A Backup Plan for Your European Summer Vacation

A fascinating development in the post-financial crisis era is the increasing realization of the limitations of monetary policy.

By cutting interest rates and buying bonds (among other activities), a central bank can help inject capital into the financial system and provide relief for market participants during times of stress.

But these activities accomplish little to fix the issue of demand. The average consumer on the street is unlikely to directly feel the impact from the Federal Reserve (Fed) opening a new credit facility to help shore up the corporate bond market.

Fiscal policy, on the other hand, has been shown to make more of a sizable economic difference from a demand perspective, especially in a consumer-driven economy. Giving people money in times of crisis to pay their bills or to spend it? There’s your demand.

There’s just that tiny little issue of getting politicians to agree on anything.

Consider a wildly accommodative central bank that has been doing everything in its power but has remained unable to stoke growth or inflation for many years. Also consider bitter fighting between politicians that only reinforces gridlock and prevents any meaningful progress from a fiscal stimulus perspective. Only recently was there a breakthrough where the fiscal gridlock was finally broken.

That may sound like the U.S. (with the first pandemic stimulus bill, at least), but I’m talking about Europe.

ECB No Longer on Its Own

In late July, European leaders came to an agreement on the EU Recovery Fund, which provides loans and grants to member states to be funded by joint debt issuance.

This historic symbolic agreement could mark a turning point in Europe’s future. It is the first major shared fiscal responsibility from European members, and it directly addresses one of the main criticisms of the structure of the EU.

For years, the European Central Bank (ECB) has done everything it could to help stimulate growth on its own. Now, finally, the frugal northern countries and more fragile southern countries have aligned to provide a powerful joint monetary and fiscal stimulus package.

To be fair, like the result of every political negotiation, the agreement isn’t a panacea, and its impact won’t immediately be felt in 2020.

But it is an important milestone that proves that the bloc can, in fact, work together fiscally. And it unquestionably improves the growth potential of the region over the next few years.

A Strong Response to an Already Strong Response

In addition to the coordinated fiscal and monetary stimulus, many European countries also deserve plaudits for their response to the COVID-19 pandemic.

Italy was the first European country to experience the full horrific potential of the virus, and Spain has seen cases tick up of late. But the overall response looks admirable, particularly compared to the U.S.

On a per million basis, the U.S. and EU both saw deaths peak around 6.5–6.6 in early April. Unlike the U.S., which saw its death rate drop to 1.5 but then surge to 3.4, the EU’s rate has hovered around 0.2 since mid-July. Both raw and adjusted daily new cases in the EU have risen of late. But the cases per million sit at only 13% of the equivalent U.S. number in early August.1

The result of the successful response is that mobility has risen, and economic activity is following suit. The composite PMI for the EU has risen sharply to 54.9 in July2, comfortably in expansionary range.

Economic surprises are jumping as well. EU GDP growth is expected to surpass that of the U.S. in 2021, a feat that has only happened eight times since 19923. The euro is rising on relative growth expectations differentials, and net long euro positioning just hit an all-time high4.

Slowly but surely, momentum is building.

Should the global economy stabilize, given the outsized role that multinational companies play in European equity markets, the region’s stocks would stand to benefit more than most.

Finally, the long-awaited rotation from growth to cyclical assets—in which European equities firmly sit—is seeing signs of life after being left for dead during much of the post-crisis era.

All of this adds up to a newfound optimistic view on the region.

Welcome Back, Strangers!

It has been a while since European stocks were met with optimism.

From 2012 to 2015, Europe-focused ETFs and mutual funds took in $69.5 billion in assets. Since then, more than $40 billion has been unwound via outflows5.

For investors who may have forgotten how to invest there while they ignored the asset class over the last five years, the question remains—what to own?

A common justification for the persistent underperformance of European stocks relative to the U.S. is that there is no equivalent to the tech champions of Silicon Valley. Tech is only 7.6% of the MSCI Europe Index, which represents only about half of its exposure to the troubled financials6.

In addition to not owning enough exciting, high-growth companies, the profitability of corporate Europe is lacking as well. Different profitability measures like return on equity (ROE), return on assets (ROA) and return on sales (ROS) all sit well below those of emerging markets, let alone the U.S.

When junk is everywhere, a quality filter is of paramount importance.

That is why, instead of settling for the entire market, we suggest a quality-focused approach, like our Europe Quality Dividend Growth Fund (EUDG).

Quality Works in Europe—Perhaps More Than Anywhere Else

EUDG represents quality within a value asset class. Its profitability ratios are multiples better than those of the MSCI Europe Index (and even rank higher than those of the S&P 500).

Why does this matter? Because quality works in Europe, perhaps more than anywhere else in the world.

Dividing equity markets into ROE quintiles shows that during the Q1 equity sell-off, quality outperformed around the world. In Europe, the excess performance of the highest ROE quintile—7.3% better than the broad index—was the highest of any major equity region in the globe7.

In the snapback since then, high-quality stocks in Europe have captured 91% of the market’s rally—a respectable number on its own and more than 500 bps better than the lowest quality quintile8.

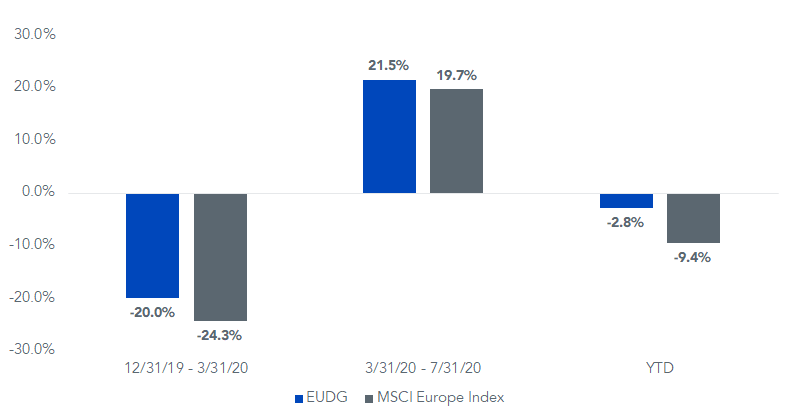

EUDG has experienced the best of all worlds— mitigating downside losses when the market sold off, while also participating in more than 100% of the rebound since March.

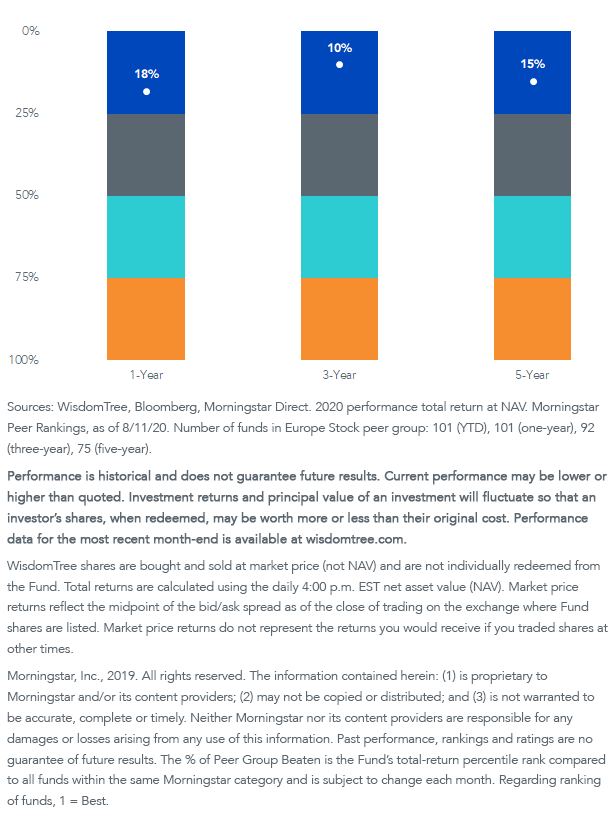

Consistent performance through different market environments helps explain how the Fund sits in the top quartile of all European stock funds—both active and passive—on all time frames over the past five years.

Sure, most Americans are currently unable to enter Europe. But even though it may not be the same as a summer vacation on Mediterranean beaches, a great buying opportunity still has to count for something, right?

2020 Performance and Peer Rankings

For standardized performance of EUDG, please click here.

1Financial Times, as of 8/4/20.

2Bloomberg, as of 7/31/20.

3Bloomberg, as of 8/10/20.

4Bloomberg, as of 8/10/20.

5Morningstar Direct, as of 6/30/20.

6MSCI, as of 7/31/20.

7WisdomTree, FactSet, as of 3/31/20.

8WisdomTree, FactSet, as of 7/31/20.

Important Risks Related to this Article

There are risks associated with investing, including possible loss of principal. Foreign investing involves special risks, such as risk of loss from currency fluctuation or political or economic uncertainty. This Fund focuses its investments in Europe, thereby increasing the impact of events and developments associated with the region, which can adversely affect performance. Dividends are not guaranteed, and a company currently paying dividends may cease paying dividends at any time. Investments in currency involve additional special risks, such as credit risk and interest rate fluctuations. As this Fund can have a high concentration in some issuers, the Fund can be adversely impacted by changes affecting those issuers. The Fund invests in the securities included in, or representative of, its Index regardless of their investment merit, and the Fund does not attempt to outperform its Index or take defensive positions in declining markets. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Share & Comment

Popular Posts

Categories

Related Links