BTCW LN

WisdomTree Physical Bitcoin

Published 3 February 2026

Director, Digital Assets Research

Bitcoin performs best when confidence in fiat money and policy credibility is weakening, and when liquidity is abundant or expected to return.

That makes bitcoin structurally different from inflation-linked assets, equities, or even gold.

The mistake investors repeatedly make is treating bitcoin as a simple inflation hedge. Bitcoin however responds to liquidity conditions, real interest rates and trust in monetary institutions, not to month-to-month consumer price index (CPI) prints.

Understanding which macro regime bitcoin favours matters for strategic allocation, expectation-setting and avoiding costly category errors.

When inflation is high and central banks appear behind the curve, bitcoin’s fixed-supply narrative gains traction. Its appeal stems from absolute scarcity (capped at 21 million coins) which contrasts sharply with discretionary monetary expansion during periods of policy stress.

Bitcoin, however, is not a mechanical hedge against CPI inflation. Historically:

In other words, bitcoin hedges monetary disorder, not day-to-day cost-of-living pressures. That distinction is critical. Bitcoin thrives when inflation undermines confidence in policy frameworks, not when prices merely rise.

Aggressive tightening cycles are bitcoin’s least favourable environment.

Liquidity withdrawal hits ‘speculative’ and duration-sensitive assets first. Rising real interest rates increase the opportunity cost of holding non-yielding assets such as bitcoin, while tighter financial conditions force the unwinding of leverage, amplifying drawdowns.

Source: Artemis Terminal, Federal Reserve Bank of St. Louis, WisdomTree. 12 January 2026. Historical performance is not an indication of future performance, and any investment may go down in value.

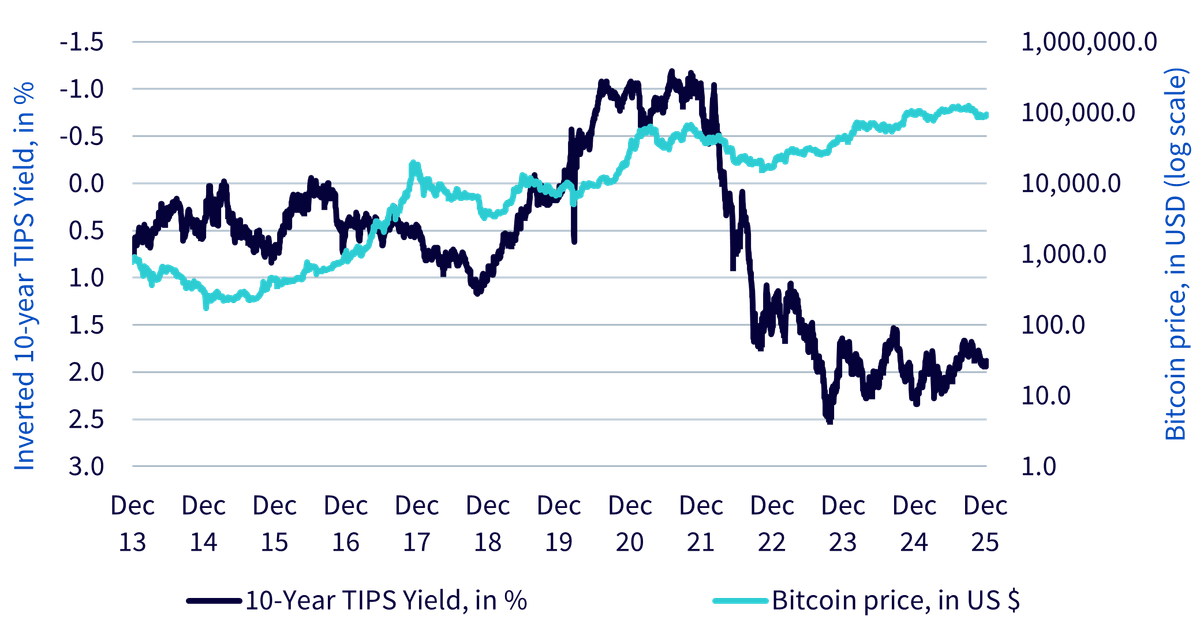

Bitcoin tracks real interest rates far more closely than inflation. As real yields rise, bitcoin struggles. As they peak and roll over, bitcoin historically begins to stabilise and recover.

Crucially, bitcoin has tended to bottom before policy pivots, not after them. Tightening phases are painful, but they often clear excess leverage and set the stage for the next structural rally once expectations shift from restriction to stabilisation.

This is bitcoin’s strongest regime. Falling real rates materially reduce the opportunity cost of holding non-yielding assets, while expanding liquidity disproportionately benefits scarce assets such as bitcoin. Although easing environments typically support all risk assets, bitcoin has often outperformed, combining liquidity sensitivity with a fixed-supply narrative to generate asymmetric upside.

Major bitcoin bull cycles coincided with accommodative monetary policy and balance-sheet expansion. Importantly, bitcoin responds not only to realised easing, but to expectations of easing, often repricing ahead of formal policy action.

This forward-looking behaviour reinforces bitcoin’s role as a liquidity-sensitive asset with convex upside, particularly early in easing cycles when policy credibility is being re-established.

Bitcoin is not a traditional crisis hedge. It is a hedge against the policy consequences crises tend to provoke.

During acute stress, bitcoin often sells off alongside other risk assets as investors prioritise cash and liquidity. This pattern is visible across historical ‘crypto winters.’

3 crypto winters | Bitcoin price change |

|---|---|

31 December 2013 - 25 January 2015 | -75.49% |

18 December 2017 - 14 December 2018 | -83.10% |

10 November 2021 - 21 November 2022 | -72.74% |

Source: Bloomberg, WisdomTree. Historical performance is not an indication of future performance, and any investment may go down in value.

Bitcoin bear markets coincided with liquidity withdrawal, not with inflation peaks.

However, once immediate stress subsides, episodes involving bank failures, capital controls, or sovereign risk tend to reinforce bitcoin’s appeal as a non-sovereign monetary asset. Historical examples include unprecedented monetary expansion following COVID-19 and the US regional banking stress in 2023.

In each case, bitcoin demand rose not during the initial shock, but in response to the policy reaction.

In environments characterised by credible central banks, positive real yields and low macroeconomic volatility, bitcoin’s value proposition weakens.

Fiat currencies function sufficiently well to limit demand for monetary alternatives, while positive real yields raise the opportunity cost of holding non-yielding assets. Subdued volatility also dampens speculative appetite.

That said, this regime has proven rare and short-lived in practice. Since 2008, sustained macro stability has been the exception rather than the rule.

Bitcoin does not thrive in a single, neatly defined macro regime. It performs best when confidence in fiat money, institutions, or policy frameworks is weakening, and when liquidity is abundant or expected to return.

Conversely, bitcoin has historically struggled during periods of aggressive real-rate increases, indiscriminate liquidity withdrawal, and durable macro stability; environments where the opportunity cost of holding non-yielding assets rises sharply.

This leads to bitcoin’s most useful framing for investors: not as a pure inflation hedge, not as a conventional risk asset, and not as digital gold, but as a long-duration option on monetary disorder and liquidity expansion.

Its value proposition is inherently convex: volatile in the short term, but increasingly compelling over longer horizons marked by rising debt burdens, fiscal dominance and constrained policy flexibility.

Approached this way, bitcoin fits best as a strategic allocation rather than a tactical trade, with volatility representing the price investors pay for exposure to a distinct and increasingly relevant macroeconomic theme.

WisdomTree Physical Bitcoin

Director, Digital Assets Research

Dovile Silenskyte is a director of digital assets research at WisdomTree. Before joining WisdomTree in May 2024, Dovile worked as an index equity product strategist at BlackRock. Currently, she is responsible for conducting analyses for in-house digital assets publications and assisting the sales team with client queries about products and markets. Dovile holds an MSc in Finance from Texas A&M University – Commerce, and she is also a chartered financial analyst (CFA).