Can Genetically Modified Crops Help with Yields, Drought and Inflation?

2022 has been a difficult year for European agriculture.

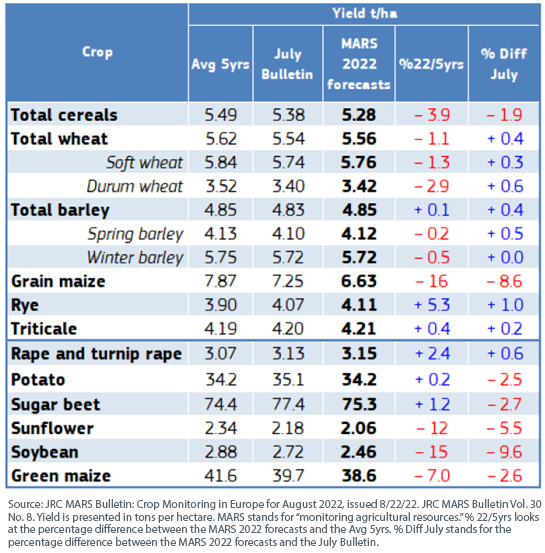

We can start with the Russia/Ukraine conflict and how that has changed market conditions and supply chains of certain critical things, like fertilizers. Then, we can continue with the fact that these difficulties were followed by drought conditions. Figure 1 summarizes some of what has become visible across the market of European agricultural yields.1

- Grain maize yield is expected to be down 8.6%.

- Sunflower yield is expected to be down 5.5%.

- Soybeans are expected to be down 9.6%.

Figure 1: Gauging the Crop Yield Forecasts in European Agriculture

Can Gene-Edited Crops Present a Solution?

There are European politicians expressing support for the use of genetic modification techniques in agriculture. Italian lawmakers are one such example, and the catalyst is that the recent heat waves and drought are leading to the demand for more resilient crops. If genetic modification is one path to provide for this type of mitigation, it’s possible it should receive all due consideration. Italy’s longest river recorded its lowest levels in the past 70 years over the summer season of 2022.2

One Genetically Modified Crop Is Grown in Europe

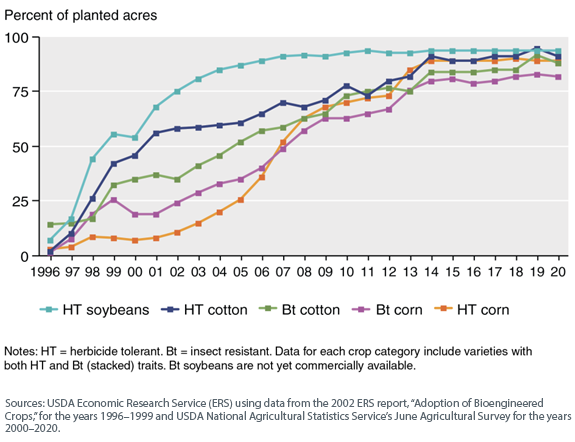

A certain bug-resistant strain of corn is the only genetically modified crop that has been grown within the European Union, based on the current highly restrictive rules. This is in stark contrast to the approach taken in the United States, where about 90% of the soybean and corn fields are genetically modified.3 Figure 2 illustrates the progression of a few different crops in the U.S.4

- Herbicide-tolerant soybeans saw the fastest ramp-up in terms of adoption, followed by herbicide-tolerant cotton. Herbicide-tolerant corn had a slower ramp-up, but then a later acceleration to roughly the same ending level in 2020.

- Insect-resistant cotton and insect-resistant corn also saw significant uptakes. As of this writing, insect-resistant soybeans were not yet commercially available.

Figure 2: Adoption of Genetically Engineered Crops in the United States, 1996–2020

Importantly, there is a difference between genetic modification and gene editing.5

- Genetic Modification: Genetic material from another organism is inserted into the DNA of a plant. Typically, this makes the plant resistant to insects or herbicides.

- Gene Editing: This is a newer technique, and it involves editing or adjusting the genome of the organism, not bringing in material from a different organism.

It was thought that gene editing might avoid GMO regulations in Europe, but these hopes were dashed in 2018 when the European Court of Justice ruled that gene-edited crops should be subject to the same regulations as GMOs.6

What Are the Most Desirable Outcomes?

If it is determined that the avoidance of gene editing and GMOs is the most desirable outcome, that is one thing. Maybe the current policies in Europe meet this goal. However, globally we have many different goals. Lowering greenhouse gas emissions is certainly another goal that is widely discussed in Europe and across the planet.

What if the wider adoption of genetically modified crops in Europe could reduce the equivalent of 7.5% of the total agricultural greenhouse gas emissions for the region? This is roughly equal to 33 million tons of carbon dioxide equivalents per year.7

Maybe the most desired outcome is to increase yield, since this could lead to greater food security for a given region, and it could also increase supply relative to a baseline during a time of higher inflation. Agricultural commodities tend to see their prices move based on supply and demand expectations. Research so far indicates the potential for genetically engineered crops to increase yields compared to non-altered baselines.8

Conclusion: Important to Keep All the Doors Open That We Can

2022 has been a stressful year in many respects. Higher inflation is stressful. Market performance is stressful. Thinking about a possible recession across much of the developed world is stressful. The fact that COVID-19 is still with us is stressful. The list goes on and on.

Thematic equity strategies, at their core, are about finding companies that are seeking to provide solutions for the big problems and the big questions. If the world is to support roughly 10 billion people by 2050—in a way that is as close to net neutral on a carbon emissions basis as possible—it is likely we will need to explore many solutions. How we decide to grow food is at the core of that.

WisdomTree’s BioRevolution strategy seeks to invest in an array of different companies focused on human health, agriculture and food, materials, chemicals, even energy—if a company can understand the information embedded in DNA, then it can open up further and further possibilities.

1 “JRC MARS Bulletin: Crop Monitoring in Europe for August 2022,” 8/22/22, vol. 30, no. 8.

2 Valentina Romano, “Italian MEPs back genetically modified crops in response to climate crisis,” EURACTIV, 7/8/22.

3 Matt Reynolds, “Europe’s Drought Might Force Acceptance of Gene-Edited Crops,” WIRED, 9/13/22.

4 Sources: USDA Economic Research Service (ERS) using data from the 2002 ERS report, “Adoption of Bioengineered Crops,” for the years 1996–1999 and USDA National Agricultural Statistics Service’s June Agricultural Survey for the years 2000–2020.

5 Source: Reynolds, 9/13/22.

6 Source: Reynolds, 9/13/22.

7 Source: Kovak et al., “Genetically modified crops support climate change mitigation,” Trends in Plant Science, 7/22, vol. 27, no. 7.

8 Source: Elisa Pellegrino et al., “Impact of genetically engineered maize on agronomic, environmental and toxicological traits: a meta-analysis of 21 years of field data,” Scientific Reports, 2/15/18, vol. 8.

Christopher Gannatti is an employee of WisdomTree UK Limited, a European subsidiary of WisdomTree Asset Management, Inc.’s parent company, WisdomTree Investments, Inc.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. The Fund invests in BioRevolution companies, which are companies significantly transformed by advancements in genetics and biotechnology. BioRevolution companies face intense competition and potentially rapid product obsolescence. These companies may be adversely affected by the loss or impairment of intellectual property rights and other proprietary information or changes in government regulations or policies. Additionally, BioRevolution companies may be subject to risks associated with genetic analysis. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. The composition of the Index is governed by an Index Committee, and the Index may not perform as intended. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.Share & Comment

Popular Posts

Categories

Related Links

Christopher Gannatti began at WisdomTree as a Research Analyst in December 2010, working directly with Jeremy Schwartz, CFA®, Director of Research. In January of 2014, he was promoted to Associate Director of Research where he was responsible to lead different groups of analysts and strategists within the broader Research team at WisdomTree. In February of 2018, Christopher was promoted to Head of Research, Europe, where he was based out of WisdomTree’s London office and was responsible for the full WisdomTree research effort within the European market, as well as supporting the UCITs platform globally. In November 2021, Christopher was promoted to Global Head of Research, now responsible for numerous communications on investment strategy globally, particularly in the thematic equity space. Christopher came to WisdomTree from Lord Abbett, where he worked for four and a half years as a Regional Consultant. He received his MBA in Quantitative Finance, Accounting, and Economics from NYU’s Stern School of Business in 2010, and he received his bachelor’s degree from Colgate University in Economics in 2006. Christopher is a holder of the Chartered Financial Analyst Designation.