EEIE LN

WisdomTree Europe High Dividend UCITS ETF

Publié le 1 août 2025

The framework accord unveiled on 27 July between Washington and Brussels ends months of escalating rhetoric and removes the threat of an outright trans-Atlantic trade war. The US will levy a uniform 15% tariff on almost every European product line, while retaining the 50% surcharge on steel and aluminium that has been in force since 2023. Aircraft components, certain generic pharmaceuticals, a narrow list of chemicals, semiconductor-manufacturing equipment and a basket of critical raw materials will continue to enter duty-free. In exchange, the European Union (EU) has pledged to increase purchases of US natural gas and other fossil fuels by $750bn through 2028 and to channel a further US$600bn of investment into US projects. From an investor’s perspective the agreement delivers clarity, yet it also codifies a meaningfully higher cost of access to the EU’s most important external market.

Before last weekend our estimates assumed an effective US tariff rate near 12.5%, reflecting an informal 10% reciprocal rate coming on top of pre-existing tariffs, with specific rates for autos (27.5%), steel and aluminium (50%) and pharmaceuticals (exempted from reciprocal tariffs). Under the new schedule the mechanically calculated average jumps to roughly 15.7%. Once the Commission obtains definitive Harmonised Code (HS)- exemptions for the announced carve-outs, the effective rate should settle in a 12-15% corridor. That upper bound is still materially below the 30% across-the-board tariff threatened by the White House earlier in July, yet it represents a significant tightening of the screws on European exporters relative to the status quo ante.

Equity markets initially welcomed the détente. The Stoxx Europe 600 advanced as industrials and capital-goods names retraced part of the sell-off that followed July’s tariff salvos, while the euro firmed toward 1.14 against the dollar1. Investors correctly judged that a worst-case outcome had been avoided, but the economic cost cannot be ignored. Europe ships more than €500bn of goods to the US each year, equivalent to one-fifth of its extra-EU exports2.

Independent simulations by the European Central Bank (ECB) suggest that a 10% increase in the average tariff can reduce that flow by roughly a quarter within two years, subtracting around three-tenths of a percentage point from euro-area GDP. The burden will not be evenly distributed. Germany, Italy and Ireland are heavily exposed through autos, precision machinery and pharmaceuticals, while smaller open economies in Central and Eastern Europe feed the same supply chains and will feel indirect contagion.

Policy offsets are already on the table. Berlin’s decision to move ahead with a €500bn off-budget infrastructure and defence fund is poised to inject almost 2% of German GDP into the economy each year through 20353. That stimulus should cushion domestic demand and provide a pipeline of contracts for construction, engineering and technology suppliers across the single market. The ECB also retains scope to ease further. Headline inflation is holding close to target, core pressures are fading, and President Lagarde has indicated she will not prejudge the growth impact of the tariff deal until staff have completed a fresh projection round due in September. The policy mix of fiscal expansion in Germany and a patient central bank at euro-area level offers an important backstop while exporters adjust.

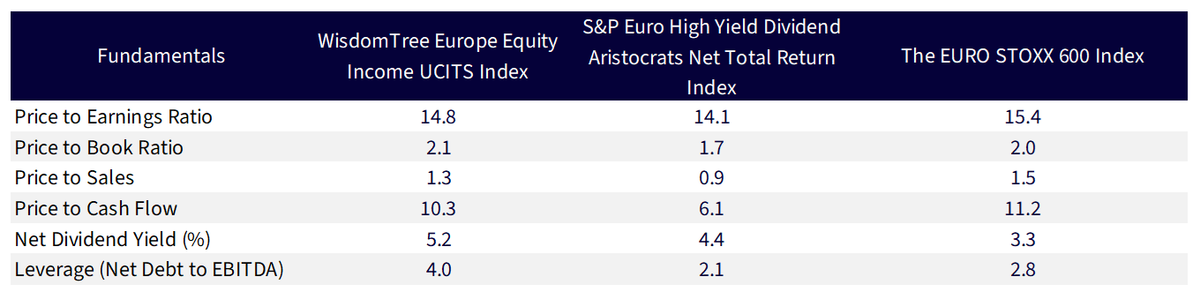

The WisdomTree Europe Equity Income UCITS ETF (Ticker: EEI) offers a compelling way to access Europe’s dividend payers at a time when value, income and policy resilience are taking centre stage. EEI tracks the price and yield performance of the WisdomTree Europe Equity Income Index (Ticker: WTEHYE). The Index’s dividend weighted strategy inherently favours value-oriented companies with consistent earnings and attractive yield profiles—attributes that not only support performance in volatile macro environments but also enforce valuation discipline over time. With a forward dividend yield above 5.2%4, the EEI provides a meaningful income stream in a period where real rates remain constrained and equity risk premiums outside the US look increasingly attractive.

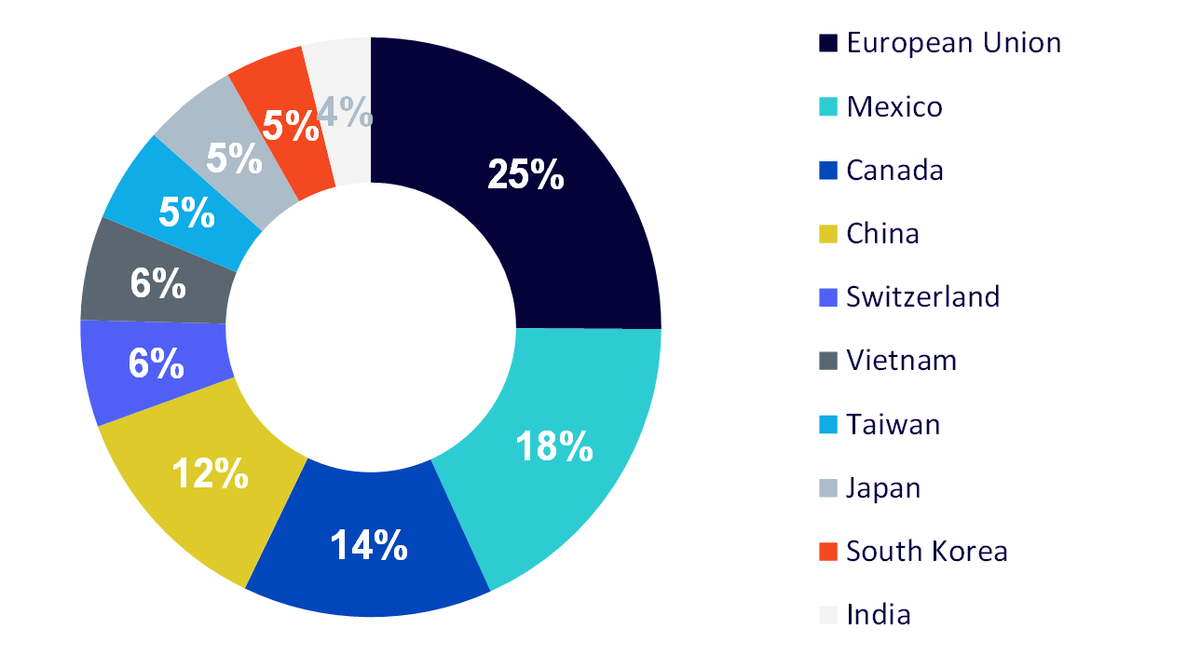

Importantly, EEI’s portfolio is well insulated from US trade policy risks, with only 9.4% weighted average revenue exposure to the US5. This makes it an appealing allocation for investors looking to reduce exposure to tariff-sensitive earnings streams and US policy uncertainty.

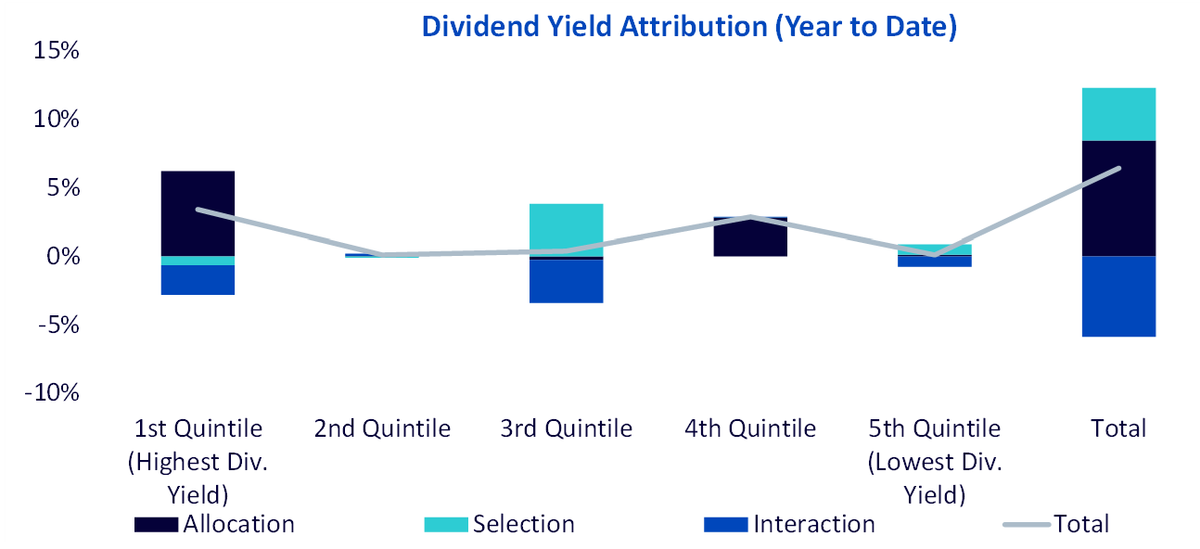

The Year-to-Date attribution between the WisdomTree Europe Equity Income Index and MSCI Europe Index highlight the importance of maintaining a higher tilt to the higher dividend yielding quintiles. The WisdomTree Europe Equity Income Index outperformed the MSCI Europe Index by 6.41% Year to Date with the biggest contribution of returns emanating from the highest dividend yielding quintile6.

Conclusion

The agreement buys time and removes the most severe downside tail, yet it codifies a new, higher cost of doing business across the Atlantic. Fiscal stimulus in Europe and a measured ECB stance will provide ballast, but investors must be selective. Concentrating on tariff-insulated themes—defence, domestically focused industrials and utilities offers the most robust way to navigate the changed US economic landscape and the evolving trade architecture.

1 Bloomberg from 28 July to 31 July 2025

2 Eurostat’s international-trade database

3 European Commission, Report on the Potential economic impact of the reform of Germany’s discal framework as of 19 May 2025

4 FactSet, WisdomTree as of 31 July 2025

5 FactSet, WisdomTree as of 30 June 2025

6 FactSet, WisdomTree as of 30 June 2025

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.