Trade war portfolio protection? Consider small caps for domestic exposure

Publié le 20 avril 2018

Global Head of Research

On an intra-day basis, some of the recent market movements have been nothing short of staggering. Depending on the news on trade wars or conflict in the Middle East, equity markets have opened either up or down by hundreds of points, and intra-day market reversals have been just as dramatic.

Clearly, geopolitical risk is shaping intra-day equity volatility.

Protection Through Small Caps

As investors, we have attempted to understand the current uncertainty. We can’t say for sure, at this stage, whether or not there will be a global trade war. Pressure, whether between the U.S. and China or regarding certain negotiations, like NAFTA, has ebbed and flowed during President Trump’s administration. However, what is clear at this point is that the uncertainty is impacting global equities on a daily basis.

For those looking to maintain their long-term allocations to equities, it may be helpful to know that there are segments of the equity market that are less affected by the current issues. Small cap stocks, many of which are less global and more domestically-focused, may offer investors more protection from the stock market volatility. The chart below shows how small caps across the world tend to export less than their large cap peers on a regional basis.

For those looking to maintain their long-term allocations to equities, it may be helpful to know that there are segments of the equity market that are less affected by the current issues. Small cap stocks, many of which are less global and more domestically-focused, may offer investors more protection from the stock market volatility. The chart below shows how small caps across the world tend to export less than their large cap peers on a regional basis.

Local revenue vs global revenue for small cap companies on a regional basis

Source: Factset. Data is as of date specified. Japan is lagged one-month due to data availability. Past performance is not indicative of future results. You cannot invest directly in an Index.

Europe offers the greatest contrast, in that companies within the WisdomTree Europe SmallCap Dividend Index generate almost twice the weighted average revenue from within Europe as companies within the large cap focused MSCI Europe Index do. This suggests that if investors have a desire to allocate to Europe but wish to invest in non-exporters, one approach is to focus on small cap equities. It’s also important to make the connection to currency performance, as export-oriented firms tend to benefit when their home currency weakens, and their goods and services become less expensive in their targeted markets abroad. Over the last 12 months1, the euro appreciated 16.2% against the U.S. dollar and the British pound appreciated 13.9% against the U.S. dollar. Whether one is thinking of non-exporters from a geopolitical or a currency perspective, small caps might be of interest.

Shifting to Japan, with the yen appreciating, many investors have been uncertain of late as to the best way to invest in Japanese equities, given that Japan’s equity market is negatively correlated to movements in the yen. Put simply—if the yen is rising, Japan’s stock market tends to fall in value - and vice versa. Small cap Japanese companies, shown here through the WisdomTree Japan SmallCap Dividend Index, derive more than 80% of their weighted average revenue inside Japan. If investors want to try to side-step the yen’s movements and benefit from growth within Japan, small caps can create the potential opportunity.

Emerging markets exhibit the smallest difference when comparing the weighted average revenue distribution of smaller companies to larger companies, but companies within the WisdomTree Emerging Markets SmallCap Dividend Index did still, in fact, derive a greater degree of local revenue than companies in the MSCI Emerging Markets Index. As emerging market companies grow and develop more global familiarity, there could be a greater chance to obtain enhanced entrepreneurial sensitivity within this space.

U.S. small caps have been in focus since President Trump’s 2016 election victory. They were clearly in favor during late 2016 as it was assumed that a Republican victory would result in corporate tax reform. This segment of the market began to lag slightly in 2017 as the corporate tax outcome became less certain, but it is notable that U.S. small caps do derive a higher proportion of revenues from inside the U.S. and therefore have greater potential for earnings growth now that corporate tax rates have been lowered.

Impact on performance

To this point, it’s clear that there may be a logical basis for considering the domestic sensitivity of small cap companies. While each region above has unique attributes, there are also some overarching commonalities. Yet, the most critical question is whether the small cap indexes that we’ve discussed deliver distinctly different performance?

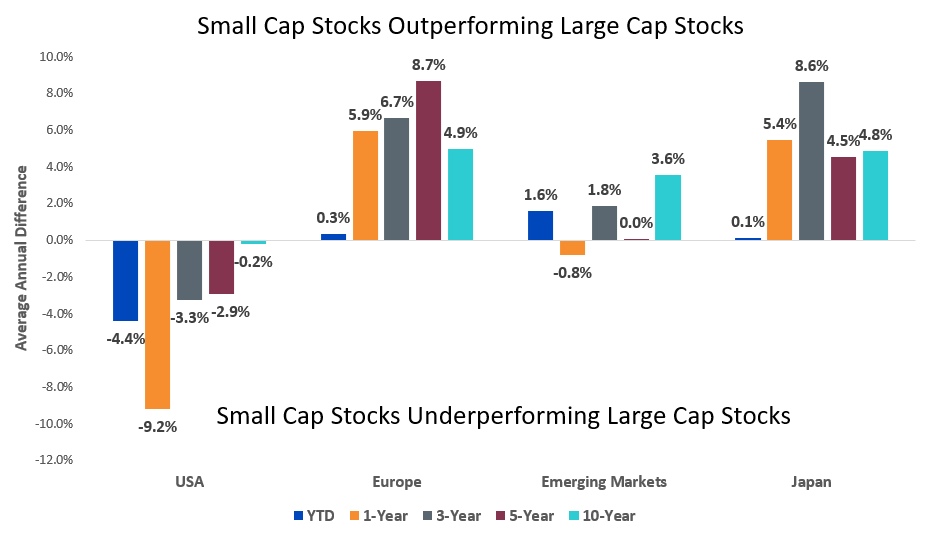

Small cap performance on a regional basis

Source: Bloomberg. Data is as of 31 Mar. 2018. Past performance is not indicative of future results. You cannot invest directly in an Index. USA refers to the difference in average annual returns of the WisdomTree U.S. SmallCap Dividend Index and the S&P 500 Index. Europe refers to the difference in average annual returns of the WisdomTree Europe SmallCap Dividend Index and the MSCI Europe Index, with returns measured in euro terms. Emerging Markets refers to the difference in average annual returns between the WisdomTree Emerging Markets SmallCap Dividend Index and the MSCI Emerging Markets Index. Japan refers to the difference in average annual returns between the WisdomTree Japan SmallCap Dividend Index and the MSCI Japan Index.

The chart above shows that small cap stocks have underperformed in the U.S. over several time horizons but outperformed in Europe, Japan and the emerging markets. The U.S. comparison clearly exhibits a distinct difference to the other global regions shown, in that small caps underperformed large caps over each period. On a one-year basis, the comparison was particularly challenging. One factor to consider here relates to what we noted earlier - many global currencies have been strengthening significantly against the U.S. dollar over the past year. This has created a nice tailwind for U.S. large-cap multinational exporters, but since small cap companies don’t export to anywhere near the same extent, it isn’t something that has impacted them to an equivalent degree.

Additionally, the strong performance of large cap U.S. equities exhibiting sensitivity to momentum as a factor, leading the industry and media to create acronyms like F-A-N-G (Facebook-Amazon-Netflix-Google) has also contributed to the large cap performance advantage.

Conclusion: small caps provide an interesting way to differentiate portfolio exposure

It is difficult to say whether the issue of trade wars will stay at the forefront of the global investment news cycle over the coming months. However, we believe that the real insight here is that when considering portfolio exposure and asset allocation, geographical revenue differences should not be ignored.

1 Source: WisdomTree, Bloomberg, from 13/04/2017 - 13/04/18/2018.

You may also be interested in reading…

Catégories

À propos du contributeur

Global Head of Research

Christopher Gannatti dirige l’équipe de recherche mondiale de WisdomTree, apportant sa riche expérience à l’entreprise. Depuis son arrivée en décembre 2010, Chris a progressé dans l’organisation avant d’en assumer la direction en 2021. Dans le cadre de sa mission mondiale, Chris joue un rôle crucial dans la conception des initiatives de WisdomTree aux États-Unis et en Europe. Son expertise repose sur les actions et les thématiques technologiques, en accordant une attention particulière à la mise en récit et aux analyses stratégiques. Basé aux États-Unis, il travaille en étroite collaboration avec Jeremy Schwartz, Directeur mondial des investissements. Avant de rejoindre WisdomTree, Chris a travaillé chez Lord Abbett en tant que consultant régional, en collaboration avec des conseillers financiers basés dans la région du Midwest. Il est titulaire d’un diplôme en économie de l’université Colgate et d’un MBA de la NYU Stern School of Business, avec des spécialisations en finance quantitative, comptabilité et économie. Il possède également la certification CFA. Chris est un véritable visionnaire, reconnu pour son leadership éclairé et sa capacité à expliquer efficacement des stratégies complexes.