DXJ LN

WisdomTree Japan Equity UCITS ETF - USD Hedged

Veröffentlicht am 6. Oktober 2025

Sanae Takaichi has won the leadership of the Liberal Democratic Party (LDP). Her election marks a historic turning point in Japanese politics as the LDP’s first female president. The symbolism and characterisation as Abe 2.0 is powerful, yet markets care more about the mandate and policies that follow. The LDP has lost its majorities in both chambers, so the new leader must build bridges across a fragmented Diet, steady household confidence and convince a younger electorate that policy can deliver.

The election results add an important fiscal angle. Takaichi has signalled an active use of the budget while promising responsibility. She has discussed a flat tax programme that can lower rates to 10% -- something that would boost consumption. She advocates strengthening Japan’s semiconductor industry as part of her economic security agenda, which should benefit tech exporters via policy support alongside a weaken Yen.

The early expectation is for front loaded package that leans into public investment, energy security and defence. If that is the mix, the curve is likely to steepen, long term yields drift higher, and equities are poised to welcome the growth impulse. The risk is that a thin governing margin forces political compromise, yet the direction of travel points to a modestly larger fiscal footprint that tries to put real income back into households without derailing the disinflation path now under way.

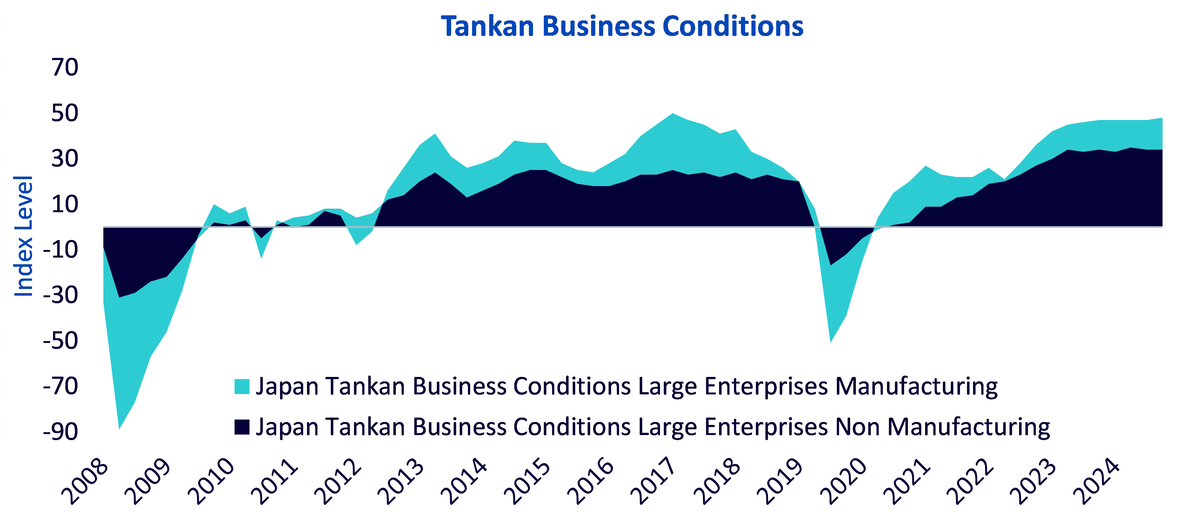

The political context matters because the economic backdrop is better than the headlines suggest. The latest Tankan survey showed a gentle but broad pulse. Large manufacturers lifted their diffusion index to +14 in Q3 from +13 as illustrated in the chart. Large non-manufacturers held constant at +34. Medium sized factories rose to +12 and small producers stayed just above water at +1. That pattern suggests domestic demand is firm enough to offset some external stress. It also says pricing power is not confined to a few export champions. Services remain resilient, even if hospitality had a soft patch during the heat of summer.

Source: Bloomberg, WisdomTree as of 30 September 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Trade policy has also moved from existential threat to manageable constraint. Tokyo and Washington have largely wrapped up a trade deal that caps auto tariffs at 15% rather than the original 25%. That is still a headwind for margins in parts of the value chain, yet the worst case has receded. Japanese manufacturers have long since diversified production. Automakers assemble most North American sales inside the region. Industry data shows that 70% of Japanese-brand vehicles sold in the US are made in North America1. Machinery and electrical firms have meaningful footprints across Association of the Southeast Asian Nations (ASEAN) and Europe. According to the latest Asia and Oceania survey, 71.5% of Japanese manufacturers developed new suppliers over the past 5 years2. When tariffs change, production schedules change with them.

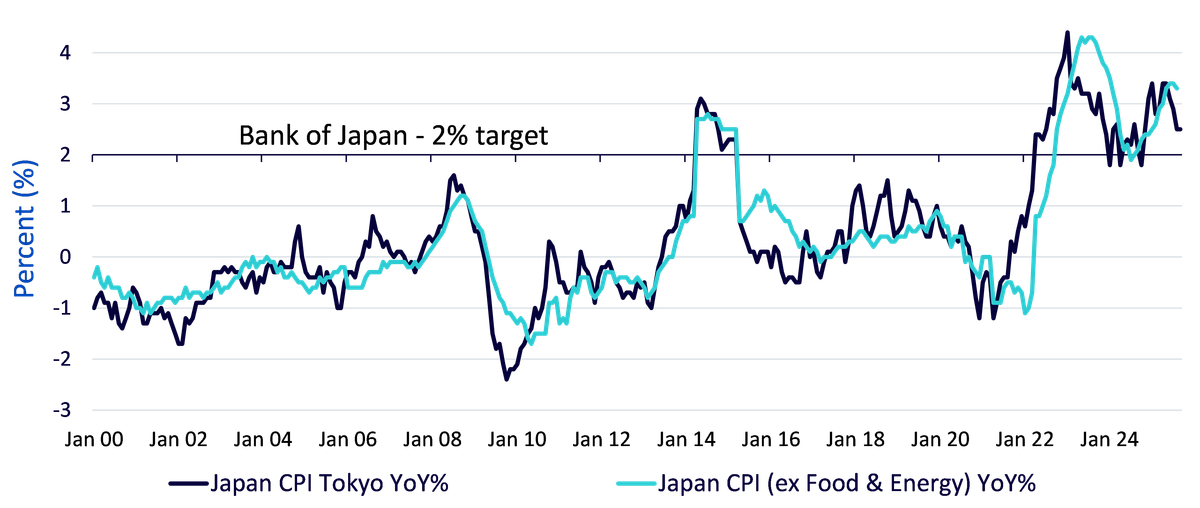

Monetary policy sits in the middle of this story. Governor Ueda has kept his options open. Inflation has been above the target since October 2022, yet the Bank of Japan (BOJ) wants more evidence that the underlying trend is sustained by wages and demand.

Source: Bloomberg, WisdomTree as of 30 September 2025. Historical performance is not an indication of future performance and any investments may go down in value.

The Osaka speech3 reminded markets that the Board will move if the baseline for activity and prices is realised, while giving no explicit timing. The odds of an October rate hike have risen. The cross currents are well known. The BOJ would prefer not to hike into a fresh round of tariff uncertainty, yet the Tankan and wage trackers are consistent with cautious normalisation. Takaichi has also called for monetary policy to stay easy, saying that the BOJ shouldn’t raise borrowing costs4.

Takaichi’s victory brings a larger and earlier fiscal package than a more reform first alternative would have delivered. That should support consumption. It may also keep the yen contained if the market reads the policy mix as growth friendly rather than inflationary. A contained yen tends to be good for exporters. Factory automation and electrical machinery still benefit from reshoring and from the energy transition build out. Semiconductor equipment and components remain tied to a healing capital spending cycle in chips, with Artificial Intelligence (AI) orders the swing factor. These are export oriented sectors where Japan retains deep competitive moats.

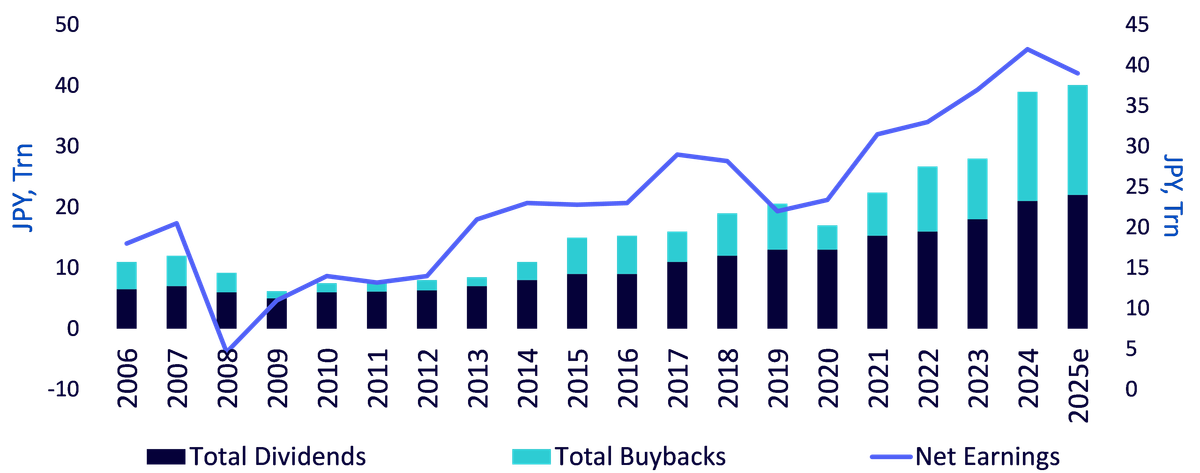

Corporate behaviour has been the quiet force behind the recent strength in equity markets. Boards are returning more cash. Authorisations for buybacks have surged and dividends are trending higher. The Tokyo Stock Exchange’s push on cost of capital and on low price to book laggards continues to change incentives. Idle assets are being sold. Cross holdings are slowly unwound. The outcome is a thicker cushion under per share earnings when top line growth is modest. It is also the reason why any cyclical pause feels less threatening than in past decades. Companies have more tools to defend results. They also have stronger balance sheets.

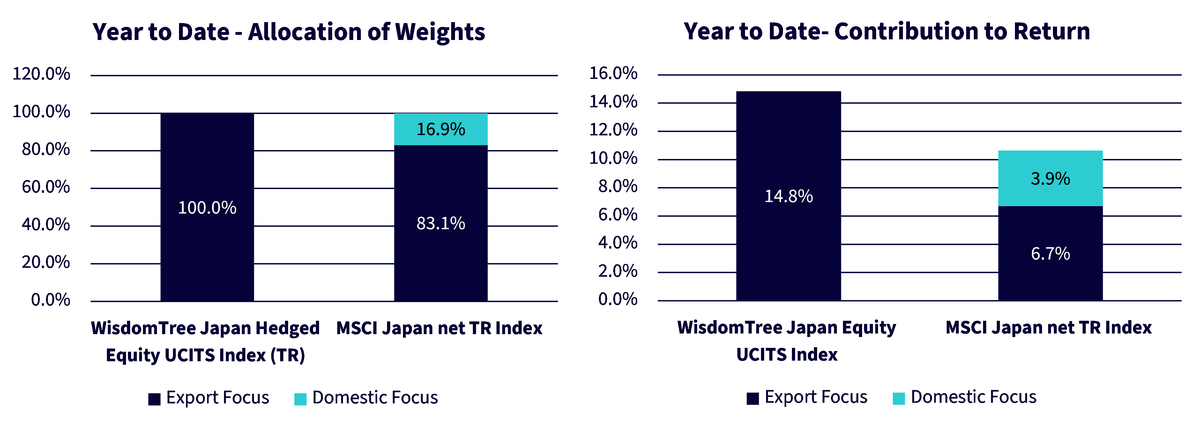

For investors seeking to capitalise on Sanae Takaichi’s victory and sector specific opportunities, the WisdomTree Japan Equity UCITS ETF USD Hedged (Ticker: DXJ) offers a valuable solution. DXJ tracks the WisdomTree Japan Hedged Equity UCITS Index (Ticker: WTIDJHUT) fundamentally weighted index that selects Japanese companies deriving at least 20% of revenue from overseas markets, with a strong emphasis on high dividend paying exporters and industrial cyclicals.

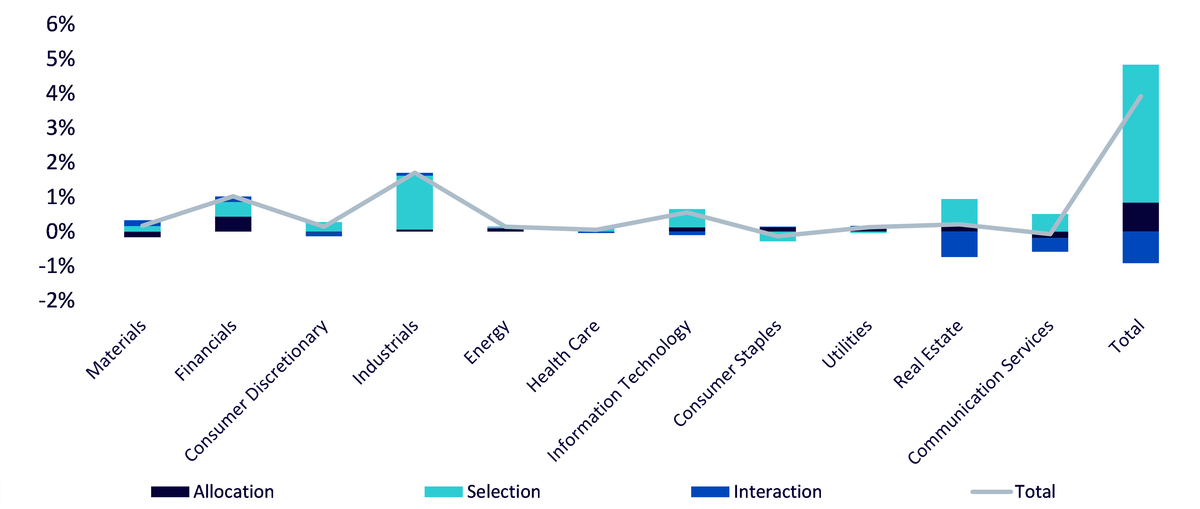

This aligns well with the expected beneficiaries of Sanae Takaichi’s victory and sector specific mix. In addition, DXJ has meaningful allocations to materials, financials and industrials, sectors that are expected to benefit from increased fiscal stimulus and a steeper Japanese yield curve. Over the past 10 years, the WisdomTree Japan Hedged Equity UCITS Index outperformed the MSCI Japan Index by 3.94% benefitting from its allocation to financials, industrials, information technology, real estate and communication services.

Source: FactSet, WisdomTree from 31 August 2015 to 29 August 2025. Historical performance is not an indication of future performance and any investments may go down in value.

DXJ incorporates a dividend weighting methodology that tilts toward higher-quality companies with stable cash flows and strong shareholder return profiles. As investor preference rotates toward income-generating, capital-efficient businesses, DXJ is well placed to capture this shift. This dividend orientation also aligns with the ongoing transformation in Japanese corporate behaviour, where firms are increasingly deploying capital via share buybacks and higher dividends—trends that have accelerated since the implementation of governance reforms and Tokyo Stock Exchange (TSE) pressure for improved Return on Equity (ROE).

Source: Universe of Tokyo Stock Exchange and Prime Market firms; net profits in FY25 based on latest Toyo Keizai forecasts, Bloomberg, FactSet as of 30 June 2025. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

A core feature of DXJ is its built-in USD hedging, which significantly reduces the impact of yen depreciation on total returns. DXJ helps isolate equity alpha from FX noise, providing a cleaner and more stable source of return.

This is especially important at a time when global macro conditions, particularly diverging central bank policies are driving substantial currency volatility. Year to Date (YtD), the WisdomTree Japan Hedged Equity UCITS Index outperformed the MSCI Japan Index by 4.8% benefitting from its higher allocation to Japanese exporters.

Source: FactSet, WisdomTree from 31 December 2024 of 29 August 2025. Historical performance is not an indication of future performance and any investments may go down in value.

Japan has a new political anchor and a clearer economic path. The Tankan shows demand holding. Trade frictions look manageable. The BoJ is edging toward normalisation without choking growth. Corporate reform is turning cash into returns. In this mix, a currency-hedged tilt to global exporters offers targeted access to earnings resilience with less currency noise.

1 JETRO, Japan External Trade Organisation

2 JETRO, Japan External Trade Organisation

3 Bank of Japan, 3 October 2025

4 Kyodo News as of 2 October 2025

Director, Macroeconomic Research, WisdomTree Europe

@AneekaGuptaWTAneeka Gupta is Director of Research at WisdomTree. Prior to the acquisition of ETF Securities in April 2018, Aneeka worked as an Equity & Commodities Strategist at the company. Aneeka has 17 years of experience working as a Research Analyst across a wide range of asset classes. In her current role she is responsible for conducting analysis for all in-house equity, commodity and macro publications and assisting the sales team with client queries around products and markets. Prior to WisdomTree, Aneeka began her career as an equity analyst at Bear Stearns International Ltd in London. She also worked as an Equity Sales Trader at Sunrise Brokers across US and Pan European Exchanges. Before that she worked as an Equity Derivatives Sales Manager at Mashreq Bank in Dubai. Aneeka holds a Masters in Mathematics from Oxford University and a BSc in Mathematics from the University of Delhi, India. She is also a CFA Charterholder.