Checking In on International Equity Markets

We’ve written extensively about our growing optimism on international equities recently, and our enthusiasm hasn’t faded.

We’re encouraged by economic data that continues to rebound, while the approval, acquisition and distribution of vaccines seem to be improving at the same time. We think this creates a compelling opportunity to reinvest in the revival of developed market equities, all while the region takes encouraging, albeit cautious, steps to reopen its local economies.

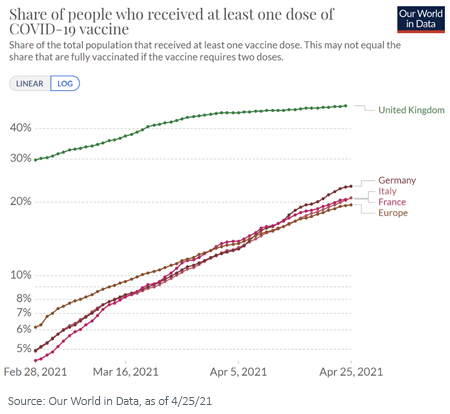

Vaccinations Are Picking Up Steam

Since the beginning of March, COVID-19 vaccination rates have steadily improved throughout Europe, which is a major component of the international equity region. The trend is promising, with 20% of the four major European economies having received at least one dose. The United Kingdom has had the most success thus far, hovering at nearly 50%.

Since the vaccination program gained momentum in March, a few countries (most notably the U.K.) have begun to revive their economies one step at a time. While the pace certainly remains cautious, we think the rest of the region may not be far behind.

A Cyclical Revival

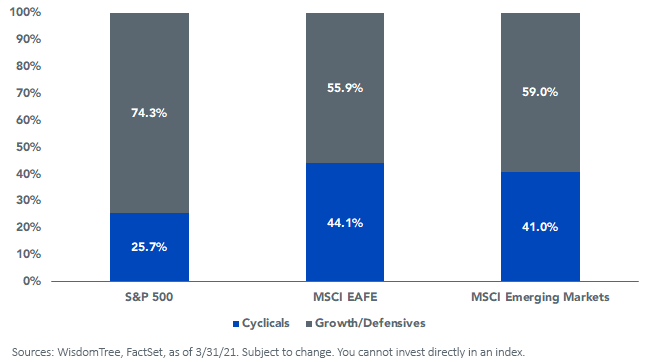

The vaccine momentum leads us to believe there’s potential for a strong revival in cyclical economic sectors, which are key pieces of developed markets relative to the rest of the world. In the chart below, we group the weights of the Financials, Industrials, Materials and Energy sectors—those most levered to overall levels of economic activity—together into our Cyclical category, while Growth/Defensives contains the remaining weight.

Developed equity markets, proxied by the MSCI EAFE Index, are nearly 45% comprised of cyclical sectors, roughly a 20% over-weight to the S&P 500 in the U.S.

Sector Composition of Regional Equity Markets

How Quality Can Help Overseas

Sector composition is not the only potential catalyst we see in developed markets, however. Recent factor performance has looked promising as well.

Since the start of March, the quality factor has caught a tailwind. The MSCI EAFE Quality Index, a proxy for quality, has outperformed all other factors (size, growth, value, minimum volatility and high dividend yield) in the region by at least 1.5% on a U.S. dollar basis (as of April 23).

This is no short-term anomaly in our opinion, however, as quality has an impressive track record over longer periods in international equity markets. Over the past two-, three- and five-year periods, the MSCI EAFE Quality Index outperformed all other factors in the region as well.

A Quality Solution for Developed Market Equities

In 2015, we launched the WisdomTree International Hedged Quality Dividend Growth Fund (IHDG), followed by its non-currency-hedged counterpart, WisdomTree International Quality Dividend Growth Fund (IQDG), a year later.

Both Funds track Indexes that employ the same strategy, resulting in exposure to companies with strong earnings, healthy balance sheets and low leverage. They select the top 300 companies from the dividend-paying, international equity universe, ranked by a combination of dividend growth and quality factors. Likewise, the two Funds deliver attractive fundamentals.

Improved Fundamentals

There are two important points to consider.

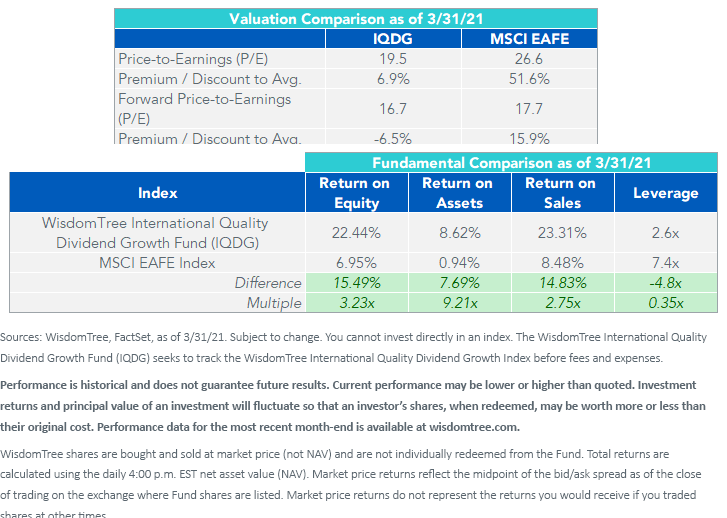

Valuations. As markets recovered from the onset of the pandemic last March, the price-to-earnings (P/E) ratio of the MSCI EAFE Index surged to a 50% premium over its historical average (since IQDG inception in April 2016). Forward P/E ratios followed suit, climbing to a 30% premium over the same time frame. But IQDG remained modestly valued at a 7% premium to its historical average P/E and a 7% discount to its historical average forward P/E. This signals to us that the quality factor helped keep valuations in control without sacrificing upside performance potential.

Quality Where It Matters Most. The ethos of the quality factor is a focus on profitability, efficient operations and strong balance sheets in order to deliver healthy results. IQDG exemplifies this, having delivered more than 3x more return on equity (ROE), 2.75x more return on sales (ROS),and 9x more return on assets (ROA), all with about one-third the leverage of the MSCI EAFE.

For standardized performance of IQDG, please click here.

No Better Time Than Now

We believe 2021 may mark a turning point for international equity markets, and the results of WisdomTree’s quality dividend growth approach speak for themselves.

Whether you’re interested in a currency-hedged or unhedged strategy when investing abroad, there’s evidence that a focus on the quality factor can potentially create healthier fundamentals, control valuations and target sectors with attractive prospects for the future.

Unless otherwise stated, all performance and information sourced from WisdomTree, FactSet, Morningstar, and/or Zephyr StyleADVISOR, as of March 31, 2021.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. To the extent the Fund invests a significant portion of its assets in the securities of companies of a single country or region, it is likely to be impacted by the events or conditions affecting that country or region.

Dividends are not guaranteed and a company currently paying dividends may cease paying dividends at any time. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. Derivative investments can be volatile and these investments may be less liquid than other securities, and more sensitive to the effect of varied economic conditions. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read each Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links

Brian Manby joined WisdomTree in October 2018 as an Investment Strategy Analyst. He is responsible for assisting in the creation and analysis of WisdomTree’s model portfolios, as well as helping support the firm’s research efforts. Prior to joining WisdomTree, he worked for FactSet Research Systems, Inc. as a Senior Consultant, where he assisted clients in the creation, maintenance and support of FactSet products in the investment management workflow. Brian received a B.A. as a dual major in Economics and Political Science from the University of Connecticut in 2016. He is holder of the Chartered Financial Analyst designation.