BRNT LN

WisdomTree Brent Crude Oil

Publié le 16 août 2024

Source: WisdomTree, Commodity Futures Trading Commission (CFTC), Bloomberg, Latest CFTC positioning data as of 06 August 2024. Historical performance is not an indication of future performance and any investments may go down in value.

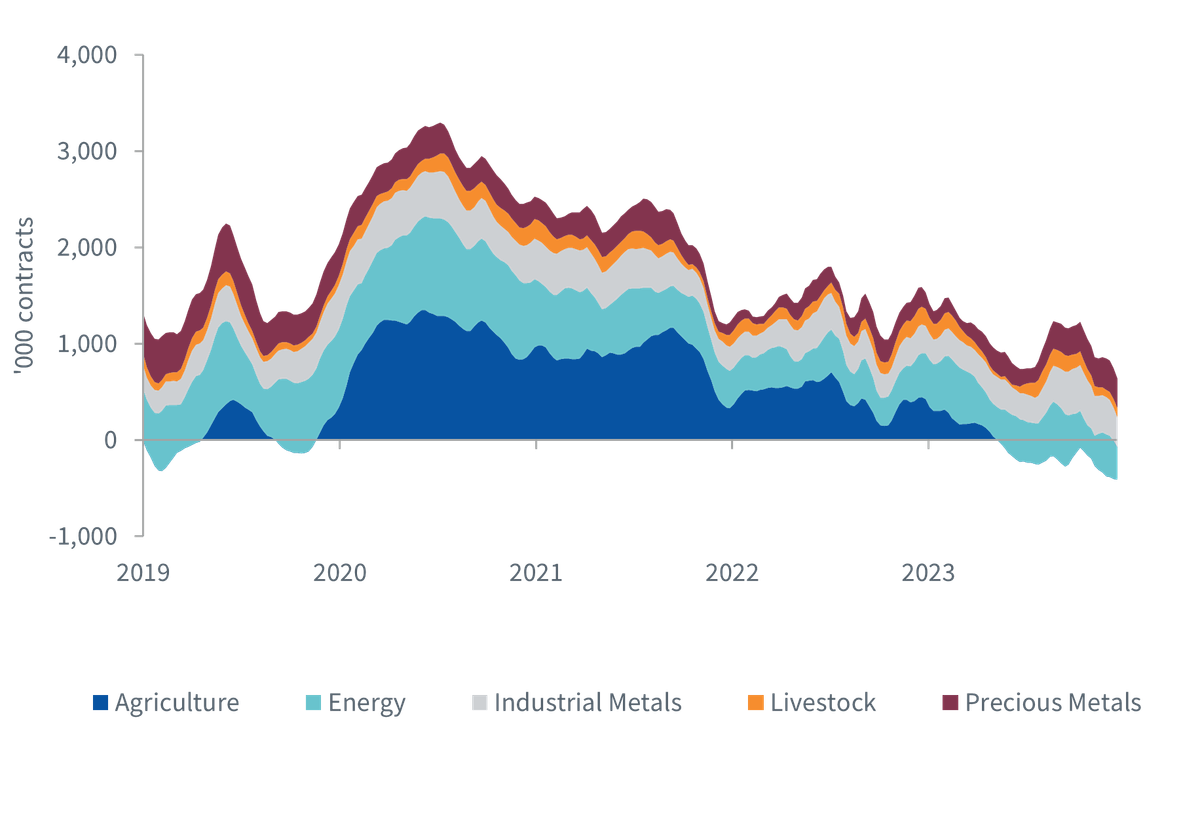

Investor sentiment in commodity markets appears to have reached an extreme level of bearishness, with net speculative positioning on commodity futures at its lowest point in five years. This pessimistic stance has been shaped by several factors, including recent market volatility and ongoing economic concerns. However, this level of bearishness may be overstated, creating potential opportunities for contrarian investors, both tactically and strategically. In this blog, we’ll explore the main subsectors of the commodities market—industrial metals, energy, precious metals, and agricultural commodities—to assess whether this is an inflection point and what might come next.

Industrial metals have faced significant headwinds recently, driven largely by weak sentiment toward China. Concerns about the country’s economic slowdown, particularly in manufacturing, have weighed heavily on the sector. Additionally, the global trend of higher interest rates has further dampened sentiment towards industrial metals, as higher borrowing costs slow down investment in infrastructure and manufacturing. Another factor contributing to the bearish sentiment is the perception of ample supply in the short-term, with rising inventories on exchanges suggesting that physical supplies are abundant.

Despite these challenges, there are strong structural tailwinds that the market seems to be overlooking. The global push toward energy transition and decarbonisation will require a massive increase in the production of industrial metals like copper, nickel, and aluminium. As the world ramps up investment in renewable energy, electric vehicles, and battery storage, demand for these metals is expected to rise significantly. This long-term narrative is not currently priced into the market, making industrial metals an attractive opportunity for investors who are willing to look beyond the short-term noise. The current bearish positioning could thus set the stage for a significant rebound as the energy transition narrative gains traction.

The energy sector, particularly oil markets, has been characterised by significant volatility in recent months. Oil prices have fluctuated broadly within a range of $70-90 per barrel, influenced by a complex mix of factors. Concerns about an impending recession in the US led to a sharp decline in prices in July and early August. However, this was followed by a rebound in mid-August as equity markets recovered and geopolitical tensions in the Middle East resurfaced.

Despite these fluctuations, the International Energy Agency expects demand growth to be just under 1 million barrels per day (mb/d) in both 2024 and 2025, considerably below last year’s 2.1mb/d growth, but not necessarily alarming. The current low level of speculative positioning in energy markets, exacerbated by recent volatility, suggests that investors may be overly pessimistic. For contrarian investors, this could represent a tactical buying opportunity, particularly as oil prices have recently approached the lower end of their trading range before rebounding. If supply struggles to keep pace with demand, especially during peak periods, we could see another upward shift in prices, potentially catching the bears off-guard.

Unlike other commodity sectors, net speculative positioning in precious metals has remained relatively stable, hovering around its five-year average. Gold has shown resilience, supported by strong central bank buying, most notably by the People’s Bank of China (PBOC). This demand has helped gold maintain its strength despite headwinds from delayed rate cuts, which have put upward pressure on Treasury yields and strengthened the U.S. dollar—both typically negative factors for gold.

Looking ahead, several factors could further boost gold’s appeal. As the Federal Reserve eventually shifts to cutting interest rates, geopolitical tensions persist, and uncertainties around global trade continue, demand for gold is likely to increase. Moreover, if investors in exchange-traded products (ETPs), who have not fully participated in the recent rally, begin to increase their exposure to gold, we could see additional upward momentum in the sector. For investors seeking a hedge against economic and geopolitical risks, gold remains a compelling option.

Among all the commodity subsectors, agricultural commodities have seen the steepest decline in net speculative positioning, reaching their lowest level in five years. In recent years, agricultural commodities have often experienced strong rallies due to various disruptive events, including the COVID-19 pandemic, the Russia-Ukraine conflict, and extreme weather patterns like El Niño and La Niña. These events have led to significant physical disruptions in supply chains, contributing to supply shortages in agricultural markets.

The current extreme low in positioning suggests that the market may be underestimating potential risks on the horizon. Agricultural commodities are particularly vulnerable to sudden disruptions, whether due to geopolitical events, climate change, or unexpected shifts in supply and demand dynamics. With the market seemingly disregarding these risks, there could be a sharp reversal in sentiment if any of these potential disruptions materialise. For investors, the current bearish positioning in agricultural commodities may present a unique opportunity to capitalise on an underappreciated sector.

While commodities have experienced a wave of bearish sentiment, reflected in the lowest net speculative positioning in five years, this extreme pessimism may be overdone. Each subsector—industrial metals, energy, precious metals, and agricultural commodities—presents unique opportunities that could lead to an inflection point in the market. As history has shown, periods of extreme bearishness can sometimes precede significant rebounds, and contrarian investors may find attractive entry points in the current market environment. Whether this marks the start of another commodity supercycle or simply a cyclical upturn remains to be seen, but the potential for a shift in sentiment is certainly worth considering.

Director, Research

@MobeenTahirWTMobeen is a member of WisdomTree’s research team where he focuses on a wide range of asset classes to offer strategic and tactical insights to our clients on global markets and investment products. Before joining WisdomTree in December 2018, Mobeen worked at Willis Towers Watson as an investment consultant advising institutional clients as well as their in-house fund business on asset allocation and portfolio construction with his research focus being equity and multi-asset smart beta. Mobeen has a BSc (Hons) in Accounting and Financial Management from Loughborough University and an MSc in Accounting and Finance from the London School of Economics and Political Science. He is also a CFA Charterholder.