3OIS LN

WisdomTree WTI Crude Oil 3x Daily Short

Veröffentlicht am 17. September 2025

Last week, OPEC+ (Organization of the Petroleum Exporting Countries plus allied producers) announced another increase in oil production, adding to the existing surplus. Yet markets shrugged off the news and oil prices continued to climb. Investors appear more concerned about tightening sanctions on Russia and Iran than about OPEC+’s policy moves.

OPEC+ restraint in context

OPEC+ has operated with multiple layers of production restraint in recent years (see summary below). The third layer of restraint—2.2 mb/d—has now been removed. Originally planned to unwind gradually over 18 months, it was instead rolled back swiftly in just six months between April and September 2025.

Group-Wide Cut (2.0 million barrels per day or mb/d): Announced in October 2022, this applies to all 22 OPEC+ members and is scheduled to remain in place through the end of 2026. Voluntary Cut (1.65 mb/d): Introduced in April 2023 by a subset of eight countries—Saudi Arabia, Iraq, Kuwait, Kazakhstan, Oman, Algeria, Russia, and the United Arab Emirates (UAE)—also running through the end of 2026. Additional Voluntary Cut (2.2 mb/d): Initiated in November 2023, this additional cut was borne again by the same “Group of Eight.” It was initially planned to be gradually unwound at a pace of approximately 138 thousand barrels per day (kb/d) between April 2025 and September 2026 but has been expedited and unwound by September 2025. |

|---|

Group-Wide Cut (2.0 million barrels per day or mb/d):

Announced in October 2022, this applies to all 22 OPEC+ members and is scheduled to remain in place through the end of 2026.

Voluntary Cut (1.65 mb/d):

Introduced in April 2023 by a subset of eight countries—Saudi Arabia, Iraq, Kuwait, Kazakhstan, Oman, Algeria, Russia, and the United Arab Emirates (UAE)—also running through the end of 2026.

Additional Voluntary Cut (2.2 mb/d):

Initiated in November 2023, this additional cut was borne again by the same “Group of Eight.” It was initially planned to be gradually unwound at a pace of approximately 138 thousand barrels per day (kb/d) between April 2025 and September 2026 but has been expedited and unwound by September 2025.

The new announcement

Last week, the Group of Eight announced plans to add another 137 kb/d to the market in October 2025, beginning the unwind of the second restraint layer (1.65 mb/d). If maintained monthly, the full tranche would be removed within 12 months, leaving only the group-wide 2.0 mb/d cut in place.

The decision was swift—reached in just 11 minutes during a virtual meeting—signalling OPEC+’s clear intent to regain market share lost during years of restraint, which enabled the US to surge ahead as the world’s largest oil producer.

Headline versus reality

The actual supply boost may fall short of targets. Iraq, the UAE, Kuwait, and Kazakhstan already produce ~1.1 mb/d above their quotas, while others, including Russia, face capacity limits. According to the IEA (International Energy Agency), OPEC+ will have increased crude output by just 1.5 mb/d since 1Q25—well below the announced 2.5 mb/d target.

Surplus or deficit?

The outlook diverges:

We see flaws in both forecasts. The IEA’s supply growth assumptions are likely too aggressive, given OPEC+’s delivery shortfalls. OPEC’s demand outlook is equally unrealistic, with seasonal summer demand winding down and China well-stocked with inventory.

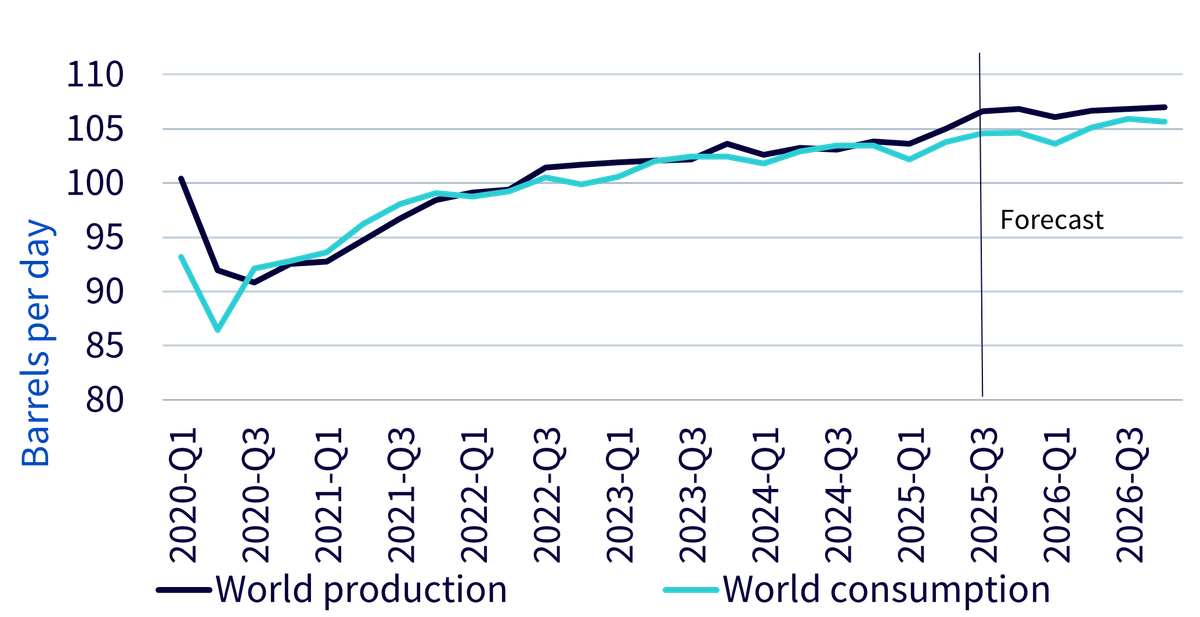

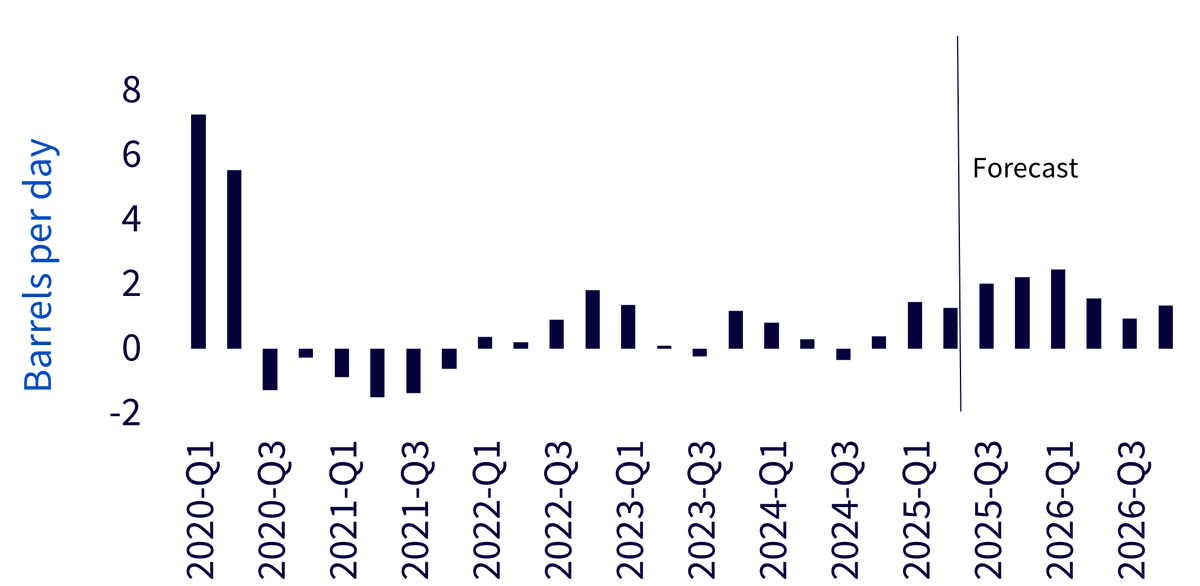

We expect a surplus, though smaller than the IEA’s forecast. A deficit seems unlikely absent a supply shock. The US Energy Information Administration’s (EIA’s) forecast of a 2.0 mb/d surplus from Q3 2025 through Q1 2026 is more reasonable. US output is expected to peak at a record 13.4 mb/d this year, before moderating slightly to 13.3 mb/d in 2026.

World production and consumption of oil and liquid fuels

World balance of oil and liquid fuels

Source: US Energy Information Administration, Short-Term Energy Outlook, September 2025. Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

Why have prices risen since the last OPEC+ announcement?

Despite rising surplus forecasts, prices have edged higher. Markets appear focused on the risk of secondary sanctions targeting Russian oil.

Since the Russia-Ukraine war began, India and China sharply increased Russian imports, taking advantage of discounts after G7 nations imposed a price cap ($60/barrel in 2022). Neither India nor China signed up to the cap, enabling Russia to redirect flows.

Now, the US is pressing G7 allies to impose tariffs—potentially as high as 100%—on Indian and Chinese purchases of Russian oil. President Trump, frustrated by a stalled Ukraine war and political pressure, is seeking tougher measures after earlier signalling a softer stance toward Russia.

If enforced, such tariffs could curb Russian exports, tightening global supply. However, in today’s inflation-sensitive environment, the appetite for strict sanctions is uncertain. Notably, Trump himself had previously urged OPEC+ to boost output to tame inflationary pressures. European G7 members, meanwhile, remain sceptical about tariffs as a policy tool.

Downside price pressure ahead

While markets focus on sanctions risk, the near-term effect of OPEC+’s production increases is underappreciated. Rising supply points to downside pressure on oil prices in the months ahead.

WisdomTree WTI Crude Oil 3x Daily Short

Head of Commodities and Macroeconomic Research, WisdomTree Europe

@NiteshShahWTNitesh Shah ist ein Finanzexperte mit über 24 Jahren Erfahrung in den Bereichen Research und Anlagestrategie. Als Head of Commodities & Macroeconomic Research bei WisdomTree Europa leitet er Marktanalysen und -einblicke für die verschiedenen Anlageklassen, wobei sein Schwerpunkt auf Rohstoffen und börsengehandelten Produkten liegt. Zuvor war er bei Moody's, HSBC Investment Bank, The Pension Protection Fund und Decision Economics tätig, wo er sein Fachwissen in den Bereichen Marktanalyse und Strategie vertiefte. Nitesh Shah hat einen Master-Abschluss in internationaler Wirtschaft und Finanzwesen von der Brandeis University und einen Bachelor-Abschluss in Wirtschaftswissenschaften von der London School of Economics. Seine Einsichten werden häufig in den Finanzmedien zitiert und er ist ein gefragter Redner bei Branchenveranstaltungen. Außerdem ist er Moderator des Podcasts „Commodity Exchange“, in dem er über Trends auf den globalen Märkten spricht. Nitesh Shah begeistert sich für die Beratung von Anlegern und bietet ihnen umsetzbare Erkenntnisse, die ihnen bei der Orientierung in der komplexen Finanzlandschaft helfen.