NTSX LN

WisdomTree US Efficient Core UCITS ETF - USD Acc

Published 20 February 2025

Head of Research, WisdomTree Europe.

When it comes to trying to outperform the equity markets, investors must usually rely on doing their own stock picking, investing in an active manager strategy, or using a systematic equity factor strategy. Whether they realise it or not, in all cases they engage in factor investing, as academic research and empirical data have consistently showed that much of the excess returns generated by active funds or stock picking in general can be traced back to systematic tilts toward well-documented equity factors such as Value, Momentum, Quality, and Minimum Volatility.

This is not a bad thing, as factor investing offers many potential advantages to investors. Factors provide systematic, repeatable sources of return by harnessing long-term premia that persist across market cycles. They also enhance diversification, as different factors tend to behave differently across the business cycle – some being more cyclical, others more defensive, and some acting as all-weather strategies. By thoughtfully combining factors such as Value, Minimum Volatility, or Quality, investors can construct more efficient equity portfolios with improved risk-adjusted returns.

Building on this idea, what if investors could access an additional source of return premia—one not based on stock-specific characteristics but on a fundamental market dynamic? The well-documented diversification benefits between equities and bonds create a powerful mechanism for improving risk-adjusted returns when structured efficiently.

By leveraging a traditional 60/40 portfolio to match the volatility of equities, investors can achieve a higher Sharpe ratio while maintaining a risk level similar to that of pure equity investments. This approach systematically captures the bond-equity diversification premium, functioning as a new ‘factor’ in its own right—one that can serve as both a complement to existing equity exposures and a potential replacement for traditional equity allocations.

WisdomTree has developed the Efficient Core strategy, a unique investment framework designed to maximise the benefits of the bond-equity diversification premium. The strategy consists of:

By dynamically combining equity and bond exposures in a leveraged, risk-balanced structure, the Efficient Core approach enhances the traditional 60/40 portfolio while preserving equity-like characteristics. In essence, this Efficient Core functions as a new equity factor—one rooted in the bond-equity diversification premium—offering investors an alternative or complementary way to enhance their equity exposure.

Figure 1 highlights that the WisdomTree US Efficient Core strategy (a portfolio investing 90% to physical US large cap equities and 60% to a portfolio of 5 US Treasury Bond future contracts) behaves like other equity factors by delivering similar outperformance and an improved Sharpe ratio.

Growth | Min Volatility | Quality | Small Cap | High Dividend | |

|---|---|---|---|---|---|

Annualised Returns | 9.9% | 8.4% | 8.8% | 9.8% | 8.1% |

Outperformance | 1.4% | -0.1% | 0.3% | 1.3% | -0.4% |

Volatility | 20.6% | 15.8% | 18.6% | 23.0% | 17.5% |

Sharpe ratio | 0.40 | 0.42 | 0.38 | 0.35 | 0.37 |

Tracking Error | 5.5% | 6.3% | 3.2% | 9.5% | 6.6% |

Information Ratio | 0.25 | -0.02 | 0.09 | 0.13 | -0.06 |

Value | Momentum | WisdomTree US Efficient Core | S&P 500 Total Return | |

|---|---|---|---|---|

Annualised Returns | 8.7% | 9.8% | 9.1% | 8.5% |

Outperformance | 0.2% | 1.3% | 0.6% |

|

Volatility | 20.6% | 20.0% | 16.7% | 19.2% |

Sharpe ratio | 0.34 | 0.40 | 0.44 | 0.35 |

Tracking Error | 6.0% | 8.2% | 4.4% |

|

Information Ratio | 0.03 | 0.15 | 0.13 |

Source: WisdomTree, Bloomberg. 31 December 2000 to 31 January 2025. Includes backtested return. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

Beyond outperformance, one of the defining characteristics of equity factors is their low correlation with one another. This diversification benefit is a critical advantage in portfolio construction. Figure 2 demonstrates that the excess returns of the WisdomTree US Efficient Core strategy exhibit similarly low correlations with traditional equity factors, reinforcing its potential as a distinct factor-like strategy.

Source: WisdomTree, Bloomberg. 31 December 2000 to 31 January 2025. Includes backtested return. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

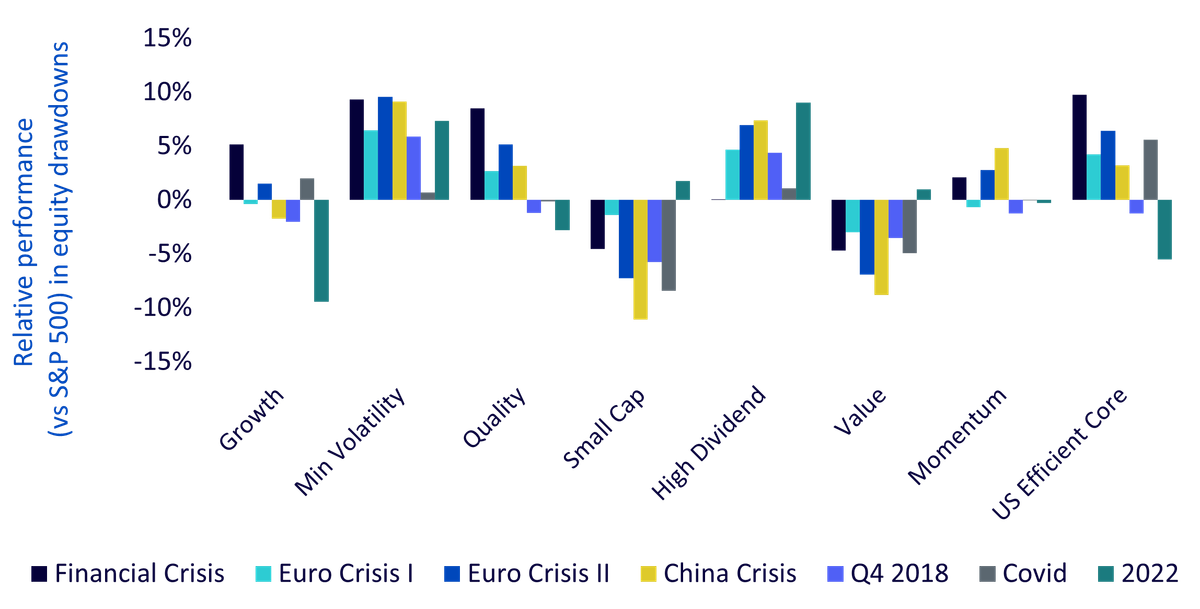

As discussed, different equity factors behave differently across market cycles. Minimum Volatility tends to be defensive, outperforming during equity drawdowns, while Value is more cyclical and performs well early in the cycle. If WisdomTree Efficient Core acts as a new factor, understanding its behaviour across different market environments is essential.

A useful way to assess this is by analysing performance in major equity market drawdowns. Figure 3 highlights the relative performance of various equity factors and WisdomTree US Efficient Core during the seven largest equity market declines since 2000. The results show that, while Minimum Volatility remains the most defensive, consistently reducing drawdowns across all periods, cyclical factors such as Value and Small Caps tend to struggle. WisdomTree US Efficient Core, however, demonstrates a balanced defensive tilt—outperforming in five of the seven downturns and effectively mitigating losses.

Source: WisdomTree, Bloomberg. 31 December 2000 to 31 January 2025. Includes backtested return. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

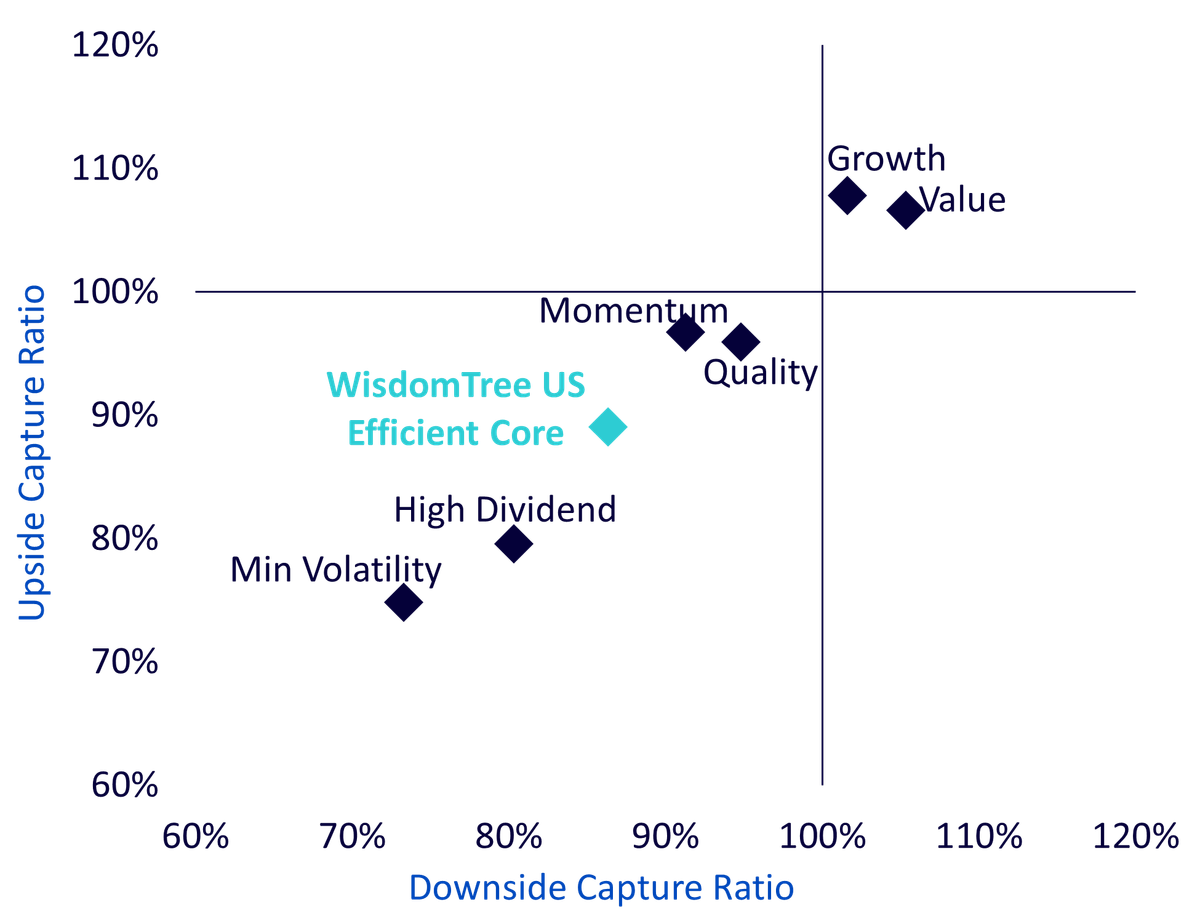

Another way to assess defensiveness is through upside and downside capture ratios, which measure how much a strategy participates in market gains versus losses. Figure 4 illustrates that, while WisdomTree US Efficient Core is slightly defensive, it is less so than Minimum Volatility. Notably, its upside/downside asymmetry is particularly strong, with an upside capture ratio of 89% and a downside capture ratio of 86%, reinforcing its ability to enhance returns while preserving capital.

Source: WisdomTree, Bloomberg. 31 December 2000 to 31 January 2025. Includes backtested return. You cannot invest directly in an index. Historical performance is not an indication of future performance and any investments may go down in value.

The WisdomTree Efficient Core strategy introduces a new dimension to equity investing, leveraging the bond-equity diversification premium to create a new solution for equity outperformance. With comparable long-term returns to equities, a higher Sharpe ratio, and built-in defensive characteristics, WisdomTree Efficient Core serves as both a potential complement to equity portfolios and replacement for traditional equity exposures.

Just as Value, Momentum, and Minimum Volatility offer unique return characteristics, the WisdomTree Efficient Core strategy brings a new, systematic approach to enhancing equity investing. As market conditions evolve, incorporating this strategy into portfolios could provide investors with a more resilient and efficient path to long-term outperformance.

Footnotes:

Definitions for the drawdown periods

Head of Research, WisdomTree Europe.

Pierre Debru leads WisdomTree’s European research team and plays a pivotal role in the strategic direction of our European research efforts. His key areas of expertise extend across equity factors and quantitative strategies, portfolio construction and model portfolios, and thematic and crypto investments. Before joining the company in 2019, Pierre worked in Investment Research for DWS and the Xtrackers range for over five years. During this period, he focused on smart beta investments, model portfolio construction and thought leadership. Pierre has over 20 years of experience in investments and structured asset management. He graduated from Ecole Central Paris and obtained a Master of Science in Mathematics applied to Finance.