Energise your portfolio with battery technology

Publié le 16 juillet 2018

The auto industry is at a turning point. As the Internal Combustion Engine (ICE) age slowly gives way to the next generation of automobiles, we expect to see a material impact on the demand for new metals utilised in batteries of electric vehicles (EV). The dangerous rise of carbon emissions coupled with greater energy efficiency driven by the evolution of battery technology is building momentum towards acceptance of EVs globally.

There is no doubt that the proliferation of EVs will be closely tied to the initiatives and support provided by governments across the world as they rely heavily on supplementary grid infrastructure. Macroeconomic factors such as the price of oil will also have a role to play in the continued growth of EVs.

Until the total cost of owning an EV remains greater than a conventional vehicle due to higher battery costs, we expect government support to play a key role in the shift towards EVs. The adoption of initiatives in support of EVs by governments across US, China and EU are sending clear signals to automakers who are starting to shift production lines in the direction of electrification. To name a few:

- Norway has led the surge by committing to end the sale of gas and diesel vehicles by 2025, followed by India in 2030 and Britain and France in 2040.

- California’s zero-emissions vehicle programme is by itself a policy that would grant support for greater demand of EVs in the US.

- China’s government issued a New Energy Vehicle (NEV) credit mandate that takes effect this year, setting out a minimum requirement for the car industry for production of new energy vehicles with some flexibility offered through a credit trading mechanism.

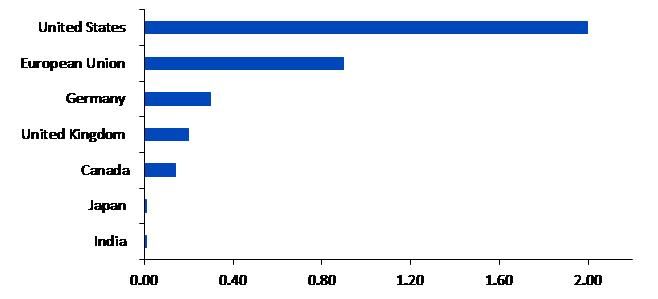

Figure 1: Investment announcements for EV infrastructure development in selected countries (Billion USD)

Source: International Energy Agency (IEA), WisdomTree, data available as of close 28 June 2018

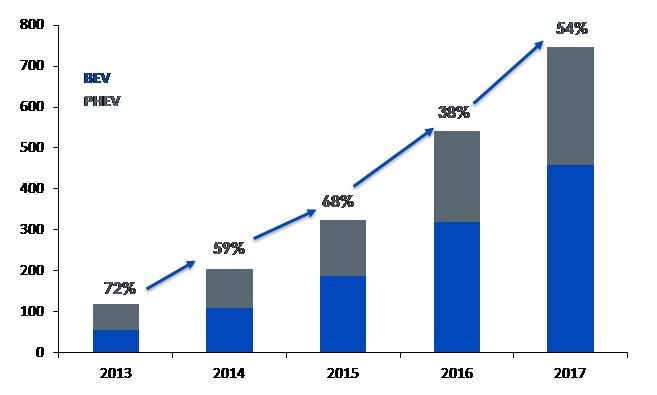

Mass adoption of EVs begins to unfold

In 2017 sales of global passenger EVs surpassed the 1-million-unit mark, posting a 54% increase over the year before,1 higher than the previous annual growth rate of 38% in 2016. China accounted for nearly 50% of global sales of EVs, representing a market share of 2.2% in 2017. The International Energy Agency (IEA) has doubled its central forecast for EVs, raising its 2030 EV fleet size estimate to 58mn from 23mn.

Closely mirroring the growth of charging infrastructure, sales of pure Battery Electric Vehicles (BEVs) were up 63% leading the pack, ahead of Plug-in Hybrid Electric Vehicles (PHEVs) that rose 40% in 2017. BEVs are powered solely by an electric motor, using electricity stored in an on-board battery, that needs to be charged regularly. In contrast, PHEVs are powered by a combination of an electric motor and an ICE that are designed to work in unison or separately.

The on-board battery can be charged from the grid, while the ICE supports the electric motor when higher operating power is required, or the battery’s power is low. BEVs are known to have the highest efficiency and have the great environmental benefits when powered by electricity from renewable sources.

Figure 2: Global Electric Passenger Vehicle Market (Million vehicles)

Source: International Energy Agency, WisdomTree, data available as of close 27 June 2018

Adoption of EVs stoking demand for metals

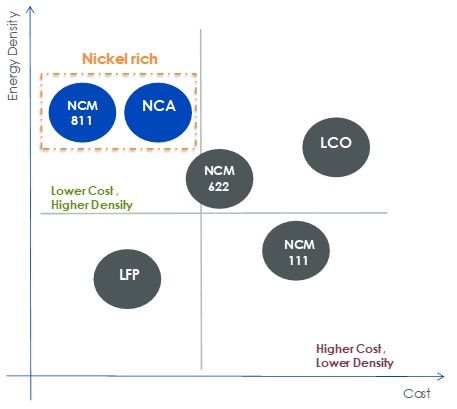

The rising pace of EV adoption is paving the way for increased demand for new metals such as nickel, lithium, cobalt, copper and aluminium. Lithium-ion batteries comprise a family of battery chemistries that employ various combinations of anode and cathode materials. The lithium-ion technologies can be compared along six dimensions: cost, safety, specific power, specific energy, performance and life-span. Currently the lithium Nickel-Manganese-Cobalt (NMC) is the most prominent technology for automotive applications. Rapid technology advances in battery chemistry is shifting to a higher proportion of nickel. While the NMC battery typically contained equal portions (1-1-1) of nickel, manganese and cobalt, the optimal ratio is now considered to be (8-1-1), thereby demanding higher percentage of nickel. This combination has provided the added advantage of lower costs and higher energy densities, although it comes at the cost of lower voltage.

Figure 3: Battery chemistry favours more nickel and less cobalt

Source: Vale, WisdomTree, data available as of close 27 June 2018, Lithium Battery abbreviations: NCM- Nickel Manganese Cobalt ; NCA- Nickel Cobalt Aluminium ; LCO- Lithium cobalt ; LFP – Lithium iron phosphate

While demand for nickel, cobalt and lithium is projected to rise, more traditional commodities such as copper and aluminium are poised to benefit from burgeoning EV industry. Aluminium, known for its light weight, helps reduce the weight of the vehicle considerably in comparison to steel. The decrease in the car’s total weight will reduce its energy consumption by nearly 8%, thereby improving its energy efficiency. An average electric car requires 80 to 90 kilograms of copper compared to the 25 kilograms for a conventional passenger car. Copper demand has been forecasted to witness a nine-fold increase from EVs2. The potential rise in demand stems from the elevated levels of copper windings in EVs compared to the ICE and growing infrastructure requirements.

1 Source: International Energy Agency 2018

2 Source: The International Copper Association

À propos du contributeur

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.