VOLT LN

WisdomTree Battery Solutions UCITS ETF - USD Acc

Published 23 July 2024

Senior Associate, Quantitative Research and Multi Asset Solutions

China’s four-day Third Plenum, typically focused on economic policies and reforms, concluded on 18 July 2024. Historically, these meetings have introduced significant changes, such as Deng Xiaoping's "reform and opening-up" policy in 1978, which catalysed China's economic growth. Held every five years, the outcomes of these meetings often have lasting impacts on the nation's economy.

Given the closed-door nature of the Third Plenum, only a brief communique has been released as of writing of this article on 19 July 2024, leaving the specifics of the decisions unknown. Initial market reactions were subdued, with the Shanghai Stock Exchange Composite Index rising 0.17% and the Hang Seng Index falling 2.0%1 the day after the meeting. While the communique and the detailed follow-up documents cover a broad range of topics, we can glean some insights and potential impact from the current communique and market expectations.

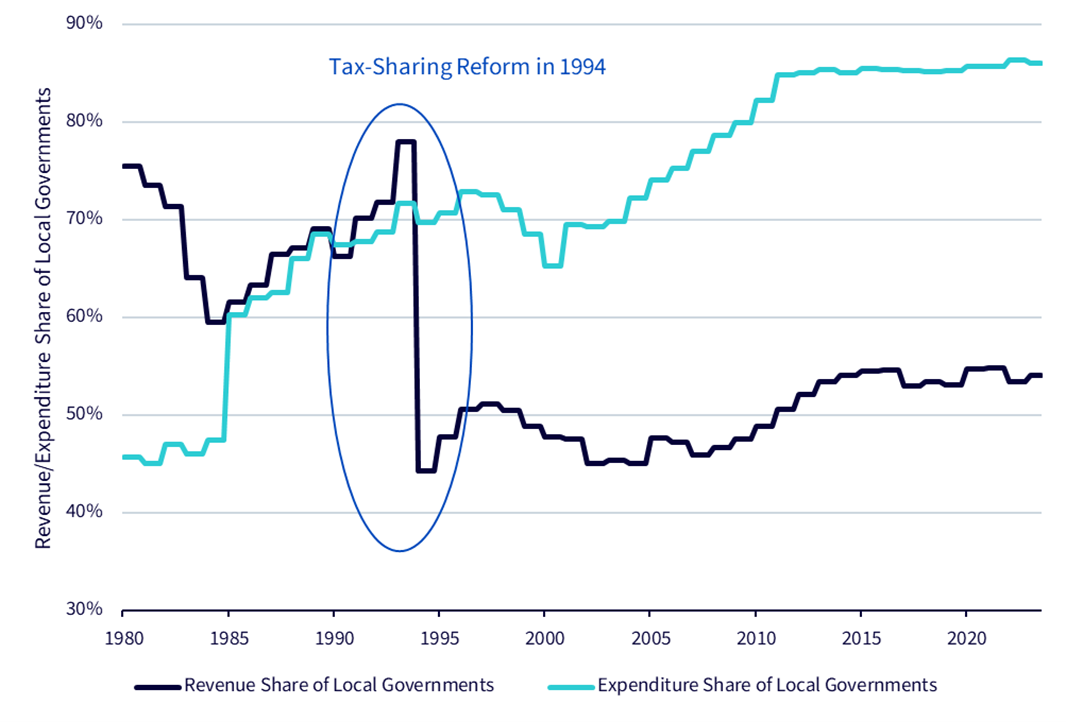

Local government debt, which reached 76% of China’s GDP in 20222, poses a significant financial risk. In response, the central government has implemented measures to mitigate this risk, including cutting local government spending and halting infrastructure investments3. The debt issue stems from a tax-sharing reform 30 years ago that favoured the central government, leaving local governments reliant on land sales and debt.

Source: Bloomberg, National Bureau of Statistics of China. Historical performance is not an indication of future performance and any investment may go down in value.

The Third Plenum's press conference indicated that the central government will assume a larger share of expenditures and expand tax resources for local governments to alleviate financial pressure. The market anticipates that consumption tax revenue, currently collected by the central government, may be partially redirected to local governments. This fiscal reform aims to address long-standing tax imbalances and reduce debt-related risks. Although the effectiveness of these policies will take time to assess, implementing systemic reforms promises more enduring outcomes than previous temporary measures, ultimately mitigating the risks associated with local debt and fostering the revitalisation of China’s economy.

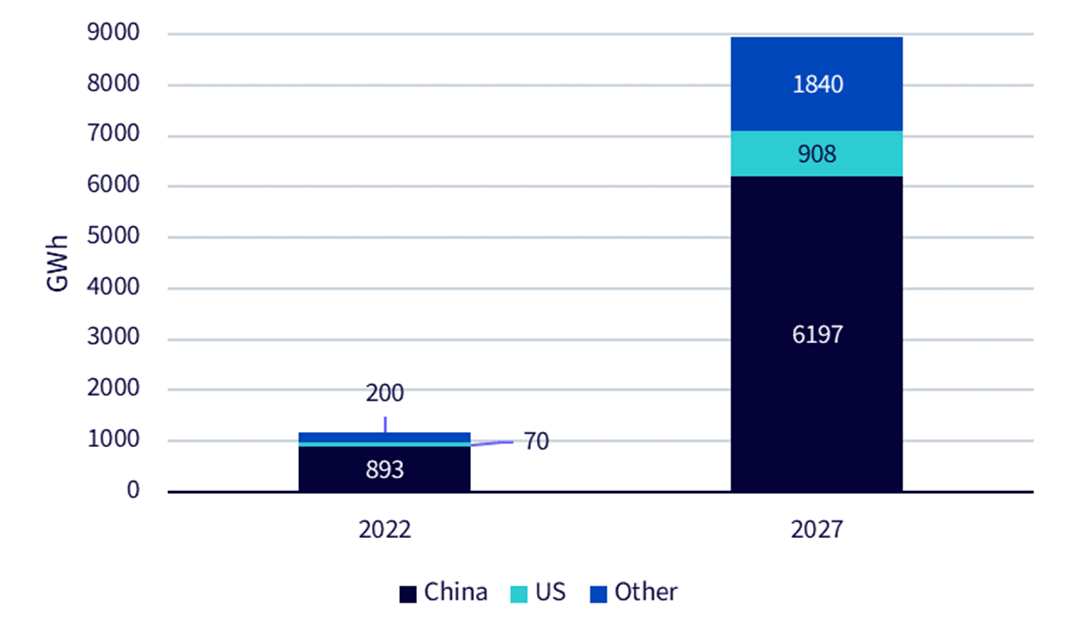

The communique emphasizes support for “new quality productive forces,” a term referring to “advanced productivity freed from traditional economic growth modes and productivity development paths”4, including green energy, biotech, advanced information technology etc. The Chinese leadership believes these sectors will drive the next phase of economic growth, placing a significant bet on their potential to transform the economy. This terminology, “new quality productive forces,” was first introduced by the Chinese leadership late last year, marking a strategic shift towards innovation-driven development.

Source: Bloomberg New Energy Finance (BNEF) as illustrated by Visual Capitalist, January 2023. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

While the communique outlines intentions to achieve key technological breakthroughs, specific details are lacking. Early this year, China announced plans to promote the “high-end, intelligent and green”5 manufacturing. The market will be watching for further information in subsequent documents to assess the long-term impact on these industries. Anticipated support for such manufacturing could create significant investment opportunities, meriting continued attention.

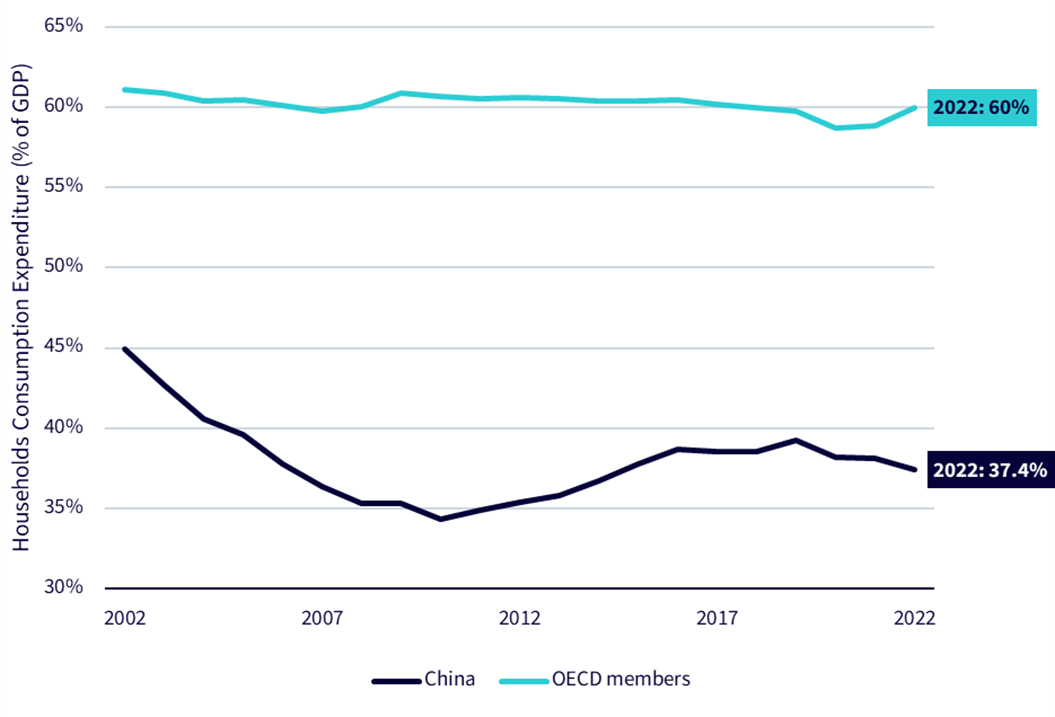

China's Consumer Price Index (CPI) year-on-year (YoY) turned negative last year, slightly rebounding to 0.2%6 in June 2024, while the Producer Price Index (PPI) YoY remains below in the same month. Despite interest rate and reserve requirement ratio (RRR) cuts earlier this year, the market is keen to know if there will be a massive stimulus, particularly for the consumption sector, to combat deflation risks. Weak GDP growth and declining household consumption share have fuelled these expectations.

Source: World Bank. Historical performance is not an indication of future performance and any investment may go down in value.

The Third Plenum’s communique does not provide details on a potential massive stimulus plan. However, it mentions plans to improve the social safety net for low-income populations in rural and less developed areas, which could be a form of indirect stimulus. The effectiveness of these measures will become clearer with more information from follow-up documents.

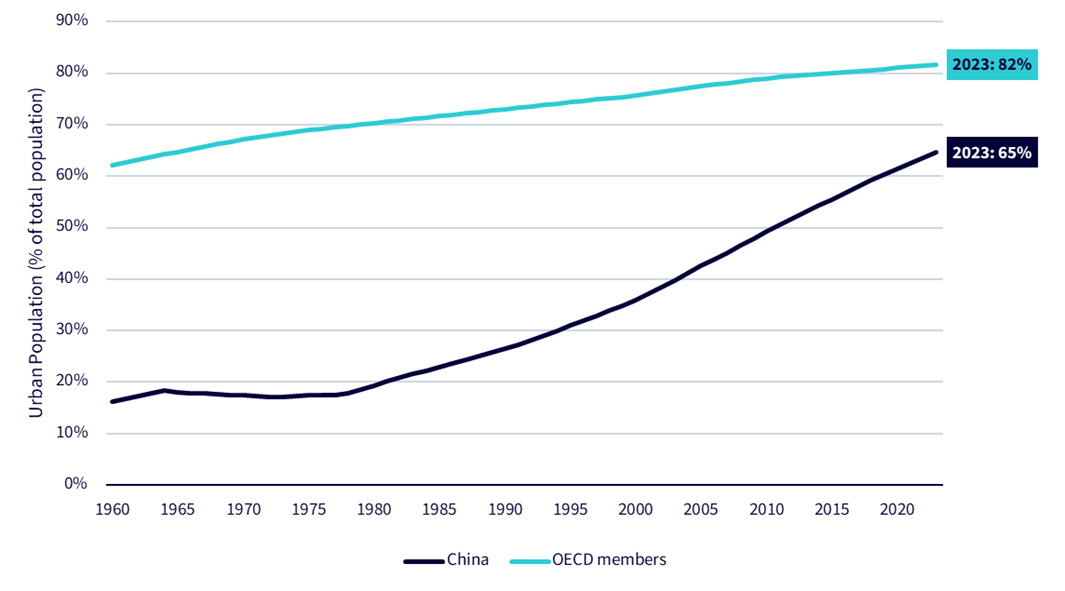

The declining housing market has strained China's economy and local government finances. One potential solution is to boost demand by accelerating urbanization. China's urban population has increased significantly over the past three decades, driving the housing boom, yet there is still potential for further urbanization compared to OECD countries.

Source: World Bank. Historical performance is not an indication of future performance and any investment may go down in value.

A government official highlighted during the Plenum's press conference that improving public services for migrant workers and easing urban residential permit controls7 are priorities. These measures aim to drive people to move from rural areas to urban areas, potentially revitalizing the housing market.

China's leadership faces a unique economic landscape, characterized by weak growth and deflation risks. Initial insights from the Third Plenum suggest a preference for mild, long-term policies over drastic stimulation. While the communique offers few new details on economic policy, it underscores existing measures. The long-term effects of these policies will take time to materialize, but the focus on specific industries could provide potential opportunities. These industries, particularly in the manufacturing with a high market share and advanced technology, might benefit from the new policies, offering potential growth despite broader economic uncertainties.

1 Source: Bloomberg.

2 Reuters, Exclusive: China orders indebted local governments to halt some infrastructure projects-sources, https://www.reuters.com/world/china/china-orders-indebted-local-governments-halt-some-infrastructure-projects-2024-01-19/

3 Financial Times, China’s treatment of local debt ‘ulcer’ threatens growth target, https://www.ft.com/content/901bc68e-ad35-42eb-97e0-542c631b9033

4 State Council Information Office of China, http://english.scio.gov.cn/chinavoices/2024-03/28/content_117091519.htm

5 Chinese Central Government, https://www.gov.cn/zhengce/202401/content_6923789.htm

6 Source: National Bureau of Statistics of China.

7 China relies on a residential system called “Hukou” to control population and allocate resources. The “Hukou” system classifies residents based on their residential status (urban or rural) and location. This status determines access to public services such as education, healthcare, and social security. Urban Hukou holders typically have better access to these services compared to rural Hukou holders. In the past, there were many restrictions on transferring status from rural to urban, but some of these restrictions have been gradually lifted in recent years.

WisdomTree Battery Solutions UCITS ETF - USD Acc

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).