WCBR LN

WisdomTree Cybersecurity UCITS ETF - USD Acc

Publié le 12 juin 2024

Global Head of Research

Senior Associate, Quantitative Research and Multi Asset Solutions

Within WisdomTree’s suite of thematic equity strategies, both the WisdomTree Team8 Cybersecurity UCITS NTR Index (WTCBRN), tracked by WisdomTree Cybersecurity UCITS ETF (WCBR) and BVP Nasdaq Emerging Cloud NTR Index (EMCLOUDN), tracked by WisdomTree Cloud Computing UCITS ETF (WCLD) focus largely on Software-as-a-Service (SaaS) companies. There is an overall feeling of concern as we reach the halfway mark in 2024, as we are receiving questions from investors and seeing a range of articles discussing the slowing growth rates in these types of stocks.

Index | Ticker | YTD | 1-year | 3-year | 5-year | 10-year | Since fund inception |

|---|---|---|---|---|---|---|---|

WisdomTree Team8 Cybersecurity UCITS Index (NTR) | WTCBRN | -8.25% | 16.64% | 1.20% | - | - | 8.02% |

BVP Nasdaq Emerging Cloud Index (NTR) | EMCLOUDN | -12.65% | 0.48% | -14.56% | 4.58% | 19.95% | 19.32% |

Source: WisdomTree, Bloomberg, as of 31 May 2024. Calculation is based on returns in USD. Return figures for time periods longer than 1 year are annualised. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

Upon examining the historical returns, what is immediately noticeable is a quantification of the so-called SaaS return rollercoaster:

There is no way to isolate a singular cause for share prices moving in different ways at different times, but if we step back and consider what has characterised asset price behaviour from January 2021, one macroeconomic variable has dominated above all others.

In what follows, we quantify this thinking using illustrations from the historical data.

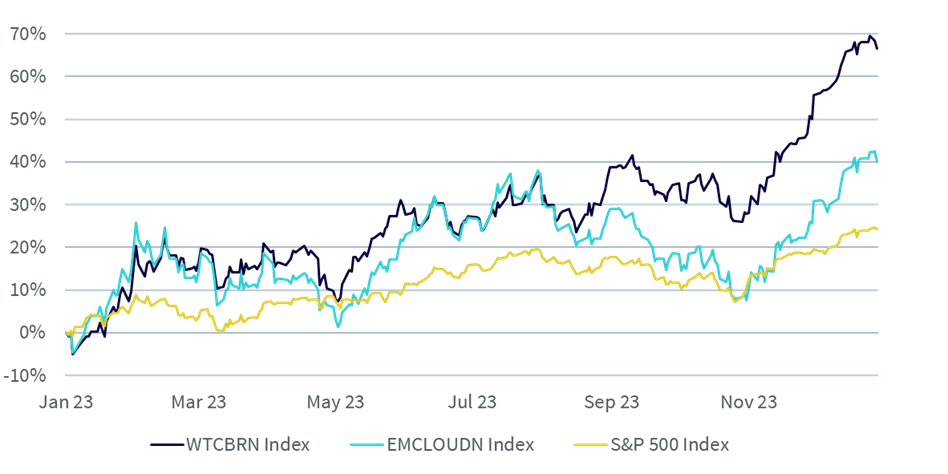

In Figure 2, many may not directly remember that WTCBRN was up almost 70% during 2023 since the character of returns observed in 2024 has been very different. EMCLOUDN was only up about 40%. Both of these strategies dramatically outperformed the S&P 500 Index during 2023.

What’s clear is that most of this outperformance came during the last two months of 2023, so we must zoom in there.

Source: WisdomTree, Bloomberg. Daily data from 02 January 2023 to 29 December 2023. Calculations are based on returns in USD. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

In Figure 3, we focus on the period from 31 October 2023 to 31 December 2023. Both WTCBRN and EMCLOUDN were up roughly 30%. We cannot say that this move was solely due to expectations of lower interest rates, but we can say that it was a major factor that created a risk of mispricing if the path of interest rates was going to stay higher for longer.

Source: WisdomTree, Bloomberg. Daily data from 31 October 2023 to 29 December 2023. Calculations are based on returns in USD. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

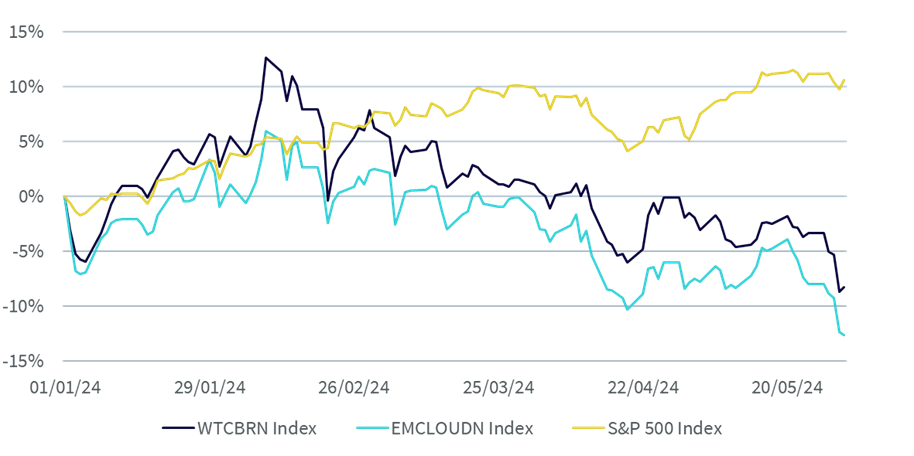

In Figure 4, we see the challenge faced by WTCBRN and EMCLOUDN in 2024. Now, most of the underlying constituent companies are growing revenues, year-over-year, above 10%. Some are growing revenues above 20% or even above 30%. However, the growth is not accelerating, and investors are not getting anywhere near as excited as they might have been in 2020 or 2021. In short, the growth we are experiencing is not enough to cancel out the negative impact on valuations of higher-for-longer interest rates2.

WTCBRN and EMCLOUDN are underperforming the S&P 500 Index, but we’d caution against benchmarking these rather narrow, high-volatility strategies against such a broad benchmark since we expect the return experience to always be dramatically different.

We believe that, with the higher risk of WTCBRN and EMCLOUDN, the time horizon needs to be extended. Anyone who needs to focus heavily on the 2024 performance results in a portfolio may face a significant risk of a negative return contribution from these strategies.

Source: WisdomTree, Bloomberg. Daily data from 01 January 2024 to 31 May 2024. Calculations are based on returns in USD. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

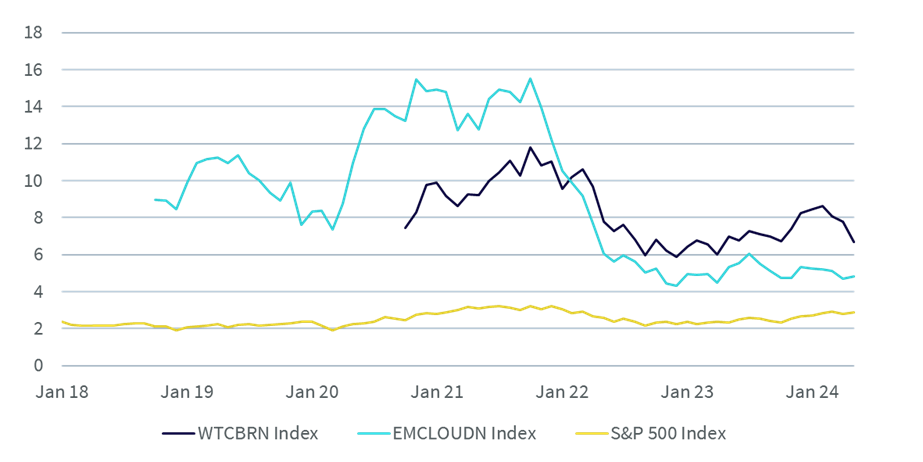

WTCBRN and EMCLOUDN are also ‘expensive’ from a valuation perspective. However, Figure 5 shows valuations were significantly higher in 2021 when interest rates were at or near zero. The massive rallies in WTCBRN and EMCLOUDN at the end of 2023 were likely largely driven by interest rate expectations. However, interest rate expectations can change and are independent of company results. Maybe it is accurate to indicate that, as we started 2024, these stocks, in many cases, were too expensive If the US Federal Reserve was not going to cut its policy rate quite quickly.

Source: WisdomTree, Bloomberg. Monthly data as of 31 May 2024. Trailing 12-months Sales data applied. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

Now, anytime software companies are in focus, we caution investors to look at valuation without looking at growth. Figures 6a and 6b indicate measures of both sales growth and EBITDA3 growth, examined from both a median and a weighted average basis.

Median sales growth | |||||||

|---|---|---|---|---|---|---|---|

Index | Ticker | 1-year | 3-year | 5-year | 1-year | 3-year | 5-year |

WisdomTree Team8 Cybersecurity UCITS Index (NTR) | WTCBRN | 16.5% | 20.7% | 15.9% | 21.4% | 26.0% | 20.9% |

BVP Nasdaq Emerging Cloud Index (NTR) | EMCLOUDN | 20.0% | 26.5% | 25.5% | 20.5% | 26.8% | 26.8% |

S&P 500 Index | SPX | 4.6% | 6.4% | 6.4% | 11.6% | 15.4% | 12.5% |

Source: WisdomTree, FactSet as of 31 May 2024. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

Median EBITDA growth | |||||||

|---|---|---|---|---|---|---|---|

Index | Ticker | 1-year | 3-year | 5-year | 1-year | 3-year | 5-year |

WisdomTree Team8 Cybersecurity UCITS Index (NTR) | WTCBRN | 21% | 45% | 25% | 34% | 102% | 94% |

BVP Nasdaq Emerging Cloud Index (NTR) | EMCLOUDN | 38% | 169% | 104% | 49% | 121% | 114% |

S&P 500 Index | SPX | 6% | 9% | 7% | 25% | 19% | 17% |

Source: WisdomTree, FactSet, as of 31 May 2024. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

There’s a large divergence between what the world thinks about the themes of cybersecurity and cloud computing through their actions and the share price performance of the companies within WTCBRN and EMCLOUDN.

As we adopt more AI, we will also need more cybersecurity. AI is a tool that can be used in both negative ways and positive ways. The higher the level of adoption, the more security is required.

We don’t know which cybersecurity companies will be the long-term winners, which is why we like a basket and ETF approach.

Nvidia is getting the lion’s share of attention in the technology space. If we think about who is buying the chips, it is the companies that offer the largest public cloud computing infrastructure. The world is spending hundreds of billions of dollars over a period of years to build more compute infrastructure in the cloud than we have ever had. However, we do not know yet which companies will be the long-term winners based on what they are using AI to do.

This divergence from the theme's potential and the current share price performance signals a time to invest over the long term. With big technology shifts, very little happens in the earlier years of the transition. However, in the later years, the compounding effect of the growth can be quite large. Volatility will likely remain quite high, but if we follow the spending, the world loves and needs both cybersecurity and cloud computing.

Fundamentals | WisdomTree Team8 Cybersecurity UCITS Index (NTR) | BVP Nasdaq Emerging Cloud Index (NTR) |

|---|---|---|

Ticker | WTCBRN | EMCLOUDN |

Price to sales ratio | 6.7x | 4.8x |

Price to book ratio | 7.0x | 5.8x |

Price to cash flow ratio | 29.6x | 29.8x |

Est. price to earning ratio | 38.1x | 31.7x |

Est. price to earning ratio (excluding firms with negative earnings) | 36.8x | 29.5x |

% of firms with negative earnings | 41.9% | 62.0% |

Sources: WisdomTree, FactSet, as of 31 May 2024. You cannot invest directly in an index. Historical performance is not an indication of future results and any investments may go down in value.

1 Specific period of calculation: 04 January 2021 to 31 May 2024.

2 Growth rates are sourced from Bloomberg and represent the year-over-year sales growth of the most recent quarterly financial report of the respective constituents within WTCBRN or EMCLOUDN, available as of May 31, 2024.

3 EBITDA stands for Earnings before Interest, Taxes, Depreciation and Amortization and allows investors to go down the income statement and get closer to a measure of ‘Operating Earnings.’

Global Head of Research

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.

Senior Associate, Quantitative Research and Multi Asset Solutions

Baoqi Zhu joined WisdomTree in 2023 as a Senior Associate on the Research team. Baoqi focuses on quantitative research on thematic equity indices and portfolio solutions. Prior to WisdomTree, Baoqi spent over two years at Ernst & Young (EY) in their Quantitative Advisory Services, where he was involved in the research and development of quantitative risk models. Earlier in his career, Baoqi served as a quantitative analyst within a multi-asset structuring team at Maven Global for more than three years. His responsibilities included designing and optimising bespoke hedging strategies based on derivatives. Baoqi holds a MSc in Financial Engineering & Risk Management from Imperial College London and a BSc in Actuarial Science from Nankai University, China. He is also a certified Financial Risk Manager (FRM).