A New Gold Standard in Capital Efficiency

I have worked alongside Jeremy Siegel, our Senior Investment Strategy Advisor, for over 20 years now.

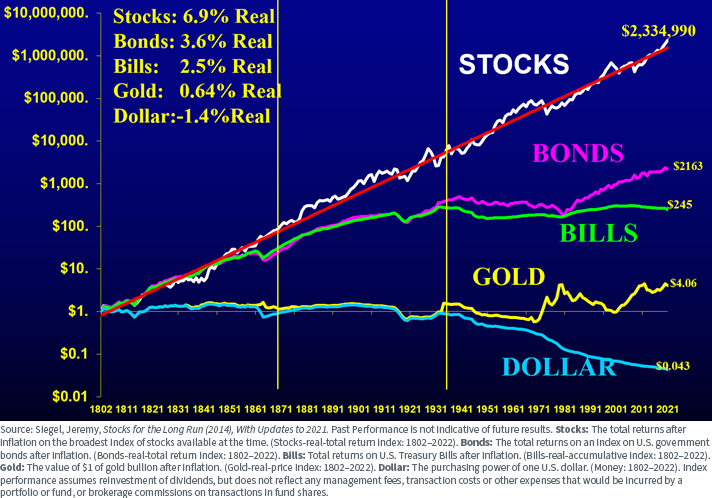

The central chart of his classic book, Stocks for the Long Run, shows the real, after-inflation returns of major asset classes over a 200-year history.

If you have seen him present, you’ve heard his punchline about the gold investment: a hypothetical $1 investment in gold in 1802 would translate to $4.06 of after-inflation purchasing power 220 years later.

In Stocks for the Long Run, his argument for stocks is the same. A $1 investment in stocks grows to over $2,334,990—with all the caveats that it would have been difficult to index and achieve the market returns in the same ways investors can replicate total market index strategies at just a few basis points of costs.

This 200+ year historical chart has been one of Siegel’s arguments against investing in gold over the really long run.

Yet, gold kept up with inflation over the long run and it provided a modest amount of after-inflation returns (less than 1% per year).

Total Real Return Indexes January 1802 – December 2021

When you look at the bond market today, real, after-inflation bond yields are in negative territory.

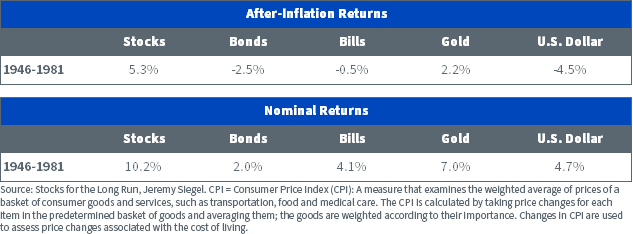

There was a long 35-year stretch of Siegel’s data, from 1946–1981, when bonds had a negative after-inflation return.

During that period, gold had a positive after-inflation return of 2.2% and 7% annually in nominal terms, beating the 4.7% per year rise in inflation.

Current Dynamics

Our outlook calls for above-average inflation over the next three to five years due to the large pandemic response and money supply growth that resulted from combined fiscal and monetary policies.

The inflation dynamics we see today resemble the 1946–1981 period. On a nominal basis, bonds returned 2%, while CPI averaged almost 5% a year. The current 10-year Treasury yield is under 2% and inflation is running at 7%. We see inflation cooling but it could very well average 4%–5% for the next 3–5 years. What to do?

Having to sell equities to fund allocations to gold—if you go by Siegel’s long-term chart—looks like a challenging proposition. But what if you stacked assets on top of each other to gain gold exposure without reducing your asset allocation to stocks?

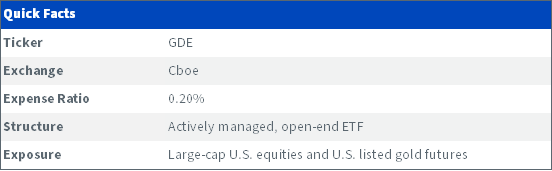

That is precisely what we are trying to achieve with the WisdomTree Efficient Gold Plus Equity Strategy Fund (GDE), which combines stock positions with gold futures.

GDE seeks to deliver a capital-efficient investment strategy with exposure to a market capitalization-weighted basket of the largest 500 U.S. equities and gold futures exposure added on top.

Here’s how it works: for every $100 invested, the Fund seeks to invest approximately $90 in the large-cap U.S. equities and $10 in short-term collateral. That collateral helps fund $90 in gold futures for $180 of total exposure to large-cap equities and gold futures in the Fund.

WisdomTree has previously launched capital-efficient strategies for stock and bond futures in a 90/60 combination across U.S., international and emerging markets. This 90/90 combination is a further extension of the capital-efficient framework utilizing gold.

Why Gold Now?

Investors often allocate to gold during cycles of turbulence as a tactical move to hedge risk. With a mix of historically low global interest rates and high inflation, investors are increasingly seeking portfolio diversifiers to hedge macro risk. We view gold exposure as a well-suited solution.

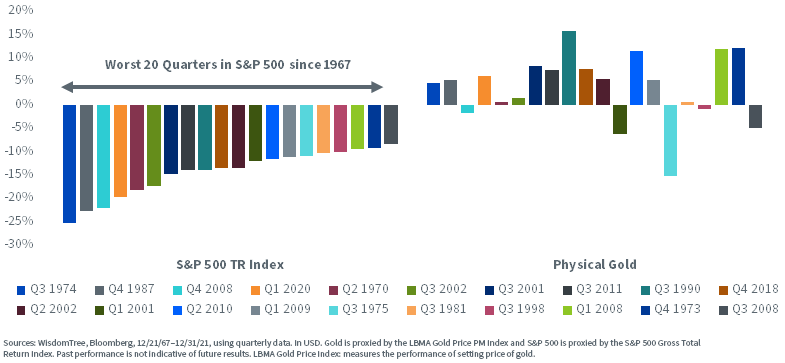

Gold can serve as a compelling portfolio diversifier—as an asset class, gold has historically been a positive performance outlier during large equity market drawdowns.

During the 20 worst quarters for the S&P 500 Index, gold outperformed by an average of 18.2%. In Q1 2020, during the onset of the COVID-19 pandemic, gold returned 6.22% compared to −19.6% for the S&P 500.

Gold returned positive performance in 15 of the 20 worst quarters for S&P 500

GDE within a Portfolio

GDE is an innovative and capital-efficient substitute for large-cap U.S. equity, multi-asset or alternative ETFs. Using leverage embedded in futures contracts, we believe GDE can help diversify a portfolio with better capital efficiency.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. The Fund is actively managed and invests in U.S.-listed gold futures and U.S. equity securities. The Fund’s use of U.S.-listed gold futures contracts will give rise to leverage, magnifying gains and losses and causing the Fund to be more volatile than if it had not been leveraged. Moreover, the price movements in gold and gold futures contracts may fluctuate quickly and dramatically, and have a historically low correlation with the returns of the stock and bond markets. U.S. equity securities, such as common stocks, are subject to market, economic and business risks that may cause their prices to fluctuate. The Fund’s investment strategy will also require it to redeem shares for cash or to otherwise include cash as part of its redemption proceeds, which may cause the Fund to recognize capital gains. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Neither diversification nor asset allocation strategies assure a profit or protect against loss. Investors should consider their investment time frame, risk tolerance level and investment goals.

Professor Jeremy Siegel is a Senior Investment Strategy Advisor to WisdomTree Investments, Inc., and WisdomTree Asset Management, Inc. This material contains the current research and opinions of Professor Siegel, which are subject to change, and should not be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. The user of this information assumes the entire risk of any use made of the information provided herein. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

Share & Comment

Popular Posts

Categories

Related Links

Jeremy Schwartz has served as our Global Chief Investment Officer since November 2021 and leads WisdomTree’s investment strategy team in the construction of WisdomTree’s equity Indexes, quantitative active strategies and multi-asset Model Portfolios. Jeremy joined WisdomTree in May 2005 as a Senior Analyst, adding Deputy Director of Research to his responsibilities in February 2007. He served as Director of Research from October 2008 to October 2018 and as Global Head of Research from November 2018 to November 2021. Before joining WisdomTree, he was a head research assistant for Professor Jeremy Siegel and, in 2022, became his co-author on the sixth edition of the book Stocks for the Long Run. Jeremy is also co-author of the Financial Analysts Journal paper “What Happened to the Original Stocks in the S&P 500?” He received his B.S. in economics from The Wharton School of the University of Pennsylvania and hosts the Wharton Business Radio program Behind the Markets on SiriusXM 132. Jeremy is a member of the CFA Society of Philadelphia.