Case study: quality factor at work in the Eurozone

Published 11 June 2018

Global Head of Research

As the month of May comes to an end one word is on the forefront of equity investors’ minds, particularly those with exposure to the Eurozone: volatility. Volatility has presented itself on the potential for trade wars, President Trump’s announcements on the Iran deal, and the complex and ongoing issues surrounding Italy and the formation of the government.

Battle-testing the quality factor

In periods where markets seem to run ever higher with minimal volatility and barely any corrections of 5% or more, it is difficult to make the case that the quality factor is needed within an equity exposure to add value. Momentum strategies fit the bill more appropriately in those types of scenarios.

Historically, we have seen that quality-oriented approaches tend to be at their relative best during periods of increased volatility and even market drawdowns.

May of 2018, with all its negative headlines, was a month to battle test WisdomTree’s Eurozone Quality Dividend Growth strategy in real time.

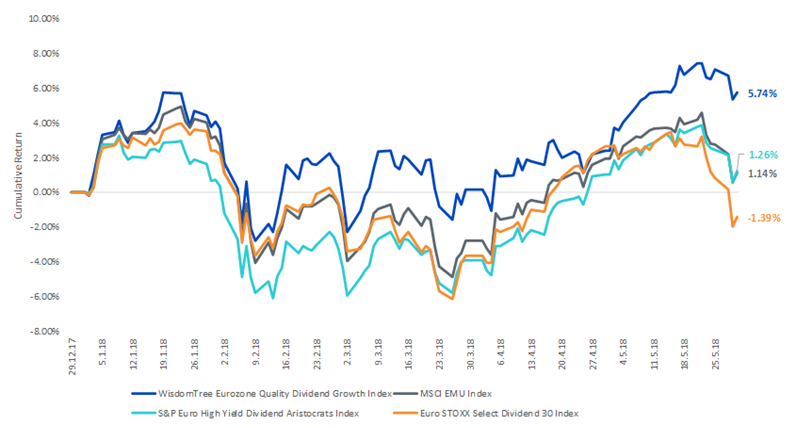

Figure 1: Year-to-date 2018: Eurozone quality has been strong

Source: Bloomberg, with data from 31 December 2017 to 30 May 2018.

Past performance is not indicative of future results. You cannot invest directly within an Index.

For those following dividend-focused eurozone equity strategies in 2018, the performance environment has been challenging. The S&P Euro High Yield Dividend Aristocrats and Euro STOXX Select Dividend 30 Indexes both have a large following, but the key thing to remember is that, as of 30 April 2018:

- The S&P Euro High Yield Dividend Aristocrats Index had 40 constituents.

- The Euro STOXX Select Dividend 30 Index had 30 constituents.

These are fairly concentrated baskets of Eurozone equities. By contrast, the WisdomTree Eurozone Quality Dividend Growth Index had 99 constituents as of this date.

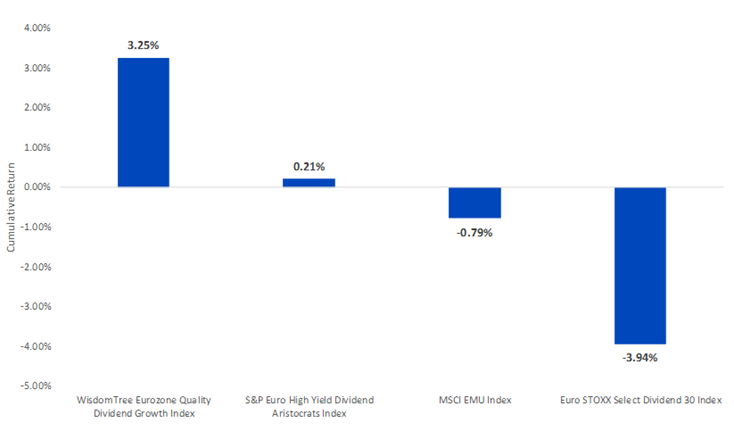

Figure 2: The May 2018 period: Italy as a catalyst for volatility

Source: Bloomberg, with data from 30 Apr. 2018 to 30 May 2018. Past performance is not indicative of future results.

You cannot invest directly within an Index.

Uncertainty surrounding the capability of Italy to form a government was the catalyst for major Eurozone equity market volatility in the month of May. Yet the WisdomTree Eurozone Quality Dividend Growth Strategy was able to still deliver a positive return of nearly 3.3%.

This compares to a 0.21% return for the S&P High Yield Dividend Aristocrats Index and a -3.94% return for the Euro STOXX Select Dividend 30 Index.

All dividend strategies are NOT equal

The WisdomTree Eurozone Quality Dividend Growth, S&P Euro High Yield Dividend Aristocrats and Euro STOXX Select Dividend 30 Indexes all have the word “dividend” in the title, but it is striking how different they truly are. We already mentioned the numbers of constituents, but additionally:

- Index Weighting: The WisdomTree strategy is weighed by cash dividends, meaning the companies that distribute the greatest amounts of cash receive the biggest weights. Both the S&P and the STOXX Indices are much more yield driven in the weighting schemes. We hesitate to say that either approach is good or bad—unfortunately in these matters things are rarely black and white. Yield driven weighting schemes deliver a higher dividend yield, which some investors may find interesting. However, companies with the highest yields may not necessarily have the healthiest balance sheets, strongest earnings growth or look positive on other quality-oriented attributes.

- Financials Exposure: With events in Italy, some investors have become quite sensitive to Financials weightings within their Eurozone equity positions. As of 30 April, the WisdomTree strategy had a less than 2.3% exposure to Financials. Now, within the MSCI EMU Index, a market capitalization-weighted benchmark for the Eurozone, the Financials exposure is more than 20.2%. The WisdomTree Eurozone Quality Dividend Growth Index actually penalizes firms in its ranking criteria that use high leverage, and Financials fit in this category. As of 30 April 2018:

- The S&P Euro High Yield Dividend Aristocrats Index had a Financials exposure of 9.7%

- While the Euro STOXX Select Dividend 30 Index utilizes a slightly different sector categorization schematic in its reporting, it is notable that 14.1% of the exposure was in Banks.

- Italy Exposure: Of course, we’d be remiss to not mention the country exposures of the 3 Indexes to Italy, as well as that of the MSCI EMU Index to get a sense of where Italy’s market capitalization weight would place it on the spectrum. As of 30 April 2018:

- The MSCI EMU Index had a 7.80% weight to Italy.

- The WisdomTree Eurozone Quality Dividend Growth Index had a 6.46% weight to Italy.

- The S&P Euro High Yield Dividend Aristocrats Index had a 13.0% weight to Italy.

- The Euro STOXX Select Dividend 30 Index had a 15.6% weight to Italy.

Continue to look to quality for potential in volatile markets

As of this writing, we cannot say for sure where the story in Italy will take us. What we can say is that the indexes mentioned in this piece all have defined, repeated, rules-based methodologies that apply at regular intervals. If markets are expected to be more volatile, why not focus exposure on firms with lower leverage, higher return on equity, higher return on assets and better forward-looking earnings growth expectations?

Categories

About the contributor

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.