation is a measure of the amount of variation or dispersion of a set of values.

4 United States Department of Agriculture.

5 World Agriculture Supply and Demand Estimates (WASDE) Report.

Related products

Categories

About the contributor

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.