PCOM LN

WisdomTree Broad Commodities UCITS ETF - USD Acc

Published 29 January 2026

Associate Director, Quantitative Research

The average European eats around 6 kilograms of chocolate every year1. Recent spikes in cocoa bean prices have fed directly into prices on the shelves around the world, offering a clear example of how agricultural supply shocks translate into consumer inflation.

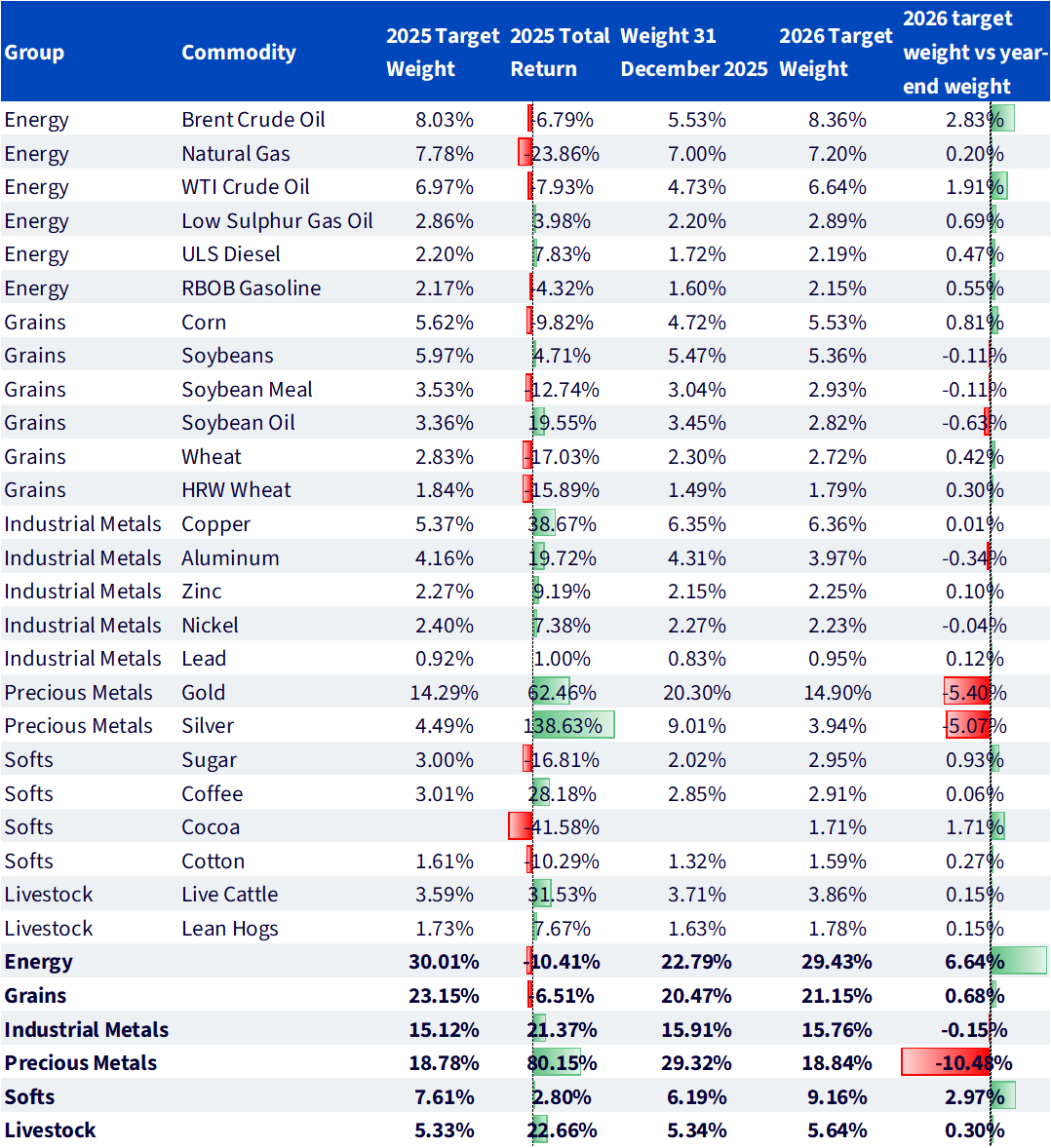

In the 2026 annual rebalancing, Bloomberg has included cocoa bean futures in its widely followed Bloomberg Commodity Index (BCOM). The index’s methodology aims to capture commodities that represent key real-economy inputs, with weights determined by global production and futures market liquidity.

Cocoa enters the index with a target weight of approximately 1.7%. At the same time, precious metals weights are being reset following strong relative performance in 2025, with target weights in 2026 close to those of 2025. Similarly, energy commodities, including Brent and WTI crude, return to weight levels seen at the beginning of 2025.

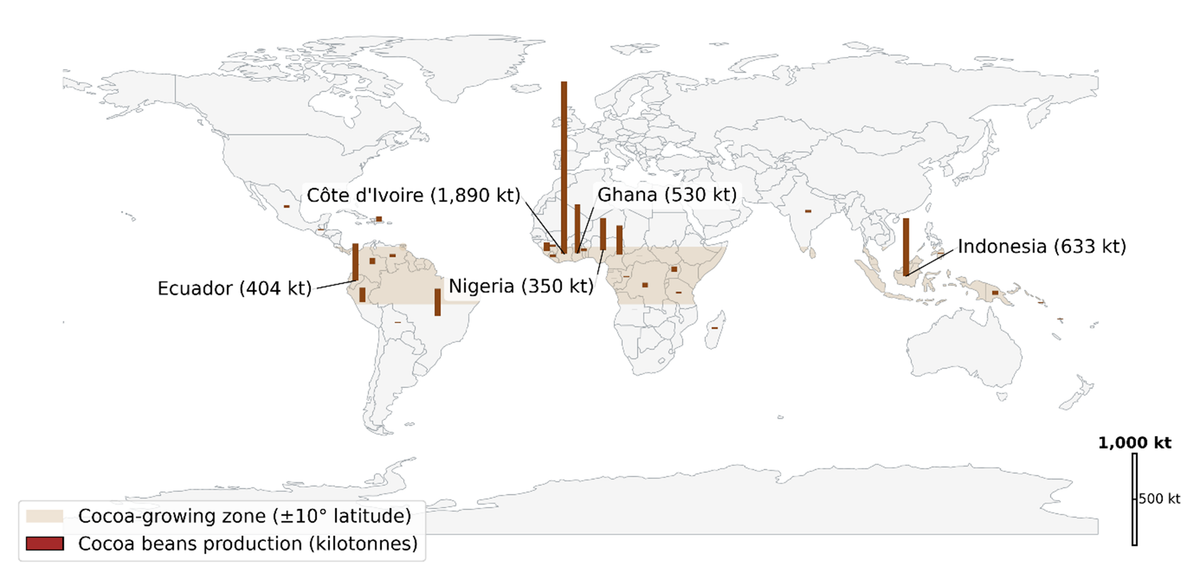

Cocoa production is highly concentrated, with the majority of global supply originating from a small number of countries within a narrow equatorial belt, most notably Côte d’Ivoire and Ghana (Figure 1). The geographic concentration makes global supply particularly sensitive to regional disruptions.

Source: Food and Agriculture Organization of the United Nations, WisdomTree. Production numbers in kilotonnes as of 2024.

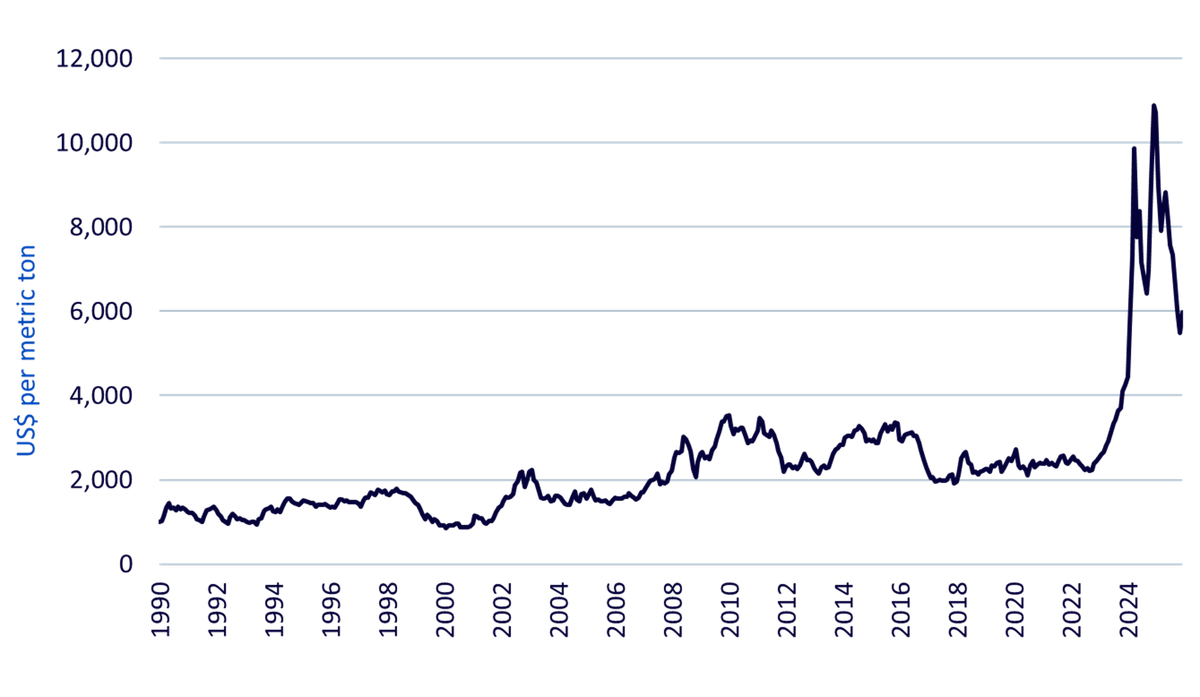

In recent years, cocoa yields have come under sustained pressure from adverse weather patterns, the spread of plant disease, ageing tree stock, and prolonged underinvestment at the farm level. These factors have constrained supply growth at a time when demand has remained resilient2.

The result has been a sharp increase in price volatility and a series of pronounced price spikes (Figure 3).

Source: IMF, International Cocoa Organization cash price, CIF US and European ports. From January 1990 to September 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Alongside the addition of cocoa beans, the most visible impact of the 2026 rebalancing is the reversal of the performance-driven weight concentration that accumulated over 2025 (Table 1). In determining the annual target commodity weights, the index relies on liquidity data and US dollar-weighted production data, rather than recent price performance.

Following the strong 2025 returns for gold (+62.46%3) and silver (+138.63%3), the weight of precious metals increased from approximately 19% to 29% over the course of the year. As the target weights for 2026 do not materially differ from those of 2025, the index’s rules-based rebalancing process reduces precious metals exposure back to its production-based allocation.

Energy commodities, which broadly declined in 2025 (-10.41%3), see the opposite effect. In line with the same methodology, allocations to Brent and WTI crude increase relative to year-end weightings, reflecting their underlying economic footprint rather than recent returns.

Source: Bloomberg. Total return from 31 December 2024 to 31 December 2025. The annual rebalancing has been implemented from the 9-15 of January 2026. Historical performance is not an indication of future performance and any investments may go down in value.

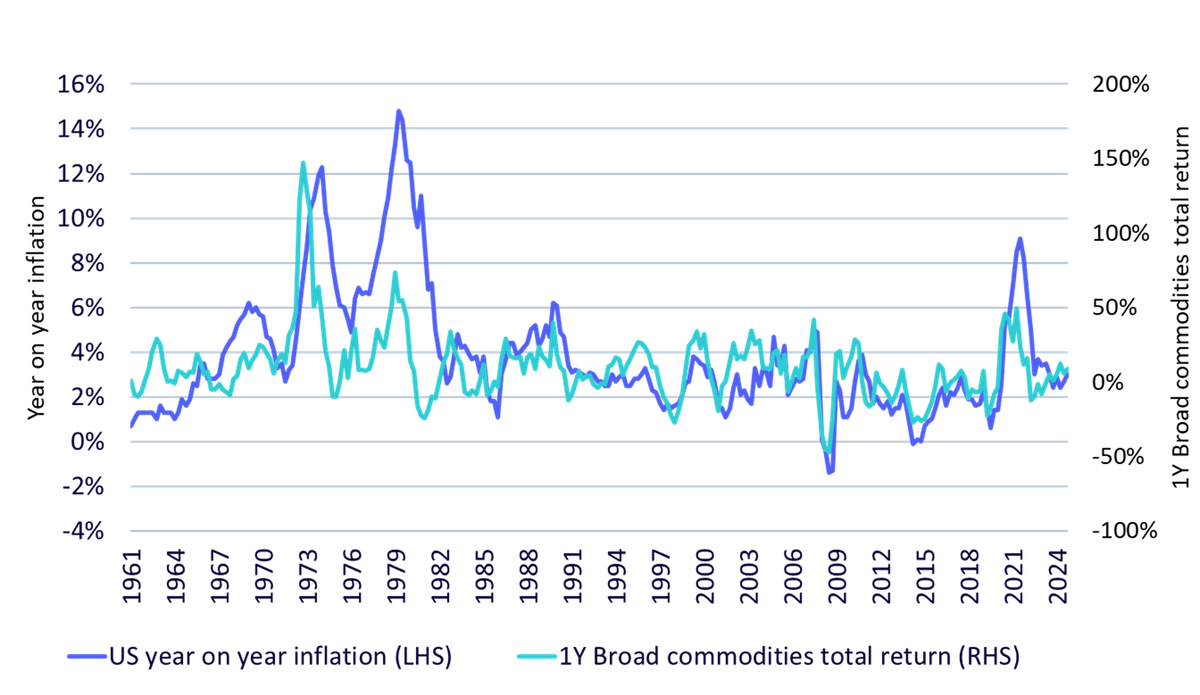

Commodities have historically exhibited a high sensitivity to inflation, reflecting their role as direct inputs into food, energy, and manufactured goods (Figure 3). As such, broad commodity benchmarks are commonly used within multi-asset portfolios seeking to preserve purchasing power.

However, the effectiveness of a commodity allocation as an inflation hedge depends not only on asset class exposure, but also on the representation of different commodities. Concentration in a small number of commodities or sectors can reduce alignment with the sources of inflation consumers experience.

By maintaining diversified exposure across energy, metals and agricultural commodities, and by systematically rebalancing weights based on economic production rather than price performance, broad benchmarks such as the Bloomberg Commodity Index are designed to remain aligned with inflation pressures as they emerge across the real economy.

Source: Bloomberg, from December 1960 to September 2025. Historical performance is not an indication of future performance, and any investments may go down in value. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

The addition of cocoa futures marginally broadens the index’s exposure to food-related price pressures. Food and beverages account for a meaningful share of consumer inflation baskets, making agricultural commodities an important, though often smaller, component of inflation-sensitive portfolios.

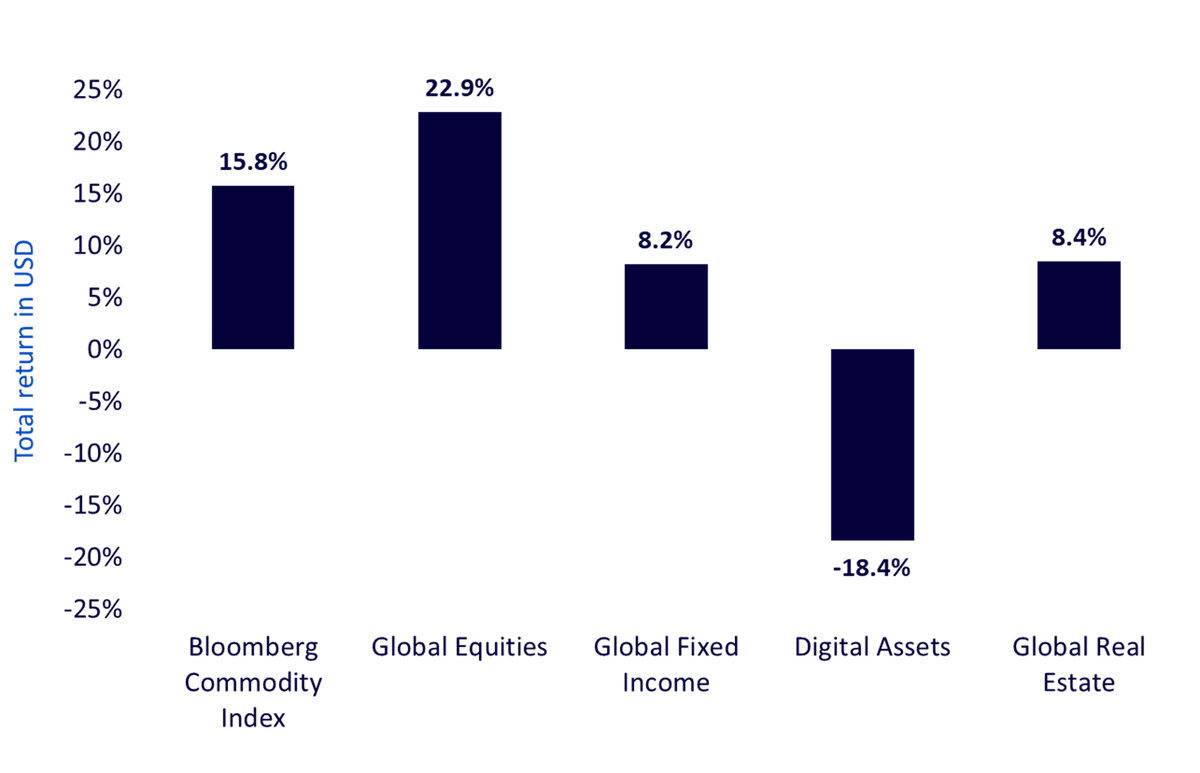

2025 was a strong year for commodities, outperforming many traditional and alternative assets (Figure 4). Precious metals were among the strongest-performing commodity segments, supported by falling real yields, sustained central bank demand for gold and periods of heightened policy and geopolitical uncertainty.

Source: Bloomberg, from 31 December 2024 to 31 December 2025 in USD, as total return. ‘Global Equities’ is the MSCI ACWI Gross Total Return USD Index, ‘Global Fixed Income’ is the Bloomberg Global-Aggregate Total Return Index Value Unhedged USD, ‘Digital Assets’ is the CoinDesk 20 Index, and ‘Global Real Estate’ is the FTSE EPRA Nareit Global REITs TR Index. Historical performance is not an indication of future performance, and any investments may go down in value.

Strong performance can amplify differences between benchmark exposure and implementation. While indices define economic exposure, the way that exposure is delivered can influence outcomes. Broad commodity ETFs typically rely on futures-based replication, which is often the only feasible approach for bulky or perishable commodities, but can introduce roll costs over time.

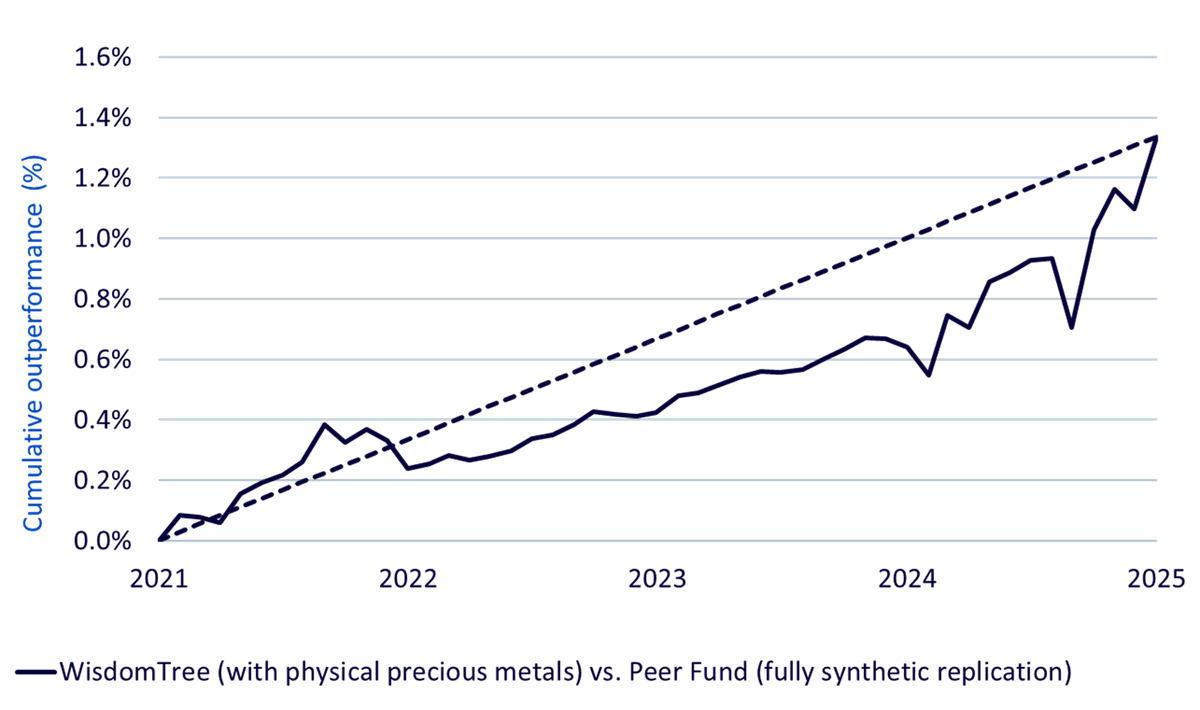

Where physical replication is possible, such as for precious metals like gold and silver, holding the underlying metal in physical form can affect performance (Figure 5). The WisdomTree Bloomberg Commodity UCITS ETF (PCOM) combines futures-based exposure with physically backed precious metals, reflecting how many investors access gold and silver individually. Over time, this implementation approach has contributed to performance differences relative to fully synthetic peers.

Source: WisdomTree, Bloomberg, from 31 December 2021 to 31 December 2025. The timeseries shows the difference in cumulative return of net asset values of the WisdomTree Broad Commodities UCITS ETF and a peer ETF tracking the same index in US Dollar. The dashed line visualises the historical trend as a linear function. Historical performance is not an indication of future performance, and any investments may go down in value.

The 2026 rebalancing of the Bloomberg Commodity Index demonstrates how a rules-based benchmark adjusts to changing market conditions through a consistent and transparent process. The inclusion of cocoa futures reflects observable developments in agricultural markets, while the reduction of performance-driven overweights shows the index’s focus on economically grounded exposures.

Beyond benchmark construction, the way commodity exposure is implemented can also matter, particularly during periods of strong market performance. Differences between futures-based and physical replication, especially in precious metals, can influence realised outcomes over time.

Taken together, these considerations highlight the importance of both index design and implementation in maintaining representative exposure to real-economy inputs and managing concentration across market cycles.

1 Association of Swiss Chocolate Manufacturers

2 Government of Netherlands’ Centre for the Promotion of Imports from developing countries (CBI), “What is the demand for cocoa on the European market?”

3 Source: Bloomberg, from 31/12/2024 – 31/12/2025 based on the respective Bloomberg Commodity Total Return Subindex. Historical performance is not an indication of future performance and any investments may go down in value.

Associate Director, Quantitative Research

Tobias Lazar is an Associate Director in WisdomTree’s Quantitative Research Team, where he focuses on developing innovative exchange-traded products across various asset classes and supporting WisdomTree’s diverse range of offerings. Before joining WisdomTree, he worked in the index research and development teams at Nasdaq and Solactive, where he was responsible for developing equity and alternative risk premia indices. Tobias holds an MSc in Financial Engineering from the University of Birmingham, UK, a BSc in Mathematics from the University of Cologne, and is a Chartered Alternative Investment Analyst (CAIA).