WisdomTree brings a new asset class to the ETP structure: CoCo bonds

Published 22 May 2018

Global Head of Research

2018 marks the ten-year anniversary of the global financial crisis of 2008-09. The financial system has truly come a long way from this point and is in a much better position to endure an economic downturn today, should one occur.

The United Kingdom example: Strong results from the Bank of England’s stress test

After the Global Financial Crisis of 2008-09, Central Banks clearly understood the importance of regularly gauging the capability of their respective banking systems to withstand difficult economic environments. When performing a stress test in 2017, the Bank of England took into consideration the following hypothetical conditions:

WisdomTree introduces a diversified approach to CoCo Bonds within the ETP structure

Contingent Convertible Bonds, or CoCo bonds, represent a way in which banks can buttress their Tier 1 capital requirements, otherwise reserved for common equity and retained earnings. This layer of the capital structure is intended to absorb losses in the event of severe market stress and serves as a cushion between equity and more senior debt.

To meet Basel III capital requirements drafted after the financial crisis, European banks began issuing Contingent Convertible Bonds. Depending on the terms and conditions, a CoCo is classified as either AT1 or Tier 2 (T2) capital. A unique feature of CoCos is their trigger and loss absorption mechanism. A CoCo trigger is the prescribed level which, when breached, activates the loss absorption mechanism. The loss absorption mechanism is the action taken thereafter. Under the conditions of the UK stress tests at the end of 2017, the prescribed trigger level of 7%, would not have been breached.

Balancing the risk of CoCos with the benefits of higher income

AT1 CoCos offer a higher yield than other bank debt since they are lower on the capital structure, right above equities. From the issuers’ standpoint, CoCos are attractive because the coupon payments are fully tax-deductible and the cost of raising capital by issuing an AT1 CoCo bond is lower than that of share capital increase.

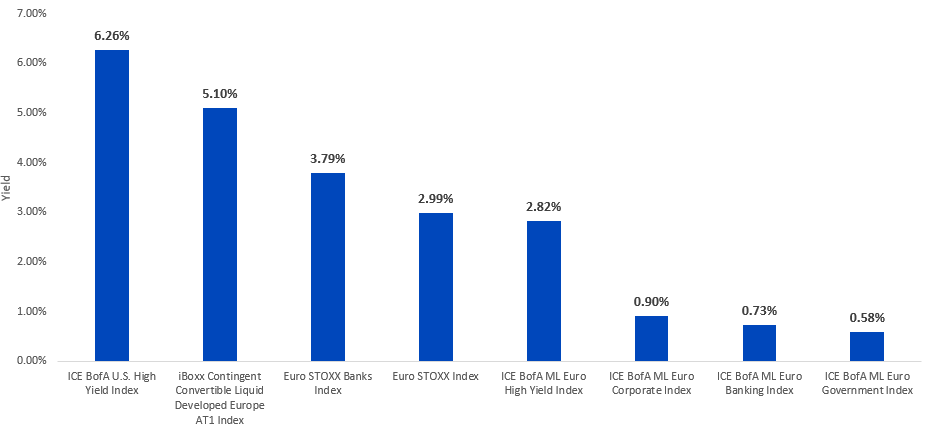

CoCos have high yields relative to other European-focused asset classes (as of 27 April 2018)

Source: Bloomberg. Past performance is not indicative of future results. You cannot invest directly in an Index

- Within Europe, yields on fixed income indexes are quite low—even the ICE BofA ML Euro High Yield Index was only at about 2.8% as of 27 April 2018. This was below the dividend yield of the Euro STOXX Index as well as that of the Euro STOXX Banks Index.

- The iBoxx Contingent Convertible Liquid Developed Europe AT1 Index was at 5.10%. Yes, CoCos clearly have unique risks, but the crucial question is whether the incremental gain in potential income is enough to compensate investors for these risks. We think that, as long as CoCo issuers have reasonably sound fundamentals, they can be quite attractive.

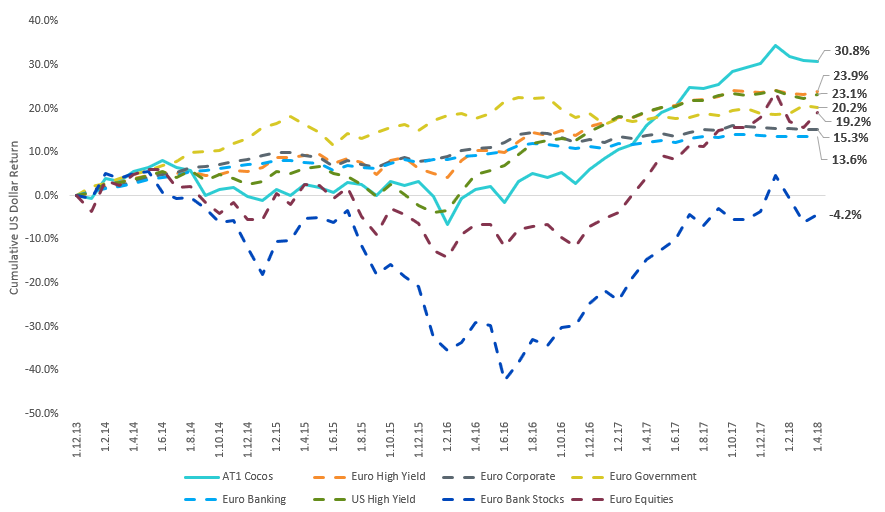

Of course, yield is only one part of the picture—the total return of a particular fixed income index captures the impact of yield but also of other factors, like capital appreciation. On a total return basis, since the end of 2013, CoCo returns have been strong. Conceptually, we also believe that it is important to hold a diversified array of these securities, given the unique risks of the asset class. While issues haven’t been widespread, close followers of European banks would likely remember Banco Populare and Deutsche Bank having their own idiosyncratic events over the past few years. While holding these specific AT1 CoCos during these times of stress would not have been pleasant, a diversified approach to the asset class was one way to mitigate these single security risks.

Cumulative returns of AT1 CoCos have outperformed since the end of 2013 (31 December 2013 to 30 April 2018)

Source: Bloomberg. Past performance is not indicative of future results. You cannot invest directly in an Index. AT1 Cocos: iBoxx Contingent Convertible Liquid Developed Europe AT1 Index, Euro High Yield: ICE BofA ML Euro High Yield Index, Euro Corporate: ICE BofA ML Euro Corporate Index, Euro Government: ICE BofA ML Euro Government Index, Euro Banking: ICE BofA ML Euro Banking Index, U.S. High Yield: ICE BofA U.S. High Yield Index, Euro Bank Stocks: Euro STOXX Banks Index, Euro Equities: Euro STOXX Index.

Market access

The most notable takeaway is that, after WisdomTree’s launch, investors now have a diversified manner to access an asset class that was formerly quite difficult. It is a great illustration of how the exchange-traded product structure is able to bring transparency and lower cost to an area of the market that formerly would have been deemed the sole province of active managers.

1 Source: Bank of England, 2017.

You may also be interested in reading:

+ WisdomTree Launches World’s First CoCo Bond ETF

+ Contingent Convertible Bonds

Related products

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.